Introduction: The Architecture of National Financial Resilience

“A nation’s wealth is not measured solely by what it produces, but by how wisely it saves, invests, and governs its financial assets across generations.” — Adapted from IMF Fiscal Monitor, 2023

When Norway’s Government Pension Fund Global surpassed $1.7 trillion in assets under management in 2024, it sent a powerful signal to the world: disciplined national savings, backed by sound financial governance and transparent investment mandates, can transform a finite natural resource windfall into perpetual intergenerational wealth.

This is the promise — and the complexity — at the heart of sovereign wealth management.

From the gilded vaults of central banks to the digital platforms of retail savings programs, governments worldwide are navigating a shared challenge: how to mobilize, protect, and grow national savings in an era of rising public debt, climate risk, geopolitical volatility, and digital disruption. The instruments they deploy — government securities, sovereign wealth funds (SWFs), national savings schemes, and risk-free instruments — form the backbone of both domestic financial systems and global capital markets.

This article examines how the world’s leading economies approach sovereign wealth and national savings, compares key instruments across jurisdictions, evaluates global best practices in financial governance and risk management, and offers a forward-looking perspective on the emerging trends reshaping the field.

Whether you are a financial professional, institutional investor, policy analyst, or informed citizen, understanding these mechanisms is essential — because sovereign finance ultimately affects every interest rate, every pension, and every public service you rely on.

Part I: Defining the Landscape — Key Concepts in Sovereign Finance

What Are Government Securities?

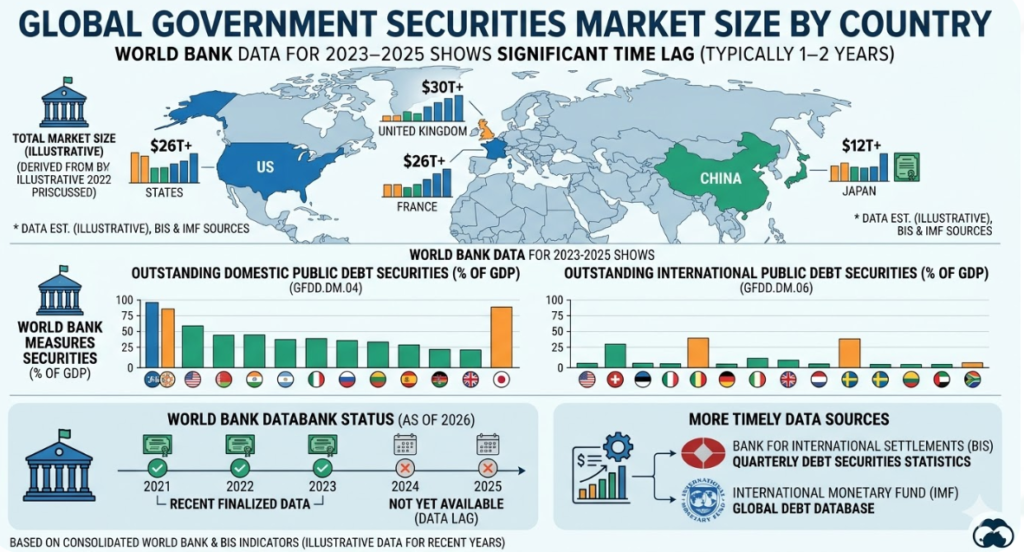

Government securities are debt instruments issued by a national government to finance public expenditure and manage national debt. They are considered risk-free instruments in conventional financial theory — that is, they carry no default risk in domestic currency terms (though inflation, currency, and reinvestment risks remain).

Key types include:

- Treasury Bills (T-Bills): Short-term instruments (typically 4–52 weeks), sold at a discount and redeemed at face value. Used heavily in the US Treasury market — the world’s largest and most liquid government securities market.

- Treasury Notes & Bonds: Medium- to long-term instruments (2–30 years) paying semi-annual coupon interest. The benchmark for global risk-free rate pricing.

- Index-Linked/Inflation-Protected Securities: Instruments whose principal is adjusted by inflation (e.g., US Treasury Inflation-Protected Securities — TIPS; UK Index-Linked Gilts).

- Sovereign Sukuk: Sharia-compliant sovereign debt instruments widely issued across Gulf Cooperation Council (GCC) nations, Malaysia, and Indonesia, structured around tangible asset-backed returns rather than interest.

Global Government Securities Market Size by Country — World Bank data, 2023

What Is a Sovereign Wealth Fund?

A Sovereign Wealth Fund (SWF) is a state-owned investment fund or entity, established from balance-of-payments surpluses, official foreign currency reserves, fiscal surpluses, or receipts from commodity exports. Unlike central bank reserves, SWFs invest in a broader range of assets — equities, real estate, private equity, infrastructure, and increasingly, ESG-aligned assets.

The Santiago Principles (Generally Accepted Principles and Practices, or GAPPs), developed under the International Working Group of Sovereign Wealth Funds and endorsed by the IMF, provide the foundational governance framework for SWFs globally — addressing transparency, accountability, investment policies, and risk management.

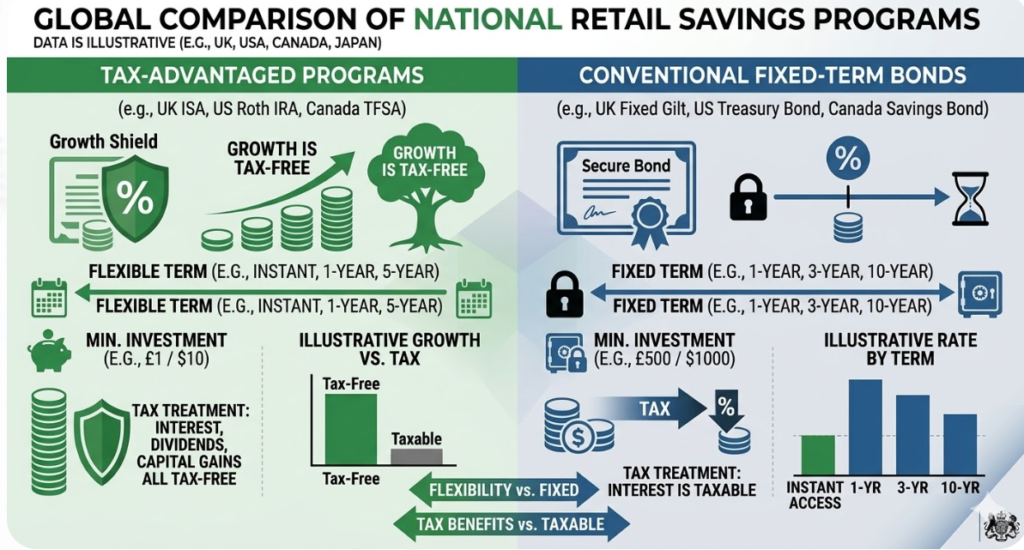

National Savings Programs: Retail-Facing Instruments

National savings programs are government-backed retail savings products designed to offer citizens a safe, accessible vehicle for savings, often with preferential tax treatment. Examples include:

- US Series I Savings Bonds (inflation-linked, direct-to-consumer via TreasuryDirect)

- UK Premium Bonds (lottery-linked, NS&I managed)

- Indian National Savings Certificates (NSC)

- Japanese Government Bonds for Retail (JGB-R)

These programs serve a dual purpose: mobilizing domestic savings for sovereign financing needs while advancing financial inclusion for retail investors.

Financial Intermediation and Maturity Transformation

Financial intermediation refers to the process by which financial institutions channel funds from savers (surplus units) to borrowers (deficit units). In the sovereign context, governments act as the ultimate intermediary, borrowing short from retail savers and markets while investing long in infrastructure, social programs, and sovereign assets.

Maturity transformation — the process of funding long-term assets with short-term liabilities — is the core function of this intermediation. Central banks, through open market operations and reserve management, actively manage the risks this creates. The Basel Committee on Banking Supervision has developed frameworks (notably Basel III’s Net Stable Funding Ratio and Liquidity Coverage Ratio) that govern how banks handle maturity mismatch — principles that increasingly inform sovereign debt management best practices.

Part II: A Global Comparative Analysis — Instruments and Approaches

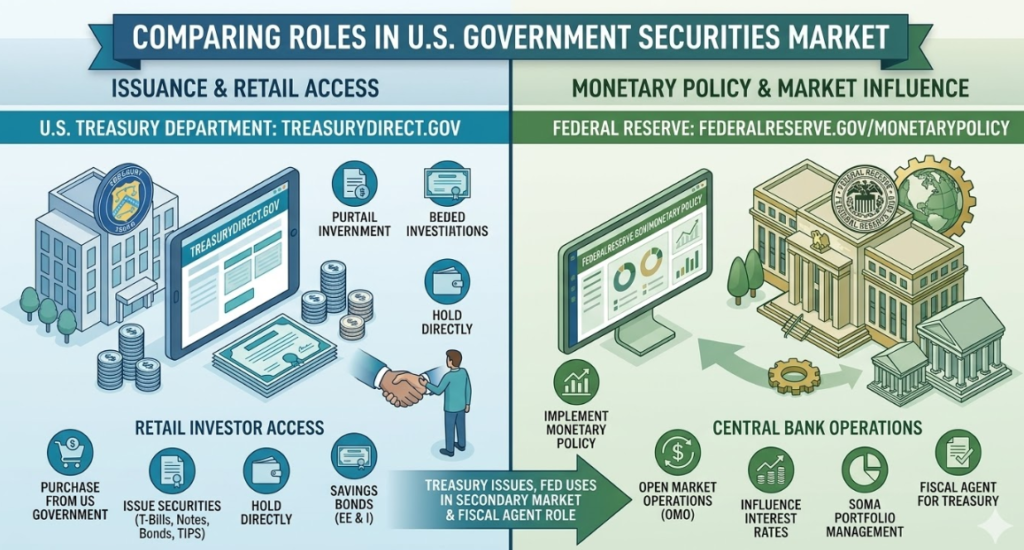

US Treasuries: The Global Reserve Benchmark

The US Treasury market is the world’s deepest, most liquid fixed-income market, with over $27 trillion in outstanding securities as of 2024 (US Treasury Department). US Treasuries serve as the global risk-free benchmark, underpinning the pricing of virtually every credit instrument worldwide.

Key features:

- Issued by the US Department of the Treasury via the Bureau of the Fiscal Service

- Primary distribution through regular auction cycles (weekly for bills; monthly for notes and bonds)

- Held globally by foreign governments, central banks, institutional investors, and retail savers

- The Federal Reserve’s open market operations in Treasuries are the primary mechanism for US monetary policy transmission

Why it matters globally: The US 10-year Treasury yield is the single most referenced risk-free rate in international finance. Its movements ripple through mortgage rates in São Paulo, corporate bond spreads in Frankfurt, and equity valuations in Singapore.

US Treasury Department — TreasuryDirect.gov; Federal Reserve — FederalReserve.gov/monetarypolicy

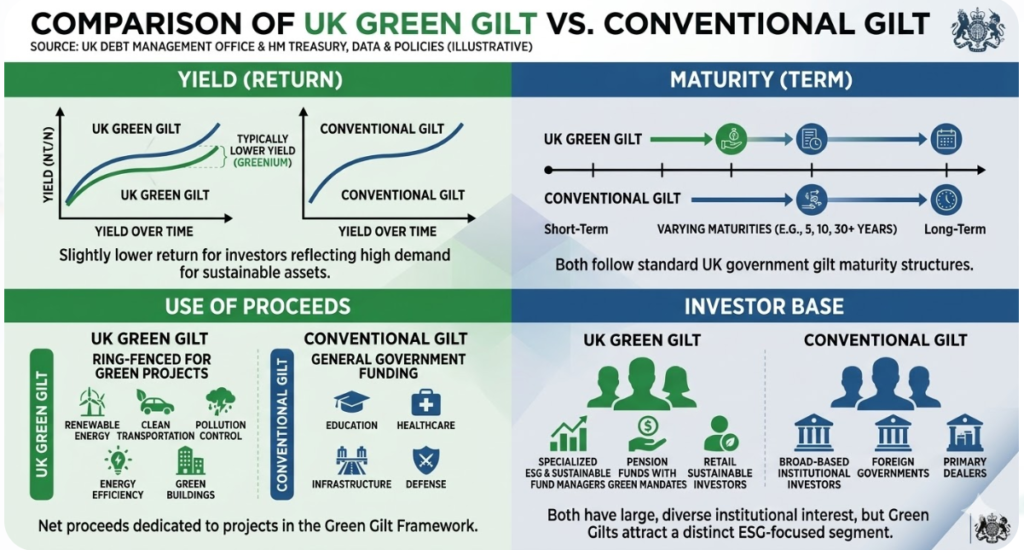

UK Gilts: History, Depth, and Innovation

UK Gilts (so named for their original gilt-edged paper certificates) represent one of the world’s oldest continuous sovereign debt markets, with origins in the late 17th century. Managed by the UK Debt Management Office (DMO) on behalf of HM Treasury, the Gilt market offers:

- Conventional Gilts (fixed coupon, fixed maturity)

- Index-Linked Gilts (principal linked to the UK Retail Prices Index — RPI)

- Green Gilts (sovereign green bonds, first issued in 2021, proceeds allocated to eligible green expenditures)

The Financial Conduct Authority (FCA) oversees market integrity in UK Gilts trading, while the Bank of England’s Asset Purchase Facility has, at various times, held significant portions of the Gilt market as part of quantitative easing programs.

Case Study — Green Gilts: The UK’s issuance of Green Gilts represents a landmark in ESG-aligned sovereign debt. By earmarking proceeds for renewable energy, clean transportation, and climate adaptation, the UK has created a replicable model for sovereigns seeking to align their liability management with environmental governance objectives. By 2023, the UK had issued over £30 billion in Green Gilts, establishing one of the largest sovereign green bond programs globally.

Comparison of UK Green Gilt vs. Conventional Gilt — Yield, Maturity, Use of Proceeds, Investor Base

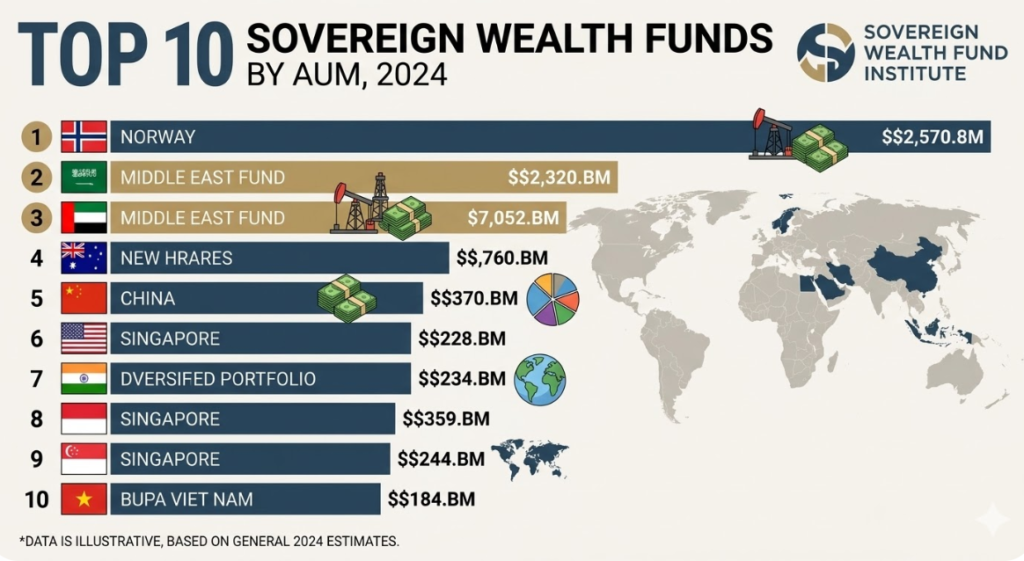

The Global Sovereign Wealth Fund Landscape

The Sovereign Wealth Fund Institute tracks over 100 SWFs globally, with combined assets exceeding $11 trillion. These funds vary enormously in mandate, governance, and investment philosophy.

Norway: The Gold Standard of SWF Governance

Norges Bank Investment Management (NBIM), which manages the Government Pension Fund Global (GPFG), is universally regarded as the benchmark for SWF governance and transparency. Key features:

- Clear fiscal rule: only 3% of the fund’s value may be drawn annually (long-run real return expectation)

- Full public disclosure of all holdings, returns, and governance decisions

- Robust ESG integration: the fund has divested from hundreds of companies on ethical grounds, including tobacco producers, weapons manufacturers, and severe environmental violators

- Independent Council on Ethics that advises on exclusions — a model for fiduciary responsibility aligned with long-term societal interests

“The Fund’s purpose is to ensure responsible and long-term management of revenues from Norway’s oil and gas resources, so that this wealth benefits both current and future generations.” — Norges Bank Investment Management, Annual Report

Singapore: Strategic and Commercial SWFs

Singapore operates two distinct SWFs with different mandates:

- GIC Private Limited — Manages Singapore’s foreign reserves with a long-term, risk-adjusted return objective. Invests across 40+ countries in equities, fixed income, real estate, and infrastructure.

- Temasek Holdings — Operates as a commercial investment company, holding stakes in major global corporations. Uniquely, Temasek publishes a rigorous annual report including its Total Shareholder Return (TSR) since inception.

Singapore’s dual-SWF model demonstrates how financial governance can serve both macroeconomic stability (GIC) and strategic national interest (Temasek) simultaneously.

Gulf SWFs: Commodity Wealth Diversification

The Gulf Cooperation Council nations have established some of the world’s largest SWFs as part of deliberate economic diversification strategies away from hydrocarbon dependency:

- Abu Dhabi Investment Authority (ADIA) — Estimated $900+ billion AUM; one of the world’s oldest and largest SWFs

- Kuwait Investment Authority (KIA) — The world’s first SWF (est. 1953), managing the Kuwait Future Generations Fund

- Saudi Arabia’s Public Investment Fund (PIF) — Rapidly expanding toward a $2 trillion target, executing Vision 2030’s domestic and international diversification agenda

These funds have progressively adopted international finance best practices, including alignment with the Santiago Principles and increasing ESG disclosures, under pressure from global institutional co-investors and international governance bodies.

Top 10 SWFs by AUM — Sovereign Wealth Fund Institute, 2024

China’s Sovereign Asset Ecosystem

China’s approach to sovereign wealth is multifaceted, operating through several distinct vehicles:

- China Investment Corporation (CIC) — China’s primary SWF, managing approximately $1.35 trillion

- State Administration of Foreign Exchange (SAFE) — Manages China’s foreign exchange reserves (the world’s largest at ~$3.2 trillion)

- National Social Security Fund (NSSF) — Manages China’s pension reserve assets

China’s model reflects a hybrid state-directed capitalism approach where sovereign financial assets serve both macroeconomic stabilization and strategic industrial policy objectives — a model that increasingly draws scrutiny from IMF governance assessments and bilateral investment frameworks.

Part III: National Savings Programs — Mobilizing the Retail Saver

The Role of Retail Savings in Sovereign Finance

Retail savings programs fulfill a critical function in financial inclusion and sovereign liability management. By directly connecting citizens to government securities, they:

- Broaden the investor base for sovereign debt, reducing dependence on volatile foreign capital

- Offer citizens a safe harbor during market turbulence

- Advance financial literacy and capital formation at the household level

- Provide sovereigns with a stable, patient pool of domestic funding

Global Models in Retail Sovereign Savings

| Program | Country | Instrument Type | Key Feature |

| TreasuryDirect | United States | T-Bills, Notes, Bonds, I-Bonds | Direct online purchase, no intermediary fee |

| NS&I Premium Bonds | United Kingdom | Lottery-linked savings | Tax-free prize draws instead of interest |

| Sukuk Ritel | Indonesia | Retail Sovereign Sukuk | Sharia-compliant, micro-denomination |

| JGB for Retail | Japan | 3/5/10-year retail bonds | Minimum purchase ¥10,000; capital guaranteed |

| Retail Savings Bonds | South Africa | Variable/fixed rate bonds | Targeted at unbanked populations via post offices |

Comparison of Key National Retail Savings Programs — Rate, Term, Min. Investment, Tax Treatment

Digital Transformation in Retail Savings: The FinTech Dimension

The digital transformation of national savings programs is one of the most consequential trends in retail sovereign finance. Key developments include:

- M-Pesa and mobile money integration: In Kenya and several Sub-Saharan African nations, mobile money platforms have been integrated with government savings programs, enabling unbanked citizens to purchase government securities directly via mobile phone — a breakthrough for financial inclusion aligned with World Bank development objectives.

- Blockchain-based bond issuance: The World Bank’s bond-i (Blockchain Operated New Debt Instrument), issued in 2018, was the first bond created, allocated, transferred, and managed using distributed ledger technology — a proof of concept for digital sovereign debt infrastructure.

- Digital savings wallets: Several central banks, under CBDC (Central Bank Digital Currency) pilot programs, are exploring the integration of sovereign savings products into digital currency wallets, blurring the line between payments infrastructure and savings vehicles.

Part IV: Financial Governance — Standards, Regulation, and Best Practices

The Santiago Principles: Global Governance for SWFs

The 24 Santiago Principles, formally titled Generally Accepted Principles and Practices (GAPPs), represent the most authoritative global governance standard for SWFs. Adopted in 2008 by the International Forum of Sovereign Wealth Funds (IFSWF) with IMF support, they address:

- Legal framework and institutional structure: SWFs should have a clear legal basis and sound governance structure

- Accountability and transparency: Regular public disclosure of investment objectives, risk management, and performance

- Investment and risk management framework: Prudent investment policies with defined risk tolerance and diversification mandates

- Relationship with owner: Clear definition of the fund’s liability to the government and separation from monetary policy operations

Compliance with the Santiago Principles is voluntary but has become a de facto prerequisite for SWFs seeking to invest in jurisdictions with robust foreign investment screening regimes (e.g., CFIUS in the United States, NSI Act in the United Kingdom).

Basel Committee Standards and Sovereign Debt

The Basel Committee on Banking Supervision — operating under the auspices of the Bank for International Settlements (BIS) — has directly shaped how banks hold and value sovereign debt:

- Basel III’s Standardised Approach: Assigns risk weights to sovereign exposures based on external credit ratings, with OECD country debt historically receiving preferential (0%) risk weight treatment

- Concentration risk guidance: Encourages banks to avoid excessive concentration in single sovereign exposures — a lesson drawn from the European Sovereign Debt Crisis of 2010–2015, when peripheral eurozone government bond spreads collapsed the “risk-free” assumption for sovereign debt

- Liquidity standards (LCR/NSFR): High-quality government securities form the core of High Quality Liquid Assets (HQLA), cementing their systemic role in bank liquidity management

Basel Committee — BIS.org/bcbs IMF Government Finance Statistics Manual

ESG Integration in Sovereign Debt and SWF Management

Environmental, Social, and Governance (ESG) considerations have moved from the periphery to the core of sovereign finance in the past decade. Key developments:

On the SWF side:

- Norway’s GPFG exclusion framework (coal, tobacco, severe human rights violations) has influenced SWF governance globally

- The One Planet SWF Framework (launched at the One Planet Summit, 2017) commits signatory SWFs to integrating climate change considerations into investment decision-making

- Temasek’s net-zero commitment by 2050 (with a 2030 interim target) demonstrates commercial SWF alignment with the Paris Agreement

On the sovereign debt side:

- Green Bonds (UK, Germany, France, Canada) earmark proceeds for climate projects

- Sustainability-Linked Bonds (SLBs): Sovereign bonds where coupon rates are tied to the issuer government achieving defined sustainability KPIs (pioneered by Chile and Uruguay)

- IMF’s Resilience and Sustainability Trust (RST): A facility enabling vulnerable member countries to address long-term structural challenges including climate change — embedding ESG into the IMF’s lending architecture

“Sovereign wealth funds that ignore ESG are essentially discounting the risk of the world they will inherit. Long-term capital must reflect long-term realities.” — Adapted from IFSWF 2022 Annual Review

Part V: Risk Management in Sovereign Finance

Defining the Risk Matrix

Sovereign wealth and savings instruments face a distinctive risk matrix that differs from corporate finance:

- Credit/Default Risk: Theoretically low for domestic currency debt, but real for foreign currency obligations (e.g., Sri Lanka, Zambia, Argentina default experiences)

- Interest Rate Risk: Duration mismatch between long-dated bonds and short-term funding sources

- Currency Risk: SWFs investing globally carry significant foreign exchange exposure

- Geopolitical Risk: Sanctions, market access restrictions, and asset freezing (Russia’s foreign reserve freeze in 2022 reset assumptions about sovereign asset safety)

- Liquidity Risk: Even deep markets (US Treasuries) experienced alarming liquidity deterioration in March 2020, prompting unprecedented Federal Reserve intervention

- ESG/Stranded Asset Risk: Increasing recognition that carbon-intensive investments may lose value as transition policies accelerate

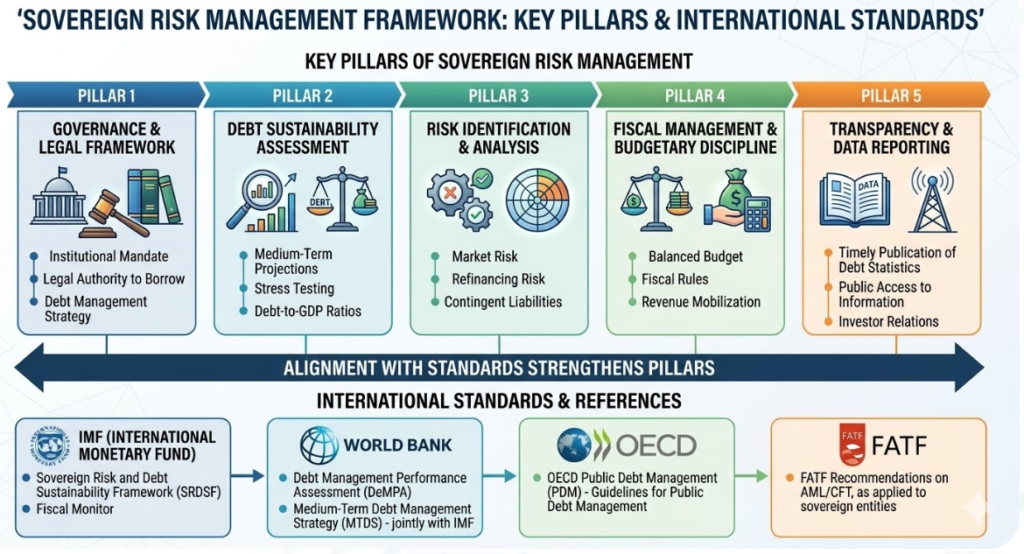

Best Practices in Sovereign Risk Management

Leading sovereign finance institutions apply several internationally recognized best practices:

- Strategic Asset Allocation (SAA) with regular review: Norway’s GPFG, GIC, and ADIA all maintain formal SAA processes, periodically stress-tested against macroeconomic scenarios

- Liability-Driven Investment (LDI): Matching asset duration and cash flows to known government liabilities — a practice mandated by the IMF’s Debt Management Guidelines

- Diversification across geographies, asset classes, and currencies: The Santiago Principles explicitly support this principle for SWFs

- Independent risk oversight: Separation between investment management and risk control functions — aligned with Basel Committee’s principles for sound internal governance

- Scenario analysis and stress testing: Mandatory under IMF’s Debt Sustainability Analysis (DSA) framework for sovereign debt managers

- Transparent reporting aligned with international standards: Adoption of IPSAS (International Public Sector Accounting Standards) or equivalent for sovereign fund reporting

Sovereign Risk Management Framework — Key Pillars and International Standards References

Part VI: Emerging Trends Reshaping Sovereign Wealth and National Savings

1. Central Bank Digital Currencies (CBDCs) and Sovereign Savings

Over 130 countries are exploring or piloting CBDCs as of 2024, according to the Atlantic Council’s CBDC Tracker. The intersection of CBDCs with sovereign savings is profound:

- CBDCs could serve as the infrastructure for next-generation retail savings programs — government-backed, digital, instantly accessible

- Programmable money could allow governments to issue time-limited savings instruments or conditional savings incentives directly to citizens

- The Bank for International Settlements (BIS) Innovation Hub is actively researching cross-border CBDC architectures that could reshape how sovereign securities are settled internationally

2. Artificial Intelligence in Sovereign Asset Management

AI and machine learning are transforming sovereign asset management at multiple levels:

- Portfolio optimization: AI-driven factor models are augmenting traditional mean-variance optimization at major SWFs including GIC and ADIA

- Risk surveillance: Natural language processing (NLP) tools monitor geopolitical news flows and ESG event signals in real time, feeding risk dashboards for sovereign debt managers

- Liquidity management: Predictive analytics improve cash flow forecasting for sovereign debt offices, reducing borrowing costs

- Firms like BlackRock (whose Aladdin platform manages risk analytics for sovereign and institutional investors globally) are at the forefront of AI-augmented asset management infrastructure

🔗 BlackRock Aladdin — BlackRock.com ; BIS Innovation Hub CBDC research — BIS.org

3. Climate-Aligned Sovereign Finance

The Task Force on Climate-related Financial Disclosures (TCFD) framework is increasingly being applied to sovereign balance sheets. The IMF’s 2021 paper, “A Strategy to Scale Up Climate Finance”, sets out a roadmap for integrating climate risk into sovereign debt sustainability assessments.

Key developments:

- Nature-linked bonds (biodiversity/ocean conservation): Belize’s Blue Bond debt-for-nature swap (facilitated by The Nature Conservancy) is a landmark model

- Debt-for-climate swaps: Enabling heavily indebted developing nations to reduce sovereign debt obligations in exchange for binding climate investment commitments

- NGFS (Network for Greening the Financial System): A coalition of 130+ central banks and supervisors integrating climate scenarios into sovereign reserve management

4. Geopolitical Fragmentation and Reserve Diversification

The freezing of Russian central bank reserves (approximately $300 billion) following the 2022 Ukraine invasion fundamentally challenged the assumption of sovereign asset safety in major reserve currencies. Consequences include:

- Accelerated reserve diversification away from USD and EUR by non-Western central banks

- Growing interest in gold reserves (central bank gold purchases reached record levels in 2023, per World Gold Council data)

- Debate within the IMF about reform of the Special Drawing Rights (SDR) basket and the future of the international monetary system

- Emerging markets exploring bilateral currency swap arrangements as alternatives to reserve accumulation

Conclusion: Sovereign Finance as the Foundation of Global Stability

Sovereign wealth management and national savings programs are far more than technical fiscal instruments. They represent a society’s commitment to intergenerational equity, financial resilience, and responsible stewardship of public assets.

Key Takeaways for Financial Professionals

- Government securities — from US Treasuries to UK Gilts to sovereign Sukuk — remain the foundational layer of global financial markets, but their risk profiles are more nuanced than traditional “risk-free” classifications suggest.

- Sovereign Wealth Funds, when governed according to international best practices (Santiago Principles, ESG frameworks, transparent reporting), can be transformative engines of long-term national prosperity.

- National savings programs, increasingly powered by digital and FinTech innovation, are becoming critical tools for financial inclusion and domestic savings mobilization — particularly in emerging markets.

- ESG integration is no longer optional for sovereign finance actors: it is a risk management imperative with direct implications for long-term fund sustainability and sovereign creditworthiness.

- Geopolitical risk has re-entered the sovereign asset equation with force, requiring sovereign wealth managers to revisit assumptions about asset safety, diversification, and reserve architecture.

Actionable Insights

- Sovereign debt managers should benchmark their governance frameworks against the IMF’s Revised Guidelines for Public Debt Management and align reporting with IPSAS standards.

- SWF investment teams should formally integrate climate scenario analysis (NGFS scenarios) and TCFD-aligned disclosures into their SAA and risk management processes.

- Retail savings program administrators should explore digital distribution channels — including mobile money platforms and CBDC-adjacent technologies — to expand reach and improve financial inclusion outcomes.

- Institutional investors engaging with sovereign securities should assess not just credit ratings but governance quality, ESG trajectory, and debt sustainability metrics as part of their fiduciary responsibility.

The Road Ahead

The next decade of sovereign finance will be defined by the intersection of digital transformation, climate transition, and geopolitical realignment. Sovereign wealth funds and national savings programs that adapt — embracing AI-driven analytics, green finance innovation, and international governance standards — will not only protect their nations’ wealth but actively shape the contours of the emerging global financial order.

The question is not whether sovereign finance will transform. It is whether institutions will lead that transformation — or be led by it.

Frequently Asked Questions (FAQ)

Q1: What is the difference between a sovereign wealth fund and a central bank’s foreign exchange reserves?

Foreign exchange reserves are assets held by a central bank primarily for monetary policy objectives — managing exchange rate stability, servicing short-term external debt, and providing a buffer against balance-of-payments shocks. They are typically held in highly liquid, low-risk instruments (government bonds, gold, SDRs).

Sovereign wealth funds, by contrast, are established for longer-term objectives — intergenerational savings, economic stabilization, or strategic investment. They invest across a broader asset class spectrum (equities, infrastructure, private equity) and accept higher risk in exchange for higher long-term returns. The IMF’s 2008 Santiago Principles explicitly distinguish SWFs from reserve assets, pension funds, and state-owned enterprises.

Q2: Are government securities truly “risk-free”?

Government securities are conventionally treated as risk-free in the sense that a sovereign government borrowing in its own currency can, in theory, always repay by printing money. However, this masks several real risks:

- Inflation risk: “Printing” to repay erodes purchasing power — bondholders may receive full nominal repayment but a fraction of real value

- Currency risk: For foreign investors, exchange rate movements can dramatically alter returns

- Sovereign default risk: Countries borrowing in foreign currencies (or subject to external debt traps) can and do default — as seen in Argentina, Sri Lanka, and Zambia in recent years

- Market/liquidity risk: Even the deepest sovereign markets (US Treasuries) experienced significant liquidity stress in March 2020

The Basel Committee and IMF have both published research questioning whether preferential “zero risk weight” treatment for all sovereign debt remains appropriate in the post-2010 environment.

Q3: How do ESG considerations affect sovereign debt ratings and investment decisions?

ESG is becoming an increasingly material factor in sovereign credit analysis, although the integration is still evolving. Key developments:

- Rating agencies (Moody’s, S&P, Fitch) have introduced ESG scores for sovereigns, assessing factors like governance quality, environmental vulnerability (climate change exposure), and social stability indicators

- Institutional investors applying ESG screening may exclude sovereigns with poor governance records or high carbon exposure from their investment universe — influencing sovereign borrowing costs

- Green and sustainability-linked sovereign bonds explicitly tie sovereign financing to ESG performance, creating market incentives for governments to deliver on environmental and social commitments

- The Principles for Responsible Investment (PRI) and IFSWF’s One Planet framework provide structured guidance for integrating ESG into sovereign and SWF investment mandates

The empirical evidence linking strong ESG governance to lower sovereign borrowing costs is growing — aligning the business case for responsible investment with the imperatives of financial governance excellence.

Suggested Further Reading & External Resources

- 🔗 IMF Sovereign Debt Management Guidelines

- 🔗 Santiago Principles — IFSWF

- 🔗 Basel Committee Publications — BIS

- 🔗 World Bank Sovereign Debt Management

- 🔗 NGFS Climate Scenarios for Central Banks

- 🔗 Norges Bank Investment Management Annual Report

- 🔗 UK Debt Management Office — Gilt Market

- 🔗 US Treasury — TreasuryDirect

- 🔗 BlackRock Investment Institute — Sovereign Research

This article reflects global financial governance standards and publicly available institutional data as of 2024. It is intended for informational and professional development purposes and does not constitute investment advice. For jurisdiction-specific guidance, consult qualified financial and legal advisors.