Table of Contents

- Introduction: The $310 Billion Tipping Point

- Key Definitions: The Language of Financial Inclusion

- The Global Landscape: Who Remains Excluded — and Why

- Microcredit: From Grameen to the Digital Frontier

- Mobile Money Revolution: The M-Pesa Blueprint

- Digital Financial Services: FinTech as the Great Equalizer

- Regulatory Frameworks and Global Governance Standards

- ESG Integration in Inclusive Finance

- Case Studies in Financial Inclusion Excellence

- Best Practices: Operational Excellence & Risk Management

- Emerging Trends: AI, CBDCs, and the Future of Inclusion

- Expert Perspectives

- Conclusion: The Road Ahead

- FAQ

Introduction: The $310 Billion Tipping Point {#introduction}

In 2026, the global microfinance market is valued at approximately $310 billion — a figure that would have seemed implausible to Muhammad Yunus when he lent the equivalent of $27 to 42 basket weavers in rural Bangladesh in 1974. That single act of radical financial inclusion sparked a worldwide movement that today reaches nearly 200 million borrowers across six continents.

Yet a profound paradox persists. Despite a historic milestone confirmed by the World Bank’s Global Findex 2025 — that 79% of adults globally now hold a financial account, up from just 62% a decade ago — an estimated 1.4 billion adults remain entirely unbanked, locked out of savings, credit, insurance, and the very tools of economic mobility. For these individuals, financial exclusion is not merely an inconvenience; it is a structural barrier that perpetuates intergenerational poverty.

The stakes could not be higher. Access to financial services is increasingly recognized by multilateral institutions — including the International Monetary Fund (IMF), the World Bank, and the G20’s Global Partnership for Financial Inclusion (GPFI) — as a foundational prerequisite for achieving the UN Sustainable Development Goals (SDGs), particularly SDG 1 (No Poverty), SDG 8 (Decent Work and Economic Growth), and SDG 10 (Reduced Inequalities).

This article offers an analytically rigorous, globally oriented examination of the microfinance revolution in 2026: the mechanisms powering it, the institutions leading it, the regulatory frameworks governing it, and the emerging technologies redefining what “financial access” means for the world’s most vulnerable populations.

Data Reference: World Bank Global Findex Database 2025 | IMF Financial Access Survey (FAS) 2025 Annual Report | Global Microfinance Market Report 2025–2030

Key Definitions: The Language of Financial Inclusion {#definitions}

To engage rigorously with financial inclusion, professionals must command its foundational vocabulary. Below are the essential terms that structure the global discourse.

Financial Inclusion

The condition in which individuals and businesses have access to useful and affordable financial products and services — including transactions, payments, savings, credit, and insurance — that meet their needs and are delivered responsibly and sustainably.

Microfinance

A category of financial services targeting individuals, microenterprises, and small businesses that lack access to conventional banking. Microfinance encompasses microcredit (small loans, typically under $1,000 in developing economies), microsavings, microinsurance, and payment services.

Microcredit

The extension of small loans, typically without traditional collateral, to low-income borrowers. Microcredit programs often use group-lending models (solidarity groups), in which borrowers mutually guarantee each other’s loans — a mechanism pioneered by Grameen Bank and now replicated by thousands of Microfinance Institutions (MFIs) globally.

Financial Intermediation

The process by which financial institutions — banks, MFIs, cooperatives, and increasingly digital platforms — channel funds from surplus units (savers/investors) to deficit units (borrowers/entrepreneurs). Effective financial intermediation reduces information asymmetry and lowers transaction costs.

Maturity Transformation

A fundamental function of financial intermediation in which institutions borrow short-term (accepting deposits) and lend long-term (issuing loans). This creates liquidity risk that MFIs and digital lenders must actively manage through robust asset-liability management (ALM) frameworks aligned with Basel Committee on Banking Supervision (BCBS) principles.

Fiduciary Responsibility

The legal and ethical obligation of financial institutions to act in the best interests of their clients. In microfinance, fiduciary responsibility encompasses responsible lending practices, transparent pricing, client protection, and data privacy — all enshrined in frameworks such as the Client Protection Pathways (formerly the Smart Campaign) and the SPTF Universal Standards for Social and Environmental Performance Management.

Financial Deepening

The process by which a broader proportion of the population actively uses a wider range of financial services, increasing the overall depth and efficiency of the financial system. Financial deepening is measurable through indicators such as private credit-to-GDP ratio, account ownership rates, and transaction volumes — all tracked in the IMF’s Financial Access Survey.

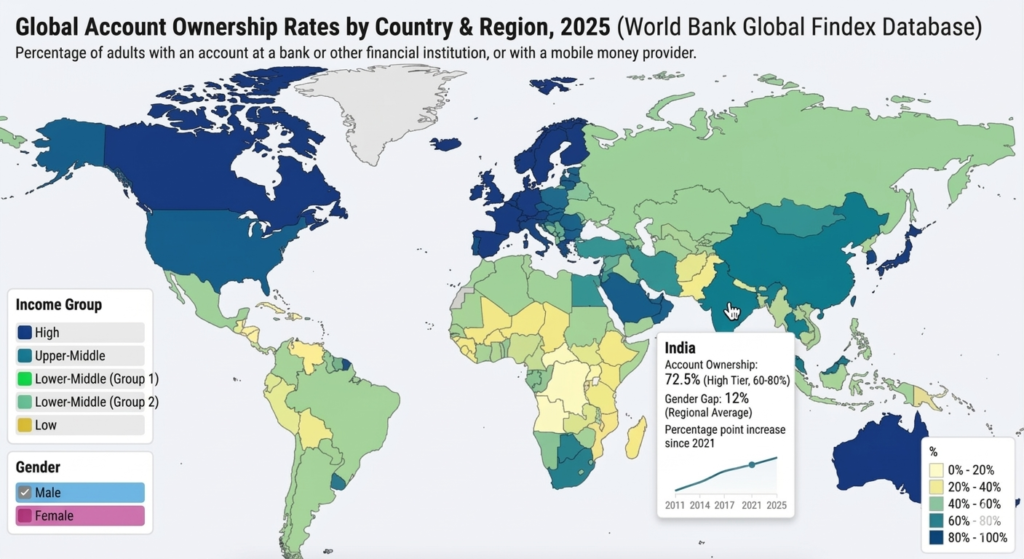

The Global Landscape: Who Remains Excluded — and Why {#global-landscape}

Understanding financial exclusion requires a regional lens. The World Bank Global Findex 2025 reveals striking divergences:

| Region | Account Ownership (Adults) | Mobile Money Penetration | Key Barrier |

| East Asia & Pacific | 83% | Moderate | Rural-urban digital divide |

| Europe & Central Asia | 78% | Low-moderate | Stagnant growth post-2021 |

| South Asia | 78% | Growing | Gender gap; informal economy |

| Latin America & Caribbean | 70% | 37% & rising | Informality; infrastructure gaps |

| Middle East & North Africa | 53% | Low | Regulatory fragmentation; conflict |

| Sub-Saharan Africa | ~55% | 40% (mobile money leader) | Infrastructure; last-mile access |

📊An interactive choropleth map displaying global account ownership rates by region, sourced from World Bank Findex 2025 data.

Why Exclusion Persists

Financial exclusion is rarely a singular problem. It is the product of overlapping structural barriers:

- Infrastructure deficits: Only one bank branch per 100,000 adults exists in the lowest-income nations, according to the International Finance Corporation (IFC).

- Documentation barriers: KYC (Know Your Customer) requirements lock out individuals without national IDs, birth certificates, or proof of address.

- Affordability: Minimum balance requirements, account maintenance fees, and high transaction costs render formal banking economically irrational for low-income users.

- Gender discrimination: Globally, women are 6 percentage points less likely than men to hold a formal account, according to Findex 2025 — a gap rooted in legal restrictions, mobility constraints, and cultural norms.

- Geographic remoteness: Rural populations face prohibitive distances to the nearest financial service point.

- Low financial literacy: Even where access exists, capability gaps prevent meaningful participation.

The convergence of mobile technology, regulatory innovation, and impact investment is dismantling these barriers with remarkable speed. But the work is far from complete.

Microcredit: From Grameen to the Digital Frontier {#microcredit}

The Grameen Model and Its Global Legacy

The modern microfinance movement traces its intellectual and operational origins to Grameen Bank, founded in Bangladesh by Nobel Peace Prize laureate Muhammad Yunus. The Grameen model established principles that remain foundational:

- Group lending: Borrowers form solidarity circles, with peer pressure and social capital replacing collateral.

- Progressive lending: Loan sizes increase as borrowers demonstrate repayment reliability.

- Women-centered design: Over 97% of Grameen borrowers are women, reflecting evidence that women reinvest earnings into family welfare at higher rates than men.

- Weekly repayments: Frequent, small installments reduce default risk and build financial discipline.

Grameen Bank today serves approximately 9 million clients and holds a 4% global market share among MFIs — remarkable for an institution that began with a handful of village women and a $27 personal loan.

The Scale of Modern Microcredit

The microcredit landscape has evolved dramatically:

- 139.9 million borrowers benefit from MFI services globally, with 80% being women.

- South Asia dominates by borrower count, with India alone accounting for nearly 35% of global microfinance clients.

- Latin America and the Caribbean leads by portfolio size, holding 44% of total sector assets — approximately $48.3 billion in outstanding loans.

- The sector maintains an average annual growth rate of 11.5% over the past five years, driven by digital transformation.

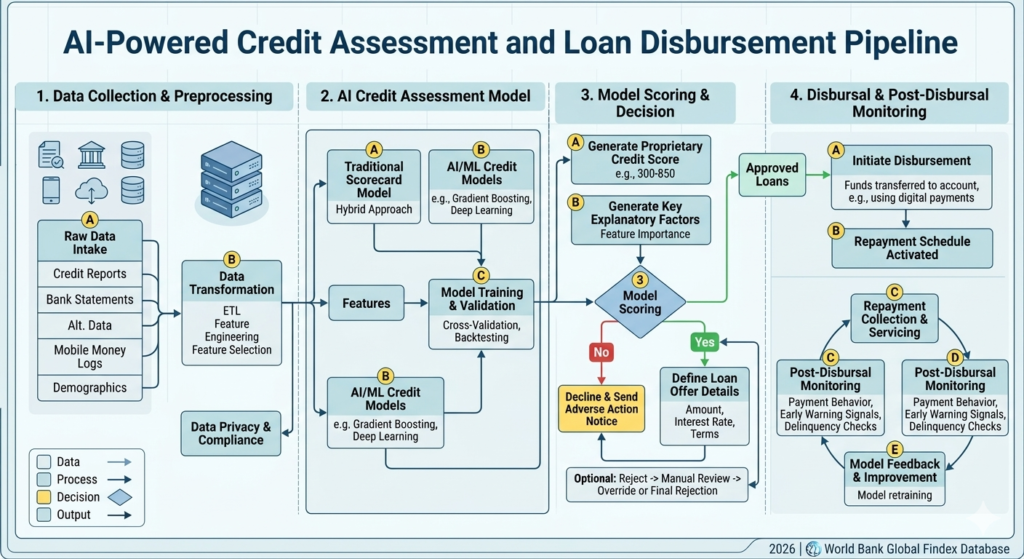

AI-Powered Credit Scoring: The New Frontier of Microlending

Perhaps the most transformative development in microcredit is the displacement of traditional underwriting by AI-driven alternative credit scoring. Leading MFIs and FinTech lenders now assess creditworthiness through:

- Mobile data analytics: Call frequency, app usage, utility payment history, and airtime top-up patterns serve as proxies for financial behavior.

- Satellite imagery: For agricultural lending, satellite data assesses crop health, farm size, and yield potential — enabling rational pricing of agricultural microloans.

- Psychometric assessments: Behavioral tests measure character traits (honesty, risk tolerance, resilience) correlated with loan repayment.

- Blockchain-based credit histories: Immutable ledgers build portable credit identities for individuals without formal banking records.

📊 A step-by-step flowchart illustrating the AI credit assessment pipeline — from data collection through model scoring to loan disbursement

Mobile Money Revolution: The M-Pesa Blueprint {#mobile-money}

The Origin Story

Launched in 2007 by Safaricom — a Kenyan telecom operator with backing from Vodafone — M-Pesa (M for mobile; Pesa meaning money in Swahili) was conceived as a mechanism for microfinance clients to repay loans via mobile phone. It rapidly evolved into something far more consequential: the world’s first large-scale mobile money ecosystem.

The innovation was elegantly simple: any mobile phone, even a basic feature phone without internet access, could send, receive, and store value. Transactions required only a PIN and a network of local agents — shopkeepers, petrol station attendants, small traders — who converted cash into digital e-money and vice versa.

By the Numbers: M-Pesa in 2025–2026

The platform’s growth has been extraordinary by any metric:

- 60+ million active users in Kenya alone by 2025, covering a substantial share of the adult population.

- $450 billion+ in annual transaction volume across East Africa in 2025, a figure that exceeds Kenya’s GDP multiple times over.

- 91% mobile money market penetration in Kenya by June 2025, according to the Communications Authority of Kenya — among the highest rates in the world.

- 83%+ of Kenyan adults now have formal access to financial services, compared to just 26% before M-Pesa’s launch in 2007.

- M-Pesa’s transaction processing capacity is being expanded to 8,000 transactions per second under its Fintech 2.0 platform upgrade.

Economic and Social Impact

The macroeconomic evidence for M-Pesa’s impact is compelling:

- Mobile money adoption has been linked to a 2.6% reduction in poverty levels in participating communities.

- Over a decade, mobile money contributed an estimated $600 billion to sub-Saharan Africa’s GDP.

- M-Pesa helped lift approximately 194,000 Kenyan households (roughly 2% of the population) out of poverty by boosting per capita consumption.

- In female-headed households, M-Pesa enabled a shift from subsistence farming to microenterprise operation, with measurable increases in household income and educational attainment for children.

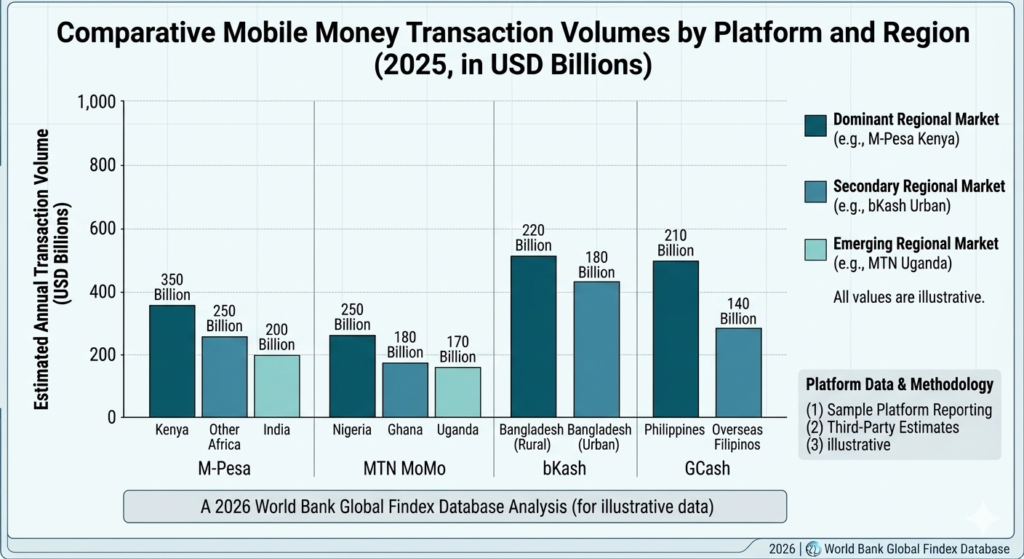

Replication Across the Globe

M-Pesa’s blueprint has catalyzed mobile money ecosystems across multiple regions:

- MTN Mobile Money (MoMo): Operates across 17 African markets; in Ghana, mobile money transaction values reached GH¢1.912 trillion in 2023 — a 78.7% annual increase.

- bKash (Bangladesh): One of the world’s largest mobile financial services platforms by subscriber count, serving tens of millions of low-income Bangladeshis.

- GCash and Maya (Philippines/Southeast Asia): Southeast Asia saw a 20% increase in microfinance digital adoption in 2023, with digital wallets becoming primary financial accounts for millions.

- JazzCash and Easypaisa (Pakistan): Serving millions in one of the world’s largest unbanked markets.

📊 A comparative bar chart showing mobile money transaction volumes by platform and region (M-Pesa, MTN MoMo, bKash, GCash)

Digital Financial Services: FinTech as the Great Equalizer {#digital-fintech}

The Embedded Finance Revolution

Digital Financial Services (DFS) represent a broader ecosystem than mobile money alone. They encompass digital payments, digital lending, digital savings, microinsurance, and — increasingly — embedded finance: the integration of financial services into non-financial digital platforms (e-commerce, health apps, agricultural platforms, ride-hailing services).

This embedded finance model is profoundly important for financial inclusion because it reaches users within digital contexts they already inhabit, removing the friction of seeking out separate financial services.

Key DFS trends reshaping global banking in 2026:

- Super apps: Platforms like M-Pesa’s expanding ecosystem, integrating insurance, lending, healthcare payments, entertainment, and government services into a single interface.

- Agent banking networks: Physical human agents who extend the digital banking frontier into remote areas without internet infrastructure.

- USSD-based services: Unstructured Supplementary Service Data enables financial transactions on the most basic mobile phones — no smartphone or internet required — dramatically extending last-mile reach.

- Open banking APIs: Interoperability mandates are enabling data portability across financial providers, reducing switching costs and stimulating competition.

FinTech Partnerships with Traditional MFIs

A structural shift is reshaping the microfinance institutional landscape: the rise of MFI-FinTech partnerships. Traditional microfinance institutions bring:

- Established client relationships and trust

- Regulatory licenses and compliance infrastructure

- Deep understanding of local credit culture

FinTech firms contribute:

- Digital origination and onboarding technology

- AI-powered credit scoring

- Mobile disbursement and collections infrastructure

- Data analytics capabilities

The combination is proving formidable. Institutions blending traditional relationship lending with digital technology are demonstrating superior outreach and credit performance, according to the 2024 MFI Index (60 Decibels), which surveyed 36,000+ clients across 45 countries.

Blockchain and Distributed Ledger Technology

Blockchain-based microloan tracking is gaining traction for its ability to deliver transparent, tamper-proof transaction records — a critical feature for building trust among both borrowers (who may distrust opaque institutions) and impact investors (who require verifiable social outcome data).

Applications include:

- Portable credit histories for mobile populations

- Cross-border remittances at dramatically reduced cost (relevant to the $650B+ global remittance market)

- Smart contract-based lending with automatic disbursement and collection

- Impact measurement on blockchain for ESG reporting

Regulatory Frameworks and Global Governance Standards {#regulatory}

Financial inclusion cannot flourish without proportionate, enabling regulatory frameworks. The global regulatory landscape is being shaped by several key bodies and frameworks.

The Basel Committee on Banking Supervision (BCBS)

The Basel III/IV framework — the international regulatory standard for bank capital adequacy, stress testing, and liquidity risk — primarily targets systemically important financial institutions. However, the Basel Committee has increasingly engaged with microfinance risk, recognizing that MFI growth at scale introduces systemic considerations.

Key Basel principles applicable to inclusive finance:

- Pillar 1 (Minimum Capital Requirements): MFIs must maintain adequate capital buffers relative to credit, market, and operational risk.

- Pillar 2 (Supervisory Review): National regulators are expected to assess the adequacy of internal risk management frameworks within MFIs.

- Pillar 3 (Market Discipline): Transparency and disclosure requirements ensure stakeholders can assess MFI financial health.

🔗 External Link Suggestion: Basel Committee on Banking Supervision Publications — the definitive resource for regulatory capital standards.

The IMF’s Financial Access Survey Framework

The IMF’s FAS (Financial Access Survey), published annually, provides the world’s most comprehensive dataset on financial services access. The FAS 2025 Annual Report, subtitled “Fintech, a Catalyst for Financial Services Access, Innovation, and Growth,” documents how FinTech innovation is reshaping the global financial access landscape.

Key IMF policy recommendations for inclusive finance:

- Tiered KYC frameworks: Simplified identity verification for low-value accounts reduces barriers to entry without compromising AML/CFT compliance.

- Regulatory sandboxes: Controlled innovation environments allow FinTechs to test novel products under regulatory supervision before full licensing.

- Proportionate regulation: Regulatory requirements calibrated to the risk profile of activities, not institutional form.

The G20 Financial Inclusion Action Plan

The G20 Global Partnership for Financial Inclusion (GPFI) coordinates international commitments to financial inclusion among the world’s largest economies. The current action plan emphasizes:

- Digital financial literacy

- Consumer protection in digital finance

- Women’s economic empowerment

- Financial resilience for vulnerable populations

Consumer Protection Frameworks

As financial inclusion scales globally, client protection has emerged as a critical governance priority. The Client Protection Pathways (CPP) framework, endorsed by a coalition of international investors and MFIs, establishes minimum standards including:

- Appropriate loan product design

- Prevention of over-indebtedness

- Transparent pricing and terms

- Fair treatment and non-discrimination

- Privacy of client data

- Mechanisms for complaint resolution

🔗 External Link Suggestion: CGAP (Consultative Group to Assist the Poor) — the World Bank Group’s policy and research center for financial inclusion governance.

ESG Integration in Inclusive Finance {#esg}

The Convergence of Impact and Returns

Environmental, Social, and Governance (ESG) principles have moved from the periphery to the mainstream of global financial governance. For the microfinance sector, ESG integration is not merely a compliance exercise — it is fundamental to mission.

Social performance management (SPM) has long been central to MFI operations. What is new in 2026 is the sophistication with which social outcomes are measured, standardized, and reported — enabling comparability across institutions and geographies.

Key ESG Dimensions in Inclusive Finance

Environmental (E):

- Green microfinance: Loans for solar energy systems, efficient cookstoves, water purification, and climate-resilient agriculture.

- Climate risk integration: IoT-enabled monitoring of agricultural borrowers’ climate exposure, informing adaptive loan structuring.

- Pay-as-you-go (PAYG) energy financing: Embedded microfinance for off-grid energy access, reaching communities without electricity grid infrastructure.

Social (S):

- Women’s financial inclusion: Female-centric financial service providers (FSPs) demonstrably outperform peers in improving clients’ financial resilience and household influence, according to the 2024 MFI Index.

- Rural inclusion: Measuring and maximizing reach to rural and remote populations who lack geographic proximity to formal financial infrastructure.

- Financial health outcomes: Beyond access metrics, measuring whether financial services actually improve clients’ economic wellbeing, resilience, and agency.

Governance (G):

- MFI Board composition and independence: Strong governance standards aligned with IFC Performance Standards.

- Transparent pricing: Commitment to publishing Effective Annual Rates (EAR) and interest rate transparency.

- Anti-corruption and AML/CFT compliance: Alignment with FATF (Financial Action Task Force) recommendations.

Impact Investing and the Funding Landscape

The microfinance sector is entering a period of significant funding reconfiguration. As noted by the Center for Financial Inclusion (CFI) in its landmark December 2025 analysis, bilateral donor support has contracted significantly — USAID effectively ended, while Germany, France, the Netherlands, and others sharply reduced commitments.

In response, the sector is pivoting toward:

- Impact investing funds providing blended finance

- Development Finance Institutions (DFIs) such as IFC, DEG, and FMO

- Green bonds and sustainability-linked debt instruments

- FinTech-enabled retail investment platforms connecting small investors to microfinance portfolios

Case Studies in Financial Inclusion Excellence {#case-studies}

Case Study 1: M-Pesa’s Fintech 2.0 Evolution (East Africa)

Challenge: Sustaining financial inclusion momentum as the market approaches saturation in core markets.

Innovation: M-Pesa’s Fintech 2.0 platform represents a fundamental architectural overhaul, introducing:

- NFC-enabled “Tap to Pay” contactless payments

- AI-driven fraud detection and personalization

- “Wallet Sharing” features for household financial management

- Full integration with government services (health insurance, taxation)

- Cross-border payment interoperability across East Africa

Outcome: Transaction capacity scaling to 8,000 transactions per second; positioning M-Pesa as a comprehensive digital life platform rather than a payments tool. This evolution mirrors the “super app” trajectory of platforms like China’s WeChat Pay, but adapted to African mobile-first users.

Global Relevance: M-Pesa demonstrates that financial inclusion infrastructure, once established, can continuously deepen its value proposition — moving from access to usage to financial health improvement.

Case Study 2: AI-Powered Agricultural Microfinance (South/Southeast Asia)

Challenge: Agricultural smallholders — representing the majority of the world’s poorest — face acute barriers to credit: lack of collateral, seasonal income variability, and remoteness from financial institutions.

Innovation: Leading MFIs and AgriTech-FinTech partnerships are deploying:

- Satellite imagery analysis assessing crop health, irrigated area, and historical yield

- IoT soil sensors providing real-time data on growing conditions

- Weather derivatives embedded in loan structures, automatically adjusting repayment schedules during drought or flood events

- Smartphone-based farm mapping enabling remote appraisals at negligible cost

Outcome: Significant improvement in agricultural loan portfolio quality; reduction in loan officer visit costs; expansion of credit access to smallholders previously deemed “unbankable.”

Regulatory Context: This innovation operates within frameworks shaped by the Alliance for Financial Inclusion (AFI) and national agricultural development banks aligned with World Bank FinSAP (Financial Sector Assessment Program) recommendations.

Case Study 3: Digital MFI Partnerships in Latin America

Challenge: Latin America leads in microfinance portfolio size ($48B+) but trails in digital adoption, with informality and fragmented regulation constraining growth.

Innovation: A new generation of digital-first MFIs — operating via mobile apps with fully digital onboarding, e-signature loan documentation, and WhatsApp-based customer service — is reaching urban and peri-urban informal workers previously excluded from traditional MFI programs.

Notable Feature: Women-led microentrepreneurs, who constitute the majority of borrowers, receive tailored financial education content embedded in the digital loan journey — addressing financial literacy gaps without requiring in-person training.

Regulatory Environment: The Inter-American Development Bank (IDB) and CAF – Development Bank of Latin America provide technical assistance and blended finance to support sustainable scaling.

Case Study 4: Green Inclusive Finance in South Asia

Challenge: Climate change disproportionately impacts low-income communities in South Asia — the region’s 85+ million microfinance borrowers face escalating exposure to flood, drought, and heat stress.

Innovation: Leading MFIs in the region are piloting climate-adaptive microfinance products including:

- Solar home system loans financed through PAYG models

- Index-based crop insurance bundled with agricultural microloans

- Climate-resilient livelihood loans supporting transition from vulnerable activities (e.g., coastal fishing) to more resilient alternatives

ESG Alignment: These products align with the Paris Agreement’s adaptation finance goals and the Sustainable Development Goals (SDGs), making them attractive to ESG-mandated institutional investors seeking verified green/social impact.

Best Practices: Operational Excellence & Risk Management {#best-practices}

Responsible Lending: The Foundation of Sustainable Inclusion

Irresponsible microfinance — characterized by aggressive sales, inadequate client assessment, and punitive interest rates — has caused documented crises in multiple markets (including India’s Andhra Pradesh crisis of 2010 and recent NPA spikes in the MFI sector). The industry’s hard-learned lesson: sustainability requires client welfare.

Best-practice responsible lending in 2026 includes:

1. Client-Centered Product Design

- Loan products structured around borrower cash flow, not institutional calendar convenience

- Flexible repayment schedules for seasonal or irregular income earners

- Grace periods for genuine emergencies, embedded as standard product features

2. Over-indebtedness Prevention

- Integration with credit bureau data to assess existing debt obligations

- Implementation of debt-to-income ratio caps

- Mandatory cooling-off periods between successive loans

- Staff incentives tied to portfolio quality, not loan volume

3. Transparent Pricing

- Mandatory disclosure of Effective Annual Rates (EAR) using standardized CGAP/MIX Market methodology

- Prohibition of hidden fees (processing fees, insurance premiums embedded without disclosure)

- Digital loan contracts with clear, plain-language terms in local languages

Credit Risk Management

MFIs face a distinctive risk profile that demands specialized management:

- Portfolio at Risk (PAR>30) — the proportion of the portfolio where payments are more than 30 days overdue — is the sector’s primary credit quality metric. Best-practice MFIs maintain PAR>30 below 5%.

- Loan Loss Provisioning: Adequate provisioning aligned with expected credit loss (ECL) accounting principles under IFRS 9 and equivalent standards.

- Concentration Risk: Monitoring geographic, sectoral, and demographic concentration to avoid correlated defaults during localized shocks.

- Climate Risk Stress Testing: Emerging best practice requires modeling portfolio performance under climate scenarios (floods, droughts, heat events) — aligned with the Task Force on Climate-related Financial Disclosures (TCFD) framework.

Digital Security and Data Privacy

As financial services migrate to digital channels, cybersecurity and data governance become critical institutional responsibilities:

- End-to-end encryption of all financial transaction data

- Biometric authentication reducing fraud risk in mobile money

- Data minimization principles — collecting only data necessary for service delivery

- Compliance with GDPR (for European operations) and emerging data protection legislation in developing markets

- AI fairness audits ensuring algorithmic credit scoring does not perpetuate discriminatory patterns

Institutional Governance

Strong governance is the backbone of sustainable microfinance institutions:

- Independent board members with relevant financial expertise

- Separation of ownership and management

- Robust internal audit and external audit functions

- Social performance management (SPM) embedded in board-level reporting

- Anti-fraud and whistleblower mechanisms

- Regular third-party social ratings (e.g., MicroRate, Planet Rating)

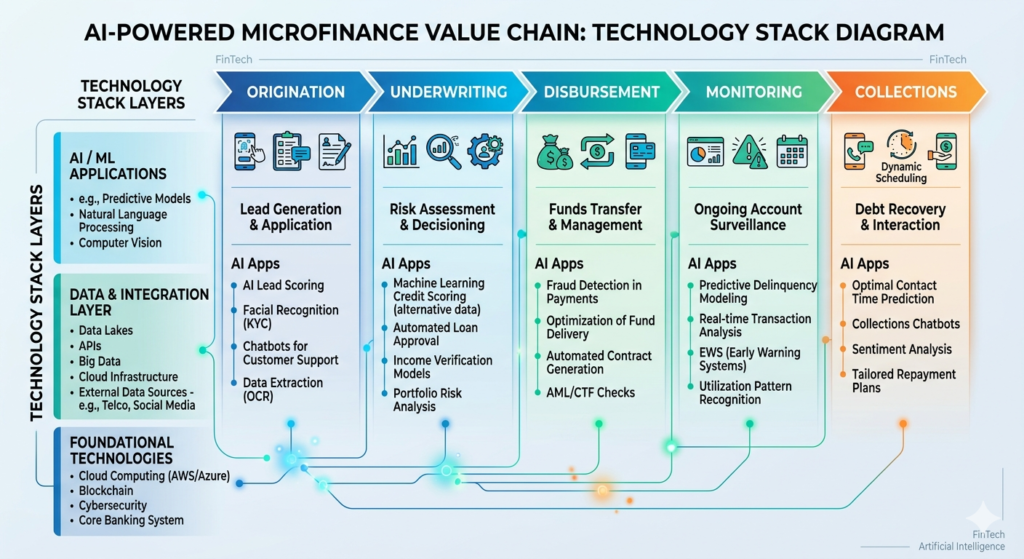

Emerging Trends: AI, CBDCs, and the Future of Inclusion {#emerging-trends}

1. Artificial Intelligence and Machine Learning

AI is reshaping every dimension of inclusive finance:

- AI credit scoring: Processing thousands of data points in real time to assess creditworthiness without traditional collateral or documentation requirements.

- Conversational AI: Chatbots and voice assistants in local languages are extending financial literacy and customer service to low-literacy populations.

- Fraud detection: Real-time anomaly detection systems reducing losses from mobile money fraud.

- Portfolio management: Predictive analytics identifying early warning signs of client stress, enabling proactive intervention.

- Personalization: Tailored financial product recommendations based on individual behavior patterns.

📊 A technology stack diagram showing AI applications across the microfinance value chain (origination → underwriting → disbursement → monitoring → collections)

2. Central Bank Digital Currencies (CBDCs)

More than 130 countries are actively exploring or piloting Central Bank Digital Currencies (CBDCs). For financial inclusion, CBDCs hold transformative potential:

- Universal access: A CBDC wallet, issued by the central bank, could provide every citizen with a foundational digital financial identity.

- Programmable money: Smart contract-enabled CBDCs could automate government benefit transfers, agricultural subsidy disbursements, and conditional cash transfers with precision and efficiency.

- Reduced transaction costs: CBDC infrastructure could dramatically reduce the cost of financial transactions, making micropayments economically viable.

- Interoperability: CBDCs could bridge between mobile money ecosystems, bank accounts, and international payment rails.

The Bank for International Settlements (BIS) and IMF are actively developing cross-border CBDC frameworks (mBridge, Project Nexus) that could fundamentally reshape international remittance flows critical to low-income households in developing economies.

3. Embedded Finance and the Platform Economy

The integration of financial services into non-financial platforms — agriculture apps, health platforms, e-commerce marketplaces — is enabling contextual financial inclusion: reaching users at the exact moment of financial need, within platforms they already trust.

4. Climate Finance Integration

Green and climate-adaptive microfinance products are projected to be among the sector’s fastest-growing segments through 2030. Blended finance mechanisms — combining public development finance with private impact investment — are scaling green microfinance in alignment with COP climate commitments and the Sharm el-Sheikh Adaptation Agenda.

5. Interoperability Mandates

Regulators across Africa, South Asia, and Southeast Asia are mandating interoperability between mobile money platforms and banking systems — allowing users to transfer value seamlessly regardless of provider. This competition-enhancing reform reduces market concentration risk while expanding consumer choice.

Expert Perspectives {#expert-quotes}

“Mobile financial services platforms like M-Pesa are vital drivers of financial inclusion in society, which can improve individual life chances and enable enterprises to launch and expand, bringing wealth and jobs into developing economies.” — Safaricom Leadership, commenting on M-Pesa’s broader economic impact (Safaricom FY24 Results Booklet)

“The sector enters 2026 shaped by the tension between rising inclusion and shrinking resources. This tension is setting in motion a reconfiguration that will influence the decade ahead.” — Center for Financial Inclusion (CFI), Financial Inclusion in 2026: Progress, Funding Shifts, and the Next Phase of the Sector (December 2025)

“What began as a microcredit movement driven by community-based organizations has grown into a vibrant ecosystem that includes development and financial sector organizations; fintech and technology firms; impact investors; and a growing cadre of mission-driven entrepreneurs.” — Center for Financial Inclusion (CFI), December 2025 Sector Analysis

Conclusion: The Road Ahead {#conclusion}

The global microfinance revolution of 2026 is a story of extraordinary progress shadowed by persistent gaps. Four in five adults worldwide now hold a financial account — a milestone that would have seemed utopian a generation ago. Mobile money platforms process hundreds of billions of dollars annually in economies where bank branches remain scarce. AI is making credit accessible to populations previously deemed too risky to serve. And ESG frameworks are aligning the mission of financial inclusion with the capital allocation priorities of global institutional investors.

Yet 1.4 billion adults remain beyond the reach of the financial system. The gender gap in financial access persists globally. Climate change is intensifying the financial vulnerability of the world’s poorest communities. And the funding landscape for inclusive finance is undergoing a structural contraction that will require the sector to accelerate its transition toward commercial sustainability without compromising its social mission.

For financial professionals and institutions, the strategic implications are clear:

- Digital transformation is no longer optional. Institutions that have not developed credible digital inclusion strategies will be outcompeted by nimbler FinTech entrants and tech-enabled MFIs.

- ESG integration is a commercial imperative. Impact investors, development finance institutions, and mainstream institutional capital increasingly require rigorous social and environmental performance measurement.

- Responsible finance protects long-term value. The crises of over-indebtedness in multiple markets have demonstrated that predatory growth destroys — rather than creates — sustainable franchise value.

- Regulatory engagement is a competitive advantage. Institutions that actively participate in shaping proportionate, enabling regulatory frameworks position themselves for sustainable market leadership.

- Partnership models unlock scale. MFI-FinTech partnerships, bank-agent network collaborations, and embedded finance integrations are delivering inclusion at costs no single institution could achieve independently.

The microfinance revolution is not merely a story of banking the unbanked. It is a story about the architecture of economic opportunity — about whether the financial system serves as a ladder of mobility or a wall of exclusion. The choices made by financial institutions, regulators, investors, and technologists in the years immediately ahead will determine which story is told at the end of this decade.

FAQ {#faq}

Q1: What is the difference between microfinance and microcredit?

Microcredit refers specifically to small loans extended to low-income borrowers who lack access to traditional bank credit. Microfinance is the broader umbrella term encompassing not just microcredit but also microsavings, microinsurance, digital payment services, and financial literacy programs. Modern microfinance institutions (MFIs) typically offer a full suite of financial services, recognizing that credit alone is insufficient to sustainably improve household financial wellbeing.

Q2: How is the risk of over-indebtedness managed in responsible microfinance?

Responsible MFIs manage over-indebtedness risk through multiple mechanisms: integration with credit bureaus to assess existing debt obligations before extending new credit; debt-to-income ratio caps aligned with clients’ verified cash flows; mandatory cooling-off periods between successive loans; client-centered product design that aligns repayment with income cycles; and staff incentive structures tied to portfolio quality rather than loan volume. Regulatory frameworks such as the CGAP Consumer Protection Standards and the Client Protection Pathways provide the normative foundation for responsible lending practice.

Q3: How can institutional investors access microfinance as an asset class?

Institutional investors access microfinance through several channels: microfinance investment vehicles (MIVs) — funds that pool capital and invest across diversified portfolios of MFIs; green/social bonds issued by development finance institutions or leading MFIs; direct equity or debt investment in mature, rated MFIs; and blended finance facilities co-structured with multilateral institutions (World Bank Group, IFC, regional development banks) that provide first-loss protection to attract private capital. Key due diligence frameworks include third-party social ratings (MicroRate, Planet Rating) and financial performance benchmarks from the MIX Market (now part of the World Bank’s Global Findex ecosystem).

References and Further Reading

- World Bank Global Findex Database 2025 — worldbank.org/globalfindex

- IMF Financial Access Survey 2025 — data.imf.org

- GSMA State of the Industry Report on Mobile Money 2025 — gsma.com/sotir

- Center for Financial Inclusion: Financial Inclusion in 2026 — centerforfinancialinclusion.org

- 60 Decibels 2024 MFI Index — 60decibels.com

- Basel Committee on Banking Supervision — bis.org/bcbs

- CGAP (Consultative Group to Assist the Poor) — cgap.org

- FinDev Gateway: Financial Inclusion Global Overview — microfinancegateway.org

- G20 Global Partnership for Financial Inclusion — gpfi.org

- Alliance for Financial Inclusion (AFI) — afi-global.org

This article is intended for professional and semi-professional audiences in banking, finance, development economics, and financial governance. All statistics are referenced from publicly available reports and market analyses current as of March 2026. Readers are encouraged to consult primary sources for investment or regulatory decisions.