How Family-Owned and Private Banks Globally Built the Principles of Trust, Governance, and Legacy That Underpin Modern Financial Institutions

Introduction: Five Centuries of Financial Trust

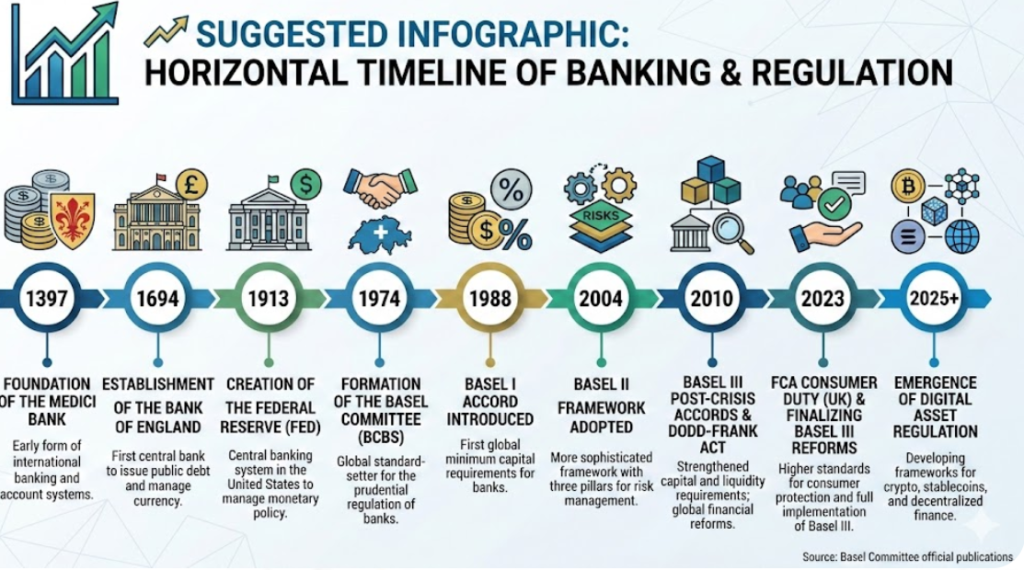

In 1397, Giovanni di Bicci de’ Medici opened a modest exchange house in Florence. Within two generations, his descendants were financing popes, monarchs, and the Renaissance itself. More than 600 years later, the Medici legacy endures — not in bricks and mortar, but in the foundational DNA of every modern bank: trust, fiduciary responsibility, and governance.

Today, global banking assets exceed $180 trillion (IMF Global Financial Stability Report, 2024), yet the principles sustaining those assets were largely forged centuries ago by family-owned dynasties and private merchant banks. Understanding their evolution is not merely a historical exercise — it is a strategic imperative for financial professionals navigating an era of digital disruption, ESG mandates, and intensifying regulatory scrutiny.

This article examines how the world’s most enduring banking dynasties — from the Medicis of Florence to the Rothschilds of London and Frankfurt — built frameworks of trust and governance that remain the bedrock of international finance. We explore how these principles have been codified into modern standards by bodies such as the Basel Committee on Banking Supervision, the International Monetary Fund (IMF), and the Financial Stability Board (FSB), and how FinTech innovators are reimagining them for the digital age.

📊 KEY GLOBAL BANKING STATISTICS AT A GLANCE

| Metric | Figure |

| Global Bank Assets | $180+ trillion (IMF, 2024) |

| Basel III Coverage | Over 100 jurisdictions globally |

| ESG-Linked AUM | $35+ trillion (Global Sustainable Investment Alliance, 2024) |

| Mobile Banking Users | 2.5+ billion globally (World Bank, 2023) |

| Oldest Active Bank | Banca Monte dei Paschi di Siena, est. 1472 |

Part I: Key Concepts in Global Financial Governance

Before tracing the arc of banking history, it is essential to define the foundational concepts that thread through this narrative.

Financial Intermediation

Financial intermediation is the process by which financial institutions channel funds from surplus economic units (savers) to deficit economic units (borrowers). The Medici bank pioneered this at scale — accepting deposits from wealthy merchants and deploying capital across trade routes spanning Europe and the Levant. Today, this function is regulated under frameworks including the Basel III Accord and monitored globally by the IMF’s Financial Sector Assessment Programs (FSAPs).

Maturity Transformation

One of banking’s most powerful — and perilous — functions, maturity transformation involves borrowing short-term (e.g., customer deposits) and lending long-term (e.g., mortgages, trade finance). The Rothschild network mastered this across borders, effectively creating international liquidity bridges between capital-rich and capital-hungry economies. Modern central banks, including the European Central Bank (ECB) and the Federal Reserve, manage systemic risks arising from maturity transformation through tools such as the Liquidity Coverage Ratio (LCR) and Net Stable Funding Ratio (NSFR), both mandated under Basel III.

Fiduciary Responsibility

Fiduciary responsibility is the legal and ethical obligation to act in the best interests of clients and stakeholders — placing their welfare above institutional self-interest. Family banking dynasties enshrined this through the concept of merchant honour: a private bank’s word was its bond. Modern regulators have codified this principle in the UK Financial Conduct Authority’s (FCA) Consumer Duty framework, the SEC’s fiduciary standard for investment advisors, and the emerging IOSCO (International Organization of Securities Commissions) principles for sustainable finance.

Corporate Governance in Banking

At its core, corporate governance in banking refers to the systems, principles, and processes by which financial institutions are directed and controlled. The Medicis introduced rudimentary governance through partnership agreements and segregated branch accounts — innovations that presage today’s OECD Principles of Corporate Governance and the Basel Committee’s Guidelines on Corporate Governance for Banks (2015, revised 2023).

Part II: The Great Banking Dynasties — Origins of Modern Financial Governance

The Medici Bank (1397–1494): Inventing the Architecture of Trust

The Medici Bank was arguably the world’s first multinational financial institution. At its zenith, it operated branches in London, Bruges, Lyon, Geneva, Rome, and Venice — each governed by a sistema di accomandita (a form of limited partnership) that ring-fenced liabilities and preserved the parent institution’s capital. This structural innovation is the forerunner of modern legal entity frameworks and subsidiary governance standards enforced by regulators globally today.

Three governance pillars defined the Medici model:

- Decentralised Autonomy: Branch managers held equity stakes and operated independently — aligned incentives long before the term ‘principal-agent theory’ existed.

- Double-Entry Bookkeeping: The Medicis refined Venetian accounting methods into the foundation of modern financial reporting, a system now mandated by IFRS and GAAP globally.

- Relationship Banking: Trust was maintained through long-term, personal relationships with clients — the conceptual ancestor of modern Private Banking and Wealth Management practices.

“The Medicis did not merely lend money; they financed civilisation. Their governance model — built on accountability, distributed risk, and reputation — is more relevant today than most modern compliance frameworks.”

— Prof. Niall Ferguson, Harvard Kennedy School, Author of ‘The Ascent of Money’

The Fugger Dynasty (1487–1657): Risk Management Before Basel

The Augsburg-based Fugger family became the dominant financiers of the Habsburg Empire, extending credit lines to emperors and funding transatlantic expeditions. Their Fuggerei — a social housing project established in 1521 and still operating today — represents arguably the world’s first institutionalised ESG (Environmental, Social, Governance) initiative in financial history.

The Fuggers pioneered sovereign credit risk assessment, developing informal but sophisticated frameworks for evaluating a monarch’s creditworthiness based on tax revenues, territorial assets, and political stability. This analytical tradition is the intellectual precursor to today’s sovereign credit ratings issued by Moody’s, S&P Global, and Fitch Ratings — and to the IMF’s Article IV Consultation surveillance framework.

The Rothschild Network (1760s–Present): Cross-Border Financial Governance

No banking dynasty better illustrates the globalisation of financial governance than the Rothschilds. Founded by Mayer Amschel Rothschild in Frankfurt’s Judengasse, the family established coordinated banking houses in Frankfurt, London, Paris, Vienna, and Naples — effectively creating the world’s first cross-border information and capital network.

Their enduring governance innovations include:

- Information Asymmetry as Competitive Advantage: The Rothschilds maintained encrypted courier networks for real-time intelligence — anticipating modern Bloomberg terminals and algorithmic trading platforms.

- Interoperability Across Jurisdictions: Each house operated under local legal frameworks while adhering to shared Rothschild governance standards — presaging today’s cross-border regulatory equivalence frameworks under MiFID II and Basel III.

- Succession Planning as Strategy: Strict intra-family succession and partnership inheritance rules ensured institutional continuity — a model now enshrined in modern banking’s regulatory requirements for succession planning and key-person risk management (FSB, 2023).

“The Rothschild Brothers were the inventors of international finance. Their network was the 19th century’s equivalent of SWIFT — and far more discreet.”

— Dr. Alasdair Roberts, Professor of Finance History, University of London

Part III: Global Context — How Different Regions Codified the Legacy

Europe: The Regulatory Vanguard

Europe has historically led the codification of banking governance principles. The Basel Committee on Banking Supervision (BCBS), established in 1974 by the G10 central bank governors following the collapse of Bankhaus Herstatt, represents the most significant formal heir to the dynastic governance tradition. Basel I, II, and III progressively refined capital adequacy, liquidity, and leverage standards that now govern more than 100 jurisdictions globally.

The European Central Bank’s (ECB) Single Supervisory Mechanism (SSM) extends dynastic-era principles of unified governance over distributed entities — directly echoing the Medici branch-management model — to the Eurozone’s 120 most significant financial institutions. Meanwhile, the FCA’s Consumer Duty (2023) reinstates fiduciary obligation as the cornerstone of financial services regulation in the United Kingdom.

North America: Market-Driven Governance Evolution

The American banking tradition evolved through periodic crises that forced governance improvements. The establishment of the Federal Reserve System in 1913 — itself modelled partly on the Banque de France and the Bank of England — institutionalised the lender-of-last-resort function that private dynasties had informally performed for centuries. J.P. Morgan’s personal intervention to stem the Panic of 1907, lending his own creditworthiness to stabilise the system, represents the last great act of dynastic financial stewardship — and the moment that crystallised the need for a permanent public institution.

Today, the Dodd-Frank Act (2010) and the SEC’s enhanced disclosure requirements carry forward the transparency and accountability imperatives that family banks maintained through reputation and relationships.

Asia-Pacific: Tradition Meets Innovation

In Asia, long-standing merchant banking traditions — from the hundi networks of South Asian traders to the qianzhuang (native banks) of imperial China — operated on relationship-based trust frameworks with striking parallels to European dynastic banking. Today, institutions such as the Bank for International Settlements’ (BIS) Asian Consultative Council work to harmonise these traditions with Basel standards across APAC jurisdictions.

Africa & Emerging Markets: Financial Inclusion as Governance Imperative

Perhaps the most compelling contemporary expression of banking’s trust heritage is the rise of mobile financial services in sub-Saharan Africa. M-Pesa, launched in Kenya in 2007, extended financial intermediation to millions previously excluded from the formal banking system — achieving in a decade what dynastic banks took centuries to accomplish in Europe. The World Bank’s Global Findex Database (2023) reports that mobile money accounts now serve over 184 million adults in Sub-Saharan Africa, demonstrating that the foundational banking principle of trust-based access to capital transcends geography and technology.

Part IV: Case Studies in Global Financial Governance Excellence

Case Study 1: BlackRock — The Modern Asset Management Dynasty

Founded in 1988, BlackRock has become the world’s largest asset manager, overseeing approximately $10 trillion in assets under management (AUM) as of 2024. Its Aladdin risk management platform — processing data on assets worth over $21 trillion globally — represents the technological evolution of the Rothschilds’ information network: a centralised intelligence system deployed to manage distributed risk across a global portfolio.

BlackRock’s Annual Stewardship Report and public letters from CEO Larry Fink to corporate leaders have redefined the role of institutional investors in corporate governance, advocating for ESG integration, board diversity, and long-term value creation — principles that would have been familiar to Medici family council members deliberating on the social responsibilities of wealth.

Case Study 2: The Rothschild Continuation — Private Banking in the 21st Century

Rothschild & Co, still majority family-owned after more than 250 years, exemplifies the durability of governance-driven banking models. The group’s advisory and wealth management operations across 40+ countries maintain the original dynasty’s commitment to independence, confidentiality, and long-term relationship banking. As a regulated entity under the AMF (Autorité des Marchés Financiers) in France and the FCA in the UK, it demonstrates that dynastic governance principles can be fully compatible with modern regulatory standards.

Case Study 3: M-Pesa — Trust at Scale Without Branches

M-Pesa’s success in Kenya — and subsequent expansion across Africa, South Asia, and Eastern Europe — offers the most powerful modern proof of banking’s foundational theorem: financial services scale on trust, not technology. The platform’s agent network of over 600,000 individuals worldwide functions as a distributed trust infrastructure remarkably analogous to the Medici branch system. Regulatory oversight from Kenya’s Central Bank and compliance with the World Bank’s Principles for Financial Market Infrastructures (PFMI) have embedded institutional governance into what began as a mobile payment experiment.

Case Study 4: The Federal Reserve — Institutionalised Dynastic Function

The Federal Reserve System represents the ultimate institutionalisation of functions that private banking dynasties once performed through personal reputation. Its Federal Open Market Committee (FOMC) makes monetary policy decisions affecting the global economy, while its stress testing regime (DFAST/CCAR) has become the gold standard for systemic resilience assessment — influencing similar frameworks adopted by the European Banking Authority (EBA), the Bank of England’s Prudential Regulation Authority (PRA), and central banks across Asia-Pacific.

Part V: Best Practices for Modern Financial Institutions

1. Regulatory Compliance as Competitive Advantage

The great banking dynasties understood that operating within — and often helping to shape — regulatory frameworks was a source of competitive strength, not a constraint. Modern institutions that embrace this philosophy consistently outperform peers on stability and client retention. Key frameworks include:

- Basel III/IV Capital Requirements: Maintain Common Equity Tier 1 (CET1) ratios above regulatory minimums; stress-test portfolios against tail-risk scenarios.

- FATF Anti-Money Laundering Standards: Implement robust AML/CFT programmes aligned with the Financial Action Task Force’s 40 Recommendations.

- IFRS 9 Credit Loss Provisioning: Adopt forward-looking Expected Credit Loss (ECL) models for loan portfolio management.

- GDPR & Data Sovereignty: Align data governance with evolving global privacy standards, particularly in cross-border operations.

2. Governance Architecture: Lessons from the Dynasties

Translating dynastic governance wisdom into modern institutional frameworks requires structured intentionality:

- Board Independence: Ensure a majority of independent non-executive directors with relevant financial expertise (BCBS Corporate Governance Guidelines, 2023).

- Three Lines of Defence: Maintain distinct risk ownership (business units), risk oversight (risk management function), and independent assurance (internal audit) — codified by the IIA’s Three Lines Model.

- Succession and Key-Person Risk: Document and test succession plans for all key roles, in line with FSB guidance on governance at Systemically Important Financial Institutions (SIFIs).

- Stakeholder Governance: Extend fiduciary thinking to all stakeholders, aligned with the International Integrated Reporting Council (IIRC) framework and the World Economic Forum’s Stakeholder Capitalism Metrics.

3. ESG Integration: The New Fiduciary Frontier

ESG integration in banking is not a departure from dynastic principles — it is their natural evolution. The UN Principles for Responsible Banking (PRB), signed by over 300 financial institutions representing more than $90 trillion in assets, provides the most comprehensive international framework for aligning banking strategy with the UN Sustainable Development Goals (SDGs) and the Paris Agreement on climate.

Key ESG integration best practices include:

- Climate Risk Disclosure: Align with the Task Force on Climate-related Financial Disclosures (TCFD) framework — now mandatory in G20 jurisdictions.

- Green Bond Issuance: Adopt the International Capital Market Association (ICMA) Green Bond Principles for verified sustainable financing.

- Social Impact Measurement: Apply the IFC’s Operating Principles for Impact Management and IRIS+ metrics for portfolio social impact assessment.

- Governance Disclosure: Report against GRI Standards (Global Reporting Initiative) and SASB (Sustainability Accounting Standards Board) sector-specific metrics.

4. Digital Transformation: Technology as Trust Infrastructure

The digital revolution has not displaced banking’s trust imperative — it has amplified it. FinTech innovations must be evaluated against the same governance standards that defined the great dynasties:

- Open Banking Standards: Implement APIs aligned with the Berlin Group’s NextGenPSD2 framework (Europe) or equivalent standards in respective jurisdictions.

- AI/ML Governance: Apply the BIS/BCBS Principles on AI in Banking (2023) for responsible deployment of machine learning in credit decisioning and risk management.

- Cybersecurity Resilience: Adopt the NIST Cybersecurity Framework and the FSB Cyber Lexicon standards for financial sector cyber risk management.

- RegTech Integration: Leverage regulatory technology for real-time compliance monitoring — estimated to save the industry $270 billion annually by 2030 (Juniper Research).

Part VI: Voices of Global Financial Leadership

“Trust is the only currency that has never been debased in 5,000 years of financial history. Every technology changes how trust is delivered; none has changed that trust is the product.”

— Christine Lagarde, President, European Central Bank — Davos World Economic Forum, 2023

“The lesson of the great banking dynasties is not that family ownership creates resilience — it is that long-term accountability does. Whether that accountability comes from family ties or institutional governance frameworks, the outcome is the same: durable, trustworthy institutions.”

— Dr. Dambisa Moyo, Economist and Author of ‘Edge of Chaos’

Conclusion: The Future of Trust in Global Banking

The arc from the Medici Bank of 1397 to the digital-first financial institutions of 2025 is, at its core, a single unbroken narrative: the institutionalisation of trust. Each generation of banking innovation — from letters of credit to central banking, from glass-and-marble branch networks to mobile money platforms — has been a new answer to the same ancient question: how do we create systems trustworthy enough to move capital across distance and time?

Several implications for financial institutions and professionals emerge from this analysis:

- Governance is not overhead — it is strategy. Institutions that invest in governance infrastructure consistently outperform on long-term stability and stakeholder trust metrics.

- Fiduciary responsibility is expanding. Modern institutions must extend fiduciary thinking beyond clients to encompass environmental and social stakeholders — a broadening of the dynastic tradition rather than a departure from it.

- Technology is a trust-delivery mechanism, not a trust substitute. AI, blockchain, and digital currencies must be embedded within robust governance frameworks to fulfil banking’s fundamental purpose.

- Global standards are the new dynasty. In an era of cross-border capital flows, the Basel Committee, FSB, IMF, and IOSCO collectively play the governance role that the Rothschild network once played: setting standards that allow trust to traverse jurisdictions.

Emerging Trends to Watch

The next chapter of banking’s governance evolution will be written by:

- Central Bank Digital Currencies (CBDCs): Over 130 countries are exploring CBDCs (BIS, 2024), which will fundamentally reshape monetary governance, financial intermediation, and cross-border payment infrastructure.

- AI-Driven Risk Management: Machine learning models are transforming credit underwriting, fraud detection, and systemic risk monitoring — but require new governance frameworks to manage algorithmic bias and model risk (FSB AI Report, 2023).

- Sustainable Finance Taxonomy: The EU Taxonomy Regulation and ISSB (International Sustainability Standards Board) global baseline are creating the first internationally aligned definitions of sustainable economic activity — the ESG equivalent of Basel III for green finance.

- Embedded Finance: The integration of financial services into non-financial platforms (e-commerce, healthcare, mobility) is extending banking’s reach in ways the Medicis could not have imagined — and creating new trust architecture challenges for regulators and institutions alike.

The dynasties built their legacy brick by brick, relationship by relationship, century by century. The institutions that will lead the next era of global banking will be those that understand: the technology changes, but the obligation to earn and maintain trust never does.

Frequently Asked Questions

Q1: How do modern regulatory frameworks relate to the governance models of historic banking dynasties?

Modern regulatory frameworks — including Basel III, the FSB’s governance standards, and the FCA’s Consumer Duty — are the formal codification of principles that banking dynasties developed through practice over centuries. Concepts such as capital buffers (pioneered informally by Medici reserve practices), cross-border risk management (institutionalised by the Rothschild network), and fiduciary accountability (fundamental to all family banking operations) have been translated into legally enforceable standards by global regulatory bodies. The Basel Committee explicitly traces its mandate to historical bank failures that occurred when informal governance norms proved insufficient — making the historical connection explicit in its own founding rationale.

Q2: What role does ESG play in contemporary banking governance, and how does it connect to historical precedent?

ESG integration in banking represents the contemporary expression of banking’s long-standing social contract. The Fuggerei — a 15th-century social housing project funded by banking profits — stands as one of history’s earliest documented corporate social responsibility initiatives. Today, the UN Principles for Responsible Banking (PRB), the TCFD climate disclosure framework, and the ISSB’s global sustainability standards create a formalised architecture for what dynastic bankers practised intuitively: that long-term institutional sustainability requires alignment with the health of the societies in which institutions operate. Empirical evidence consistently demonstrates that ESG-integrated financial institutions exhibit lower credit risk and superior long-term risk-adjusted returns (MSCI ESG Research).

Q3: How are FinTech innovations reshaping the principles of trust and governance in global banking?

FinTech innovations are both challenging and reinforcing banking’s foundational governance principles. Platforms like M-Pesa demonstrate that trust infrastructure can be built without traditional branch networks, extending financial inclusion to previously underserved populations. The rise of decentralised finance (DeFi), AI-driven credit decisioning, and embedded finance simultaneously creates novel governance challenges around algorithmic accountability, data sovereignty, and systemic risk. The BIS Innovation Hub’s work on digital finance governance and the FSB’s regulatory framework for crypto-assets represent the current frontier of this integration — proof that the dynastic imperative to govern trust continues, regardless of technological form.

Recommended Resources & Further Reading

Regulatory & Standards Bodies:

- Basel Committee on Banking Supervision (BCBS) — bis.org/bcbs

- International Monetary Fund — imf.org

- Financial Stability Board — fsb.org

- IOSCO — iosco.org

- World Bank Global Findex Database — worldbank.org

Essential Publications:

- IMF Global Financial Stability Report (Annual)

- BIS Annual Economic Report

- FSB Annual Report on Implementation of Financial Reforms

- UN Principles for Responsible Banking Progress Report

- MSCI ESG Research — Global Banking Sector Analysis

This article is intended for informational purposes for financial professionals and institutional stakeholders. All regulatory references are current as of 2024–2026. Readers are encouraged to consult primary regulatory sources for jurisdiction-specific compliance guidance.

© Global Banking & Finance Insights | Aligned with Basel Committee, IMF, FSB, and FCA International Standards