Introduction: Why Capital Markets Are the Lifeblood of Global Economies

Every thriving economy needs a mechanism to channel savings into productive investment. Capital markets serve precisely this purpose — and at a scale that defines the modern financial world. According to the World Federation of Exchanges (WFE), global equity market capitalisation surpassed $100 trillion in recent years, a figure that underscores the extraordinary depth of today’s interconnected financial system.

At the heart of this ecosystem lies a fundamental question: how do companies access the funding they need to grow, innovate, and compete on a global stage? The answer, for many, is the Initial Public Offering (IPO) — a transformative milestone that converts private ambitions into publicly traded enterprises and simultaneously deepens the liquidity pools available to investors worldwide.

Yet IPOs are only one chapter of the larger capital markets story. Stock exchanges function as liquidity engines, continuously matching buyers and sellers, pricing risk, and allocating capital with a precision that no other mechanism can replicate. For financial institutions, regulators, and investors, understanding how capital markets operate — and how global best practices in listing, disclosure, and secondary market functioning are evolving — is not merely academic. It is operationally and strategically essential.

This article provides a comprehensive, globally oriented exploration of capital markets and IPOs: how they work, why they matter, what the best practices are, and where the future of financial governance and market infrastructure is heading.

Part I: Foundations of Capital Markets

What Are Capital Markets?

Capital markets are financial markets in which long-term debt and equity instruments are bought and sold. They serve as the primary conduit between those who supply capital — individuals, pension funds, sovereign wealth funds, institutional investors — and those who demand it: corporations, governments, and other entities seeking to fund operations, expansion, or public projects.

Capital markets are broadly divided into two segments:

- Primary markets, where new securities are issued for the first time (e.g., through an IPO or a bond issuance).

- Secondary markets, where previously issued securities are traded among investors (e.g., on a stock exchange or over-the-counter platform).

This distinction is more than definitional. It defines how capital flows: primary markets inject new money into the economy; secondary markets ensure that capital remains mobile, liquid, and efficiently priced.

“Capital markets do not merely reflect economic activity — they actively shape it. Efficient markets allocate resources to their highest-valued uses, driving productivity and long-term growth.” — Adapted from principles outlined in IMF Working Papers on financial development

Key Terms Defined

| Term | Definition |

| Financial Intermediation | The process by which financial institutions channel funds from savers (surplus units) to borrowers (deficit units), reducing transaction costs and information asymmetries. |

| Maturity Transformation | The practice of borrowing short-term funds and lending or investing them long-term, a core function of banks and critical to the functioning of capital markets. |

| Fiduciary Responsibility | The legal and ethical obligation of a financial professional or institution to act in the best interest of their clients, underpinning trust in securities markets. |

| Market Liquidity | The ease with which an asset can be bought or sold in the market without significantly affecting its price — a defining quality of healthy capital markets. |

| Price Discovery | The process by which markets aggregate information to determine the fair value of a security, fundamental to capital allocation efficiency. |

| Securities Regulation | The framework of laws and rules — issued by bodies like the SEC (US), FCA (UK), ESMA (EU) — that govern the issuance, trading, and disclosure of securities. |

Part II: Stock Exchanges as Liquidity Engines

The Architecture of a Modern Stock Exchange

A stock exchange is far more than a marketplace. It is a sophisticated financial infrastructure that performs several interdependent functions simultaneously:

- Listing and Admission — Vetting companies that seek public capital and enforcing standards of disclosure and governance.

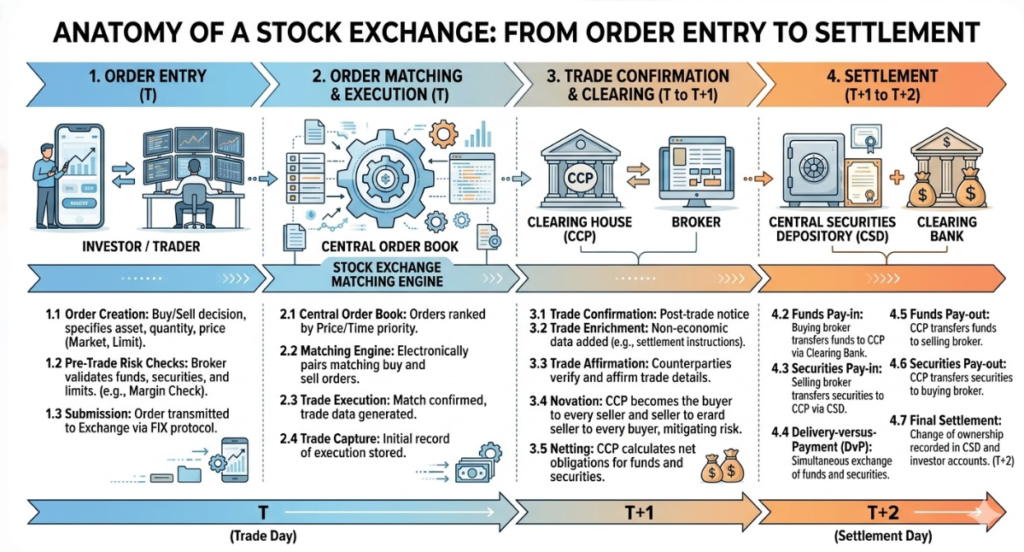

- Trading and Price Discovery — Providing regulated, transparent platforms where buy and sell orders are matched, often in microseconds via electronic order books.

- Clearing and Settlement — Ensuring that completed trades are settled reliably, typically within T+1 or T+2 timelines (moving toward T+0 in many markets).

- Market Surveillance — Monitoring for manipulation, insider trading, and other abuses through real-time analytics.

- Index Compilation — Curating benchmarks (e.g., the S&P 500, MSCI World) used by institutional investors globally.

Anatomy of a Stock Exchange — from Order Entry to Settlement

How Exchanges Generate Liquidity

Liquidity does not emerge spontaneously. Stock exchanges cultivate it through deliberate structural design:

- Market makers and designated liquidity providers commit to continuous two-sided quotations, ensuring buyers and sellers can always transact.

- Continuous versus auction trading models cater to different securities and investor profiles, from ultra-liquid blue chips to less-traded small-cap equities.

- Exchange-traded funds (ETFs) have dramatically deepened liquidity by enabling investors to access diversified baskets of securities in a single trade — a development championed by asset managers like BlackRock, whose iShares platform manages over $3 trillion in ETF assets globally.

- Cross-listings allow companies to list on multiple exchanges (e.g., dual-listing on the London Stock Exchange and the Hong Kong Exchanges and Clearing), broadening their investor base and increasing trading volume.

Global Exchange Landscape: Regional Perspectives

Capital markets are not monolithic. Their structure, regulation, and depth vary significantly across regions:

Americas: Dominated by the NYSE and NASDAQ, the US equity markets represent the world’s deepest pool of capital. The SEC enforces some of the most rigorous disclosure regimes globally, including requirements under the Sarbanes-Oxley Act (SOX) for listed companies.

Europe: Markets operate within the framework of the Markets in Financial Instruments Directive (MiFID II), overseen by national regulators and coordinated by the European Securities and Markets Authority (ESMA). The City of London, despite post-Brexit adjustments, remains a global hub for international bond issuance and foreign equity listings.

Asia-Pacific: Rapid deepening of capital markets in Asia — particularly in Japan, Australia, Singapore, and India — has been supported by regulatory modernisation and growing institutional investor bases. The Shanghai and Shenzhen exchanges now rank among the world’s largest by market capitalisation.

Emerging Markets: The World Bank and International Finance Corporation (IFC) have invested substantially in capital market development in sub-Saharan Africa, Southeast Asia, and Latin America, recognising that deep local capital markets are a prerequisite for sustainable growth and financial inclusion.

“Developing domestic capital markets is one of the most powerful levers for reducing dependence on volatile external capital flows.” — World Bank, Capital Market Development: A Framework for Emerging Economies

Part III: Initial Public Offerings (IPOs) — The Gateway to Public Capital

What Is an IPO?

An Initial Public Offering (IPO) is the process by which a private company offers its shares to the public for the first time, typically via a stock exchange listing. It is simultaneously a capital-raising event, a liquidity event for early investors, a branding milestone, and the beginning of a new governance regime.

The IPO process typically involves:

- Selecting underwriters — Investment banks (e.g., global bulge-bracket firms and boutiques like Rothschild & Co) advise on structure, pricing, and investor outreach.

- Due diligence and documentation — Preparing the prospectus (Registration Statement / Offering Document), which must satisfy the disclosure requirements of the relevant regulator (e.g., SEC Form S-1, FCA Prospectus Rules).

- Roadshow — Management teams present to institutional investors across financial centres — London, New York, Hong Kong, Singapore — to build the order book.

- Bookbuilding and pricing — Demand is assessed and an offer price is set, balancing capital raised with post-listing performance expectations.

- Listing and trading — Shares commence trading on the exchange; the company assumes obligations as a publicly listed entity.

“Global IPO Activity by Region — Volume and Value, 2021–2025 (Source: EY Global IPO Trends Report)”

Global IPO Trends

The IPO market is cyclical, closely tied to equity market valuations, investor sentiment, interest rates, and macroeconomic conditions. Key observations from recent years:

- Technology IPOs have dominated global listings in the past decade, with the Asia-Pacific region — particularly China, South Korea, and India — producing some of the highest-value offerings.

- SPACs (Special Purpose Acquisition Companies) surged and then retreated as a listing mechanism, particularly in US markets, prompting regulatory review by the SEC around disclosure standards.

- Direct Listings have emerged as an alternative pathway, allowing companies to list existing shares without raising new capital or paying traditional underwriting fees — a model notably used by major technology firms.

- ESG-aligned IPOs are increasingly attracting premium valuations, as institutional investors integrate sustainability criteria into investment mandates.

According to EY’s Global IPO Trends 2024, while global IPO volumes moderated in 2023 amid rate tightening cycles, markets in South Asia and the Middle East demonstrated remarkable resilience, reflecting diversification in the global capital markets architecture.

Best Practices in IPO Preparation

1. Governance Readiness Companies must transition from entrepreneurial governance structures to board-level oversight consistent with public market expectations. This includes:

- Establishing independent audit, remuneration, and nomination committees.

- Adopting governance codes aligned with international standards (e.g., the UK Corporate Governance Code, OECD Principles of Corporate Governance).

- Ensuring senior management has clearly delineated fiduciary responsibilities.

2. Financial Reporting Standards Global capital markets expect financial statements prepared under recognised accounting frameworks:

- IFRS (International Financial Reporting Standards) — adopted by over 140 countries and required for listings on most major exchanges outside the US.

- US GAAP — required for companies listed on US exchanges.

- Reconciliation disclosures — often required for dual-listed entities.

3. Disclosure Quality Investors and regulators demand transparent, material, and timely disclosure. Best practice includes:

- Risk factors articulated with specificity, not boilerplate language.

- Management Discussion & Analysis (MD&A) that gives genuine insight into operational performance drivers.

- Related-party transactions disclosed with rigour.

- Forward-looking statements accompanied by robust caveats.

4. ESG Integration Increasingly, IPO candidates are expected to present credible Environmental, Social, and Governance (ESG) frameworks. Institutional investors — including many of the world’s largest asset managers — now incorporate ESG scores into IPO allocation decisions. Reference frameworks include:

- GRI (Global Reporting Initiative) Standards

- TCFD (Task Force on Climate-related Financial Disclosures) Recommendations

- ISSB (International Sustainability Standards Board) Standards — now integrated into IFRS reporting for many jurisdictions

Part IV: Secondary Market Excellence — Best Practices in Market Functioning

The Importance of Secondary Markets

The existence of a robust secondary market is not peripheral to the IPO process — it is foundational to it. Investors participate in IPOs in part because they know they can exit their positions in a liquid secondary market. Without this confidence, primary market activity would atrophy.

Secondary markets serve five core functions:

- Continuous liquidity — enabling investors to rebalance portfolios in response to changing conditions.

- Price discovery — aggregating dispersed information into observable prices.

- Risk transfer — allowing investors to hedge exposures through derivatives and structured products.

- Corporate governance signalling — stock price performance provides management with market-based feedback.

- Benchmark creation — secondary market prices underpin indices, fund valuations, and regulatory capital calculations.

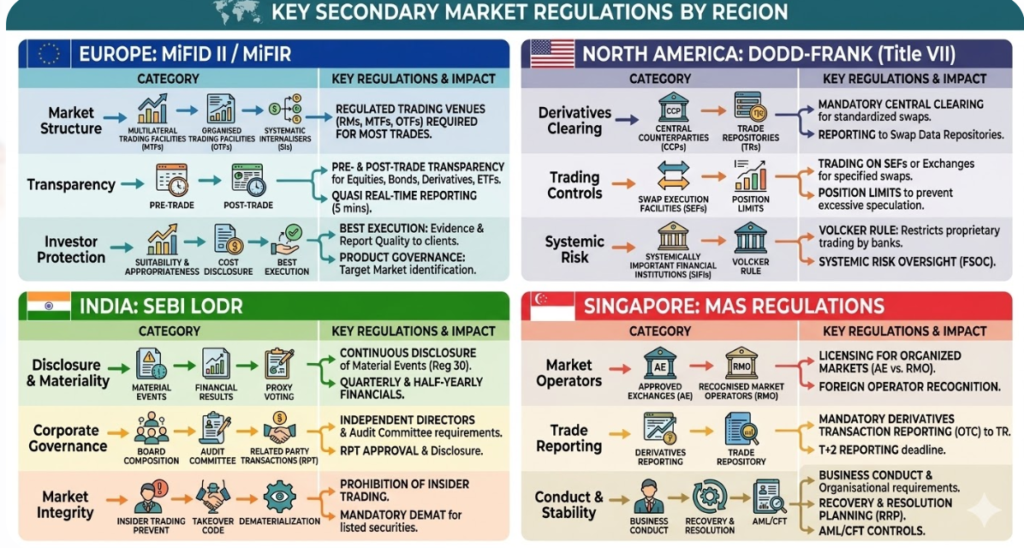

Regulatory Frameworks Governing Secondary Markets

Sound secondary market functioning depends on an integrated regulatory architecture. Key pillars include:

Market Integrity

- Prohibition of insider trading — a universal standard enforced by virtually every major securities regulator.

- Market manipulation rules — prohibiting practices such as spoofing, layering, and wash trading, with digital surveillance tools increasingly deployed by exchanges and regulators.

- Short-selling regulations — ranging from disclosure requirements to temporary restrictions during periods of market stress, as seen during the COVID-19 crisis.

Transparency and Reporting

- Pre- and post-trade transparency — requirements, such as those under MiFID II in Europe, mandate publication of quotes and executed trades.

- Transaction reporting — regulators require detailed trade data to monitor systemic risk and detect abuse.

Market Infrastructure

- Central Counterparty Clearing (CCPs) — reduce counterparty risk by interposing between buyer and seller; regulated under frameworks like the European Market Infrastructure Regulation (EMIR) and the Dodd-Frank Act (US).

- Central Securities Depositories (CSDs) — hold securities in dematerialised form and manage settlement; subject to international standards set by the Committee on Payments and Market Infrastructures (CPMI) and IOSCO.

Key Secondary Market Regulations by Region — MiFID II, Dodd-Frank, SEBI LODR, MAS Regulations

FinTech’s Transformation of Secondary Markets

FinTech innovation is reshaping how secondary markets operate across multiple dimensions:

Algorithmic and High-Frequency Trading (HFT): Automated strategies now account for a significant proportion of trading volume on major exchanges, improving liquidity but also raising questions about market stability. Regulators globally — including the SEC, ESMA, and the Financial Conduct Authority (FCA) — have introduced frameworks requiring HFT firms to register and maintain risk controls.

Distributed Ledger Technology (DLT) and Tokenisation: Several exchanges and central banks are piloting DLT-based settlement infrastructure. The BIS (Bank for International Settlements) has conducted extensive research through its Innovation Hub on how tokenised securities could shorten settlement cycles to near-instantaneous. Early use cases include tokenised government bonds and equity-like instruments on regulated platforms.

Artificial Intelligence in Surveillance: AI-powered surveillance systems are being deployed by exchanges and regulators to detect anomalous trading patterns with greater speed and accuracy than rule-based systems. The FCA in the UK has been a noted pioneer in RegTech adoption, including AI-driven supervisory tools.

Retail Investor Platforms: Commission-free trading platforms and fractional share programmes have dramatically lowered the barriers to secondary market participation, broadening financial inclusion. However, they have also raised questions about gamification and investor protection, prompting regulatory reviews in multiple jurisdictions.

Part V: ESG Integration in Capital Markets — From Aspiration to Architecture

The ESG Imperative

Environmental, Social, and Governance considerations have moved from the periphery to the centre of global finance standards in capital markets. This shift is structural, not cyclical. Several converging forces are driving it:

- Institutional investors representing tens of trillions in assets under management have signed the UN Principles for Responsible Investment (PRI), committing to ESG integration.

- Regulatory mandates — including the EU’s Sustainable Finance Disclosure Regulation (SFDR) and the EU Taxonomy — require disclosure of sustainability risks and impacts.

- Climate risk has been formally recognised as a financial stability risk by central banks and the Financial Stability Board (FSB), elevating it beyond corporate reporting into systemic risk management.

ESG in IPOs and Listings

The integration of ESG in the IPO process is accelerating:

- Pre-IPO ESG audits are becoming standard, as underwriters and institutional investors demand evidence of credible sustainability strategies before capital allocation.

- Green and sustainability-linked bonds — issued under frameworks aligned with the ICMA Green Bond Principles — offer an ESG-specific capital raising pathway that complements equity offerings.

- Stock exchanges are increasingly mandating ESG disclosures. The London Stock Exchange, SGX (Singapore Exchange), and Nasdaq have all introduced ESG reporting requirements for listed companies.

“The integration of sustainability into capital markets is not just an ethical choice — it is a risk management imperative. Climate-related financial risks are material risks, and markets must price them accordingly.” — Adapted from FSB Task Force on Climate-Related Financial Disclosures (TCFD), Final Report

Case Study: Green Bond Issuance — A Global Finance Standard in Action

The global green bond market illustrates how capital markets can be deliberately structured to channel funds to sustainable uses. Issuers — ranging from sovereign governments to multilateral development banks to corporate entities — issue green bonds under defined frameworks, with proceeds ring-fenced for qualifying projects (renewable energy, clean transportation, sustainable water management).

The International Capital Market Association (ICMA) Green Bond Principles provide the voluntary framework underpinning this market, which surpassed $500 billion in annual issuance. This market exemplifies how global finance standards can mobilise private capital at scale for public good — a model increasingly referenced by the World Bank and IMF in their sustainable development financing strategies.

Part VI: Digital Transformation and the Future of Capital Markets

Technology as Structural Disruptor

The convergence of technology and capital markets is producing structural changes that will define the industry for decades. Key themes include:

1. Digital Asset Markets and Tokenisation The tokenisation of real-world assets — including equities, bonds, real estate, and commodities — onto blockchain-based platforms represents a potentially transformative shift in market infrastructure. If realised at scale, tokenisation could:

- Eliminate intermediary layers, reducing costs.

- Enable 24/7 settlement, removing the overnight risk inherent in T+1/T+2 cycles.

- Open access to previously illiquid assets for a broader range of investors.

- Facilitate programmable compliance through smart contracts enforcing regulatory rules automatically.

Several major financial institutions and exchanges are actively piloting tokenised securities platforms, with regulatory sandboxes in Singapore (MAS), the UK (FCA), and the EU providing structured environments for experimentation.

2. AI in Capital Markets Artificial Intelligence is being deployed across the capital markets value chain:

- Investment research — AI models scanning and synthesising vast datasets to generate investment signals.

- Risk management — Real-time AI monitoring of portfolio exposures and tail risks.

- Regulatory compliance — Automated interpretation of regulatory changes and compliance mapping.

- Fraud detection — AI-powered surveillance for market abuse and financial crime.

The Basel Committee on Banking Supervision (BCBS) has highlighted both the opportunities and risks of AI adoption in financial institutions, emphasising the need for model governance, explainability, and auditability.

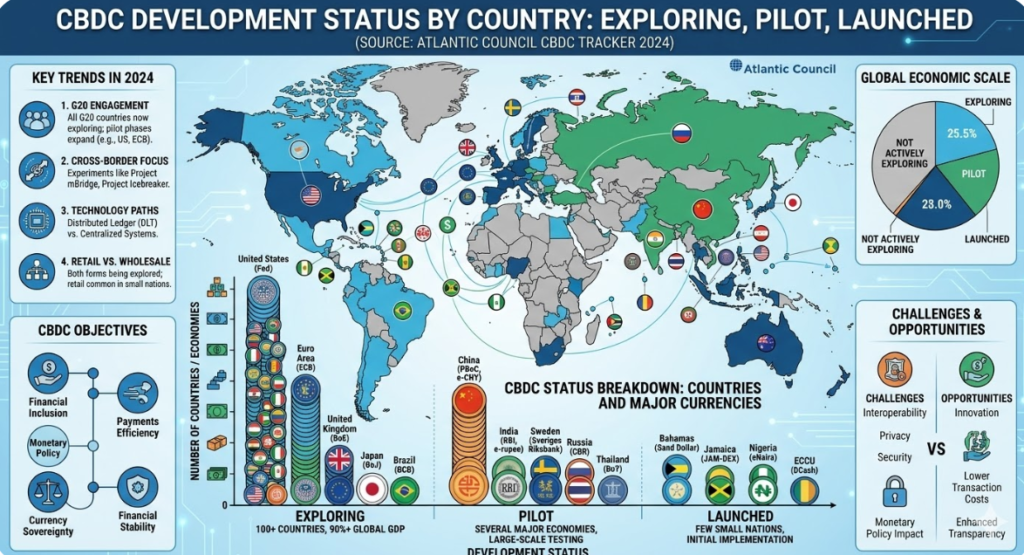

3. Central Bank Digital Currencies (CBDCs) and Market Infrastructure Over 130 countries are now exploring CBDCs, according to the Atlantic Council CBDC Tracker. Their potential impact on capital markets is significant: wholesale CBDCs could transform settlement infrastructure, enabling atomic delivery-versus-payment (DvP) for securities transactions, eliminating settlement risk entirely.

“CBDC Development Status by Country — Exploring, Pilot, Launched (Source: Atlantic Council CBDC Tracker 2024

4. FinTech and Democratised Market Access The model represented by platforms like M-Pesa in financial inclusion — using mobile technology to reach previously unbanked populations — is being extended into capital markets through mobile-first investment platforms. In markets like India, Kenya, and Indonesia, retail participation in equity markets has grown dramatically through digital platforms, reshaping the secondary market participant base and deepening liquidity.

Part VII: Risk Management in Capital Markets — The Regulatory Foundation

Capital Requirements and Market Risk

Capital markets activity generates exposures that must be managed within rigorous frameworks. The Basel Committee on Banking Supervision has, through successive accords (Basel I, II, III, and the ongoing refinements toward “Basel IV”), established global minimum standards for the capital that banks must hold against their market risk exposures.

Key components include:

- Value at Risk (VaR) and Expected Shortfall (ES) — statistical measures of potential loss, required under the Fundamental Review of the Trading Book (FRTB).

- Stress testing — both internal (ICAAP) and supervisory (e.g., EBA stress tests in Europe, Fed DFAST/CCAR in the US).

- Liquidity Coverage Ratio (LCR) and Net Stable Funding Ratio (NSFR) — Basel III requirements ensuring banks maintain adequate liquidity buffers.

“Basel III Capital Framework — Tier 1, Tier 2 Capital, Leverage Ratio, LCR, NSFR”

Systemic Risk Oversight

Beyond individual institution resilience, capital markets require systemic risk oversight:

- Financial Stability Board (FSB) — coordinates global macroprudential policy and monitors cross-border systemic risks.

- International Organization of Securities Commissions (IOSCO) — sets global standards for securities regulation and market oversight.

- Global Systemically Important Banks (G-SIBs) — subject to enhanced capital surcharges, resolution planning, and supervisory intensity.

The interconnected nature of global capital markets means that stress in one centre — as demonstrated during the 2008 Global Financial Crisis, the COVID-19 shock, and the 2023 banking sector turbulence — can propagate rapidly across borders, underscoring the necessity of coordinated international regulatory governance.

Conclusion: The Capital Markets Imperative for Financial Institutions

Capital markets stand at the intersection of economic ambition and financial reality. They transform private savings into public companies, channel long-term investment into productive assets, and provide the price signals that guide resource allocation across the global economy.

For financial institutions operating in this space — whether as underwriters, exchanges, custodians, or investors — the key imperatives are clear:

- Governance must lead. Fiduciary responsibility and independent oversight are the non-negotiable foundations of investor trust and market integrity.

- Disclosure must be genuine. Material, timely, and transparent disclosure — not compliance-driven boilerplate — is the currency of capital market credibility.

- ESG integration is structural. Sustainability is no longer a reporting exercise but a risk management, capital allocation, and strategic positioning imperative.

- Technology must be governed. FinTech innovation — from AI to DLT — offers transformative opportunities but demands proportionate regulatory oversight and robust model governance.

- Inclusion must be intentional. Expanding access to capital markets — for retail investors, SMEs, and participants in emerging economies — requires deliberate design, not incidental outcomes.

Looking ahead, the capital markets landscape will be shaped by the convergence of digital transformation, climate finance imperatives, geopolitical reconfigurations of capital flows, and the deepening of multilateral regulatory coordination. Institutions that embed these trends into their strategic frameworks — rather than treating them as external constraints — will be best positioned to fuel, and benefit from, the next chapter of global growth.

FAQ: Capital Markets and IPOs

Q1: What is the difference between a primary and secondary capital market? The primary market is where new securities are created and sold for the first time — for example, through an IPO or a bond issuance. Proceeds go directly to the issuing company or government. The secondary market is where investors subsequently buy and sell those already-issued securities among themselves. Price discovery and liquidity are the secondary market’s primary contributions; the issuer does not receive funds from secondary market transactions.

Q2: How do global regulatory standards affect IPO readiness? Companies planning to list on international exchanges must meet the disclosure and governance standards of the relevant regulator — whether the SEC in the US, the FCA in the UK, ESMA across the EU, or equivalent bodies in Asia-Pacific. These standards typically encompass financial reporting (IFRS or US GAAP), corporate governance (independent board committees, codes of conduct), and ongoing disclosure obligations (material events, related-party transactions). Non-compliance not only risks regulatory sanction but materially undermines investor confidence and IPO valuation.

Q3: How is ESG changing the IPO landscape for companies and investors? ESG considerations are now embedded across the IPO lifecycle. Pre-IPO, companies are expected to demonstrate credible sustainability strategies, assessed by institutional investors using frameworks like the GRI, TCFD, and ISSB standards. At listing, exchanges in major markets require or incentivise ESG reporting. Post-listing, ESG ratings — from agencies like MSCI ESG, Sustainalytics, and CDP — influence index inclusion, institutional allocation, and ultimately, valuation multiples. For investors, ESG integration represents both a risk management discipline and, increasingly, a fiduciary obligation under evolving regulatory frameworks.

Further Reading and External Resources

- Basel Committee on Banking Supervision Publications

- IMF Working Papers on Financial Markets and Capital Flows

- World Bank Capital Markets Development

- IOSCO Standards and Research

- FSB — Financial Stability Board Reports

- ICMA Green Bond Principles

- EY Global IPO Trends Reports

- UN Principles for Responsible Investment

This article reflects global best practices and publicly available information as of 2025. It is intended for professional and semi-professional audiences in banking, finance, and investment management. It does not constitute investment or legal advice.