Introduction: The Architecture of Global Financial Stability

| Global financial assets exceeded $450 trillion in 2024, according to the McKinsey Global Institute — more than four times global GDP. The question is not how large the system has grown, but whether its internal architecture can withstand the shocks of an increasingly multipolar, digitised world. |

Every nation’s economy rests upon an invisible circulatory system — a financial architecture that channels capital from savers to borrowers, converts short-term deposits into long-term investments, manages systemic risk, and provides the payment rails on which commerce depends. Understanding this anatomy is no longer the exclusive domain of central bankers or macroprudential supervisors. In an era defined by cross-border contagion, digital disruption, and intensifying regulatory scrutiny, finance professionals, policymakers, and business leaders across all sectors must appreciate how the system functions — and where it can fracture.

This article provides a comprehensive, globally oriented examination of the key players, structures, and regulatory frameworks that constitute a national financial system. We draw on internationally recognised standards — from the Basel Committee on Banking Supervision (BCBS) to the International Monetary Fund (IMF), the Bank for International Settlements (BIS), and the Financial Stability Board (FSB) — to anchor the analysis in established best practice. Case studies reference globally significant institutions and innovations without focusing on any single national market.

Whether you are a practitioner navigating Basel IV implementation, an investor evaluating systemic risk, or a policy analyst benchmarking regulatory frameworks, this guide delivers the structural literacy you need.

Section 1: Core Definitions — The Language of Financial Systems

Before mapping the system, we must establish a common vocabulary. Below are the foundational concepts that underpin all subsequent analysis.

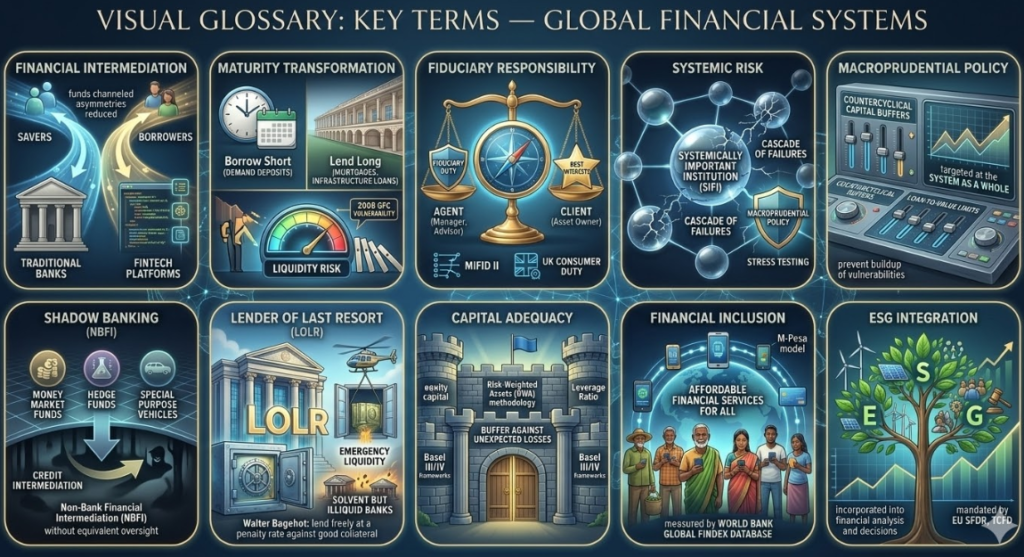

| KEY TERM GLOSSARY — GLOBAL FINANCIAL SYSTEMS |

| Financial Intermediation: The process by which financial institutions channel funds from surplus units (savers/investors) to deficit units (borrowers/issuers), reducing information asymmetries and transaction costs. Banks are the classic intermediaries; fintech platforms are redefining the model. |

| Maturity Transformation: The practice of borrowing short (demand deposits) and lending long (mortgages, infrastructure loans). This creates inherent liquidity risk — the core vulnerability exposed during the 2008 Global Financial Crisis. |

| Fiduciary Responsibility: The legal and ethical obligation of financial agents (asset managers, trustees, advisors) to act in the best interests of clients. Increasingly codified in frameworks such as the EU’s MiFID II and the UK FCA’s Consumer Duty. |

| Systemic Risk: The risk that the failure of one or more institutions triggers a cascade of failures across the financial system. Addressed through macroprudential policy, stress testing, and SIFI (Systemically Important Financial Institution) designation. |

| Macroprudential Policy: Regulatory tools targeted at the financial system as a whole — rather than individual institutions — to prevent the buildup of vulnerabilities. Examples include countercyclical capital buffers and loan-to-value limits. |

| Shadow Banking: Credit intermediation outside traditional banking regulation. The FSB prefers the term Non-Bank Financial Intermediation (NBFI) to capture entities such as money market funds, hedge funds, and special purpose vehicles that perform bank-like functions without equivalent oversight. |

| Lender of Last Resort (LOLR): The function performed by a central bank to provide emergency liquidity to solvent but illiquid institutions, preventing panic-driven runs. First articulated by Walter Bagehot: lend freely at a penalty rate against good collateral. |

| Capital Adequacy: The requirement for banks to hold minimum levels of equity capital as a buffer against unexpected losses. Governed by the Basel III/IV framework through the Risk-Weighted Assets (RWA) methodology and the leverage ratio. |

| Financial Inclusion: Ensuring access to affordable, appropriate financial services for all individuals and businesses. Measured by the World Bank’s Global Findex Database; advanced by mobile banking platforms (e.g., M-Pesa model) and digital public infrastructure. |

| ESG Integration: The systematic incorporation of Environmental, Social, and Governance factors into financial analysis and investment decisions. Increasingly mandated by regulators (EU SFDR, TCFD) and embedded in institutional investment policy. |

Section 2: The Four Pillars of a Financial System

A well-functioning financial system comprises four interdependent pillars: commercial banking, central banking and regulatory architecture, shadow banking and non-bank financial intermediation, and financial technology (fintech) innovation. Each pillar performs distinct functions; their interaction creates both resilience and vulnerability.

2.1 Commercial Banking — The Core Intermediary Layer

Commercial banks remain the bedrock of any financial system. They accept deposits, extend credit, facilitate payments, and create money through the lending process. According to the BIS, global bank assets exceeded $180 trillion by 2024, representing the largest single segment of the financial system.

Commercial banks perform three irreplaceable macroeconomic functions:

1. Credit creation: Banks do not merely intermediate pre-existing savings — they create new money when they extend loans, expanding the monetary base in response to productive demand.

2. Liquidity provision: By pooling deposits and maintaining fractional reserves, banks transform illiquid assets (loans) into liquid liabilities (deposits), providing the economy with a continuous supply of transaction money.

3. Risk transformation: Banks pool and diversify credit risk, converting idiosyncratic borrower risk into a portfolio risk that can be managed and priced more efficiently.

| REGULATORY BENCHMARK: Under Basel III (and the forthcoming Basel IV output floors effective 2025–2028), internationally active banks must maintain a Common Equity Tier 1 (CET1) ratio of at least 4.5%, a Tier 1 ratio of 6%, and a Total Capital ratio of 8%, plus a Capital Conservation Buffer of 2.5%. The Liquidity Coverage Ratio (LCR) and Net Stable Funding Ratio (NSFR) address short- and long-term liquidity respectively. |

Global banking is increasingly stratified. The BIS identifies 30 Global Systemically Important Banks (G-SIBs) — institutions whose failure would have cross-border consequences — and requires them to hold Additional Loss-Absorbing Capital (ALAC) surcharges of 1.0–3.5% of RWA. This tier-based approach reflects the lesson of 2008: not all bank failures are created equal.

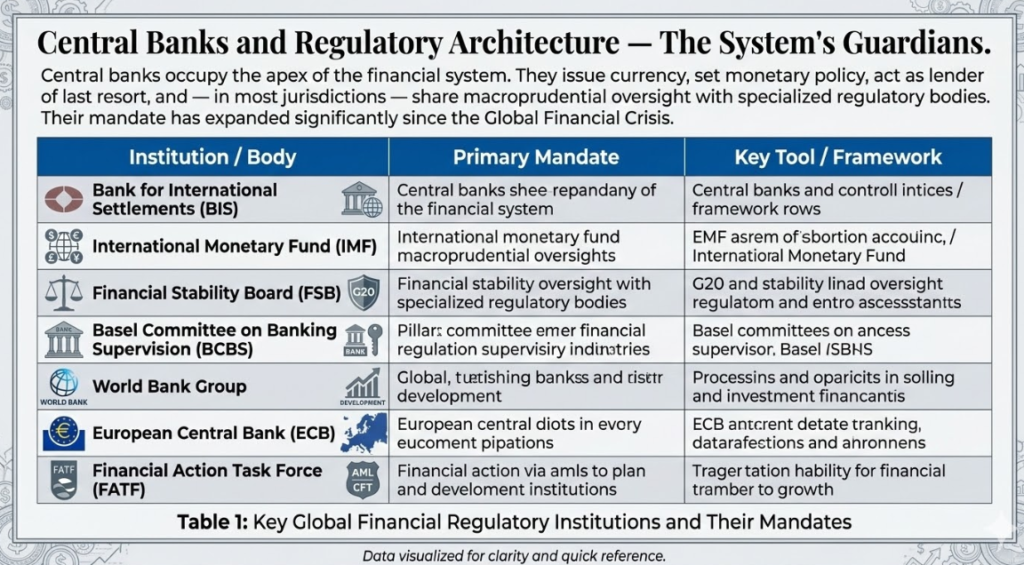

2.2 Central Banks and Regulatory Architecture — The System’s Guardians

Central banks occupy the apex of the financial system. They issue currency, set monetary policy, act as lender of last resort, and — in most jurisdictions — share macroprudential oversight with specialised regulatory bodies. Their mandate has expanded significantly since the Global Financial Crisis.

| Institution / Body | Primary Mandate | Key Tool / Framework |

| Bank for International Settlements (BIS) | Central bank of central banks; coordination of monetary and financial stability policy | Basel Accords, CPMI standards, FSB Secretariat |

| International Monetary Fund (IMF) | Global monetary cooperation, balance of payments support, financial surveillance | Article IV Consultations, FSAP, SDRs |

| Financial Stability Board (FSB) | Monitor and address systemic vulnerabilities across G20 jurisdictions | G-SIB list, NBFI monitoring, TLAC standards |

| Basel Committee on Banking Supervision (BCBS) | Set minimum global standards for bank capital and liquidity | Basel I / II / III / IV capital framework |

| World Bank Group | Development finance, poverty reduction, financial sector reform | IFC, MIGA, IBRD lending; FCI Advisory |

| European Central Bank (ECB) | Monetary union stability for the eurozone; Single Supervisory Mechanism | Asset Purchase Programmes, TLTRO, SREP |

| Financial Action Task Force (FATF) | Combat money laundering and terrorist financing globally | 40 Recommendations, grey/black list evaluations |

Table 1: Key Global Financial Regulatory Institutions and Their Mandates

The post-2008 consensus shifted central banking from narrow inflation targeting toward dual mandates encompassing financial stability. The result has been the institutionalisation of macroprudential tools: countercyclical capital buffers, sectoral capital requirements, systemic risk buffers, and — controversially — central bank balance sheet expansion through quantitative easing (QE) and, more recently, quantitative tightening (QT).

“The financial crisis demonstrated that the stability of individual institutions is necessary but not sufficient for the stability of the system as a whole. Macroprudential policy fills the gap.”

— BIS Annual Economic Report, 2023

2.3 Shadow Banking and Non-Bank Financial Intermediation (NBFI)

The term ‘shadow banking’ — coined by economist Paul McCulley in 2007 — describes the constellation of financial entities and activities that perform bank-like credit intermediation outside the regulatory perimeter of conventional banking supervision. The FSB has progressively refined this concept, now preferring Non-Bank Financial Intermediation (NBFI) to capture both the risks and the legitimate economic functions of this sector.

The NBFI ecosystem encompasses a diverse set of actors:

• Money Market Funds (MMFs): Provide short-term liquidity to corporations and governments; vulnerable to ‘run’ dynamics as demonstrated in March 2020 and September 2008.

• Hedge Funds: Employ leverage and derivatives strategies; interconnected with prime brokerage via investment banks. The collapse of Archegos Capital in 2021 demonstrated concentrated counterparty risk.

• Insurance Companies and Pension Funds: The largest institutional investors globally, with combined AUM exceeding $100 trillion. Increasingly important in long-duration bond and infrastructure markets.

• Private Credit / Direct Lending Funds: The fastest-growing NBFI segment, exceeding $1.5 trillion in AUM by 2024 (IMF Global Financial Stability Report). Provide credit to mid-market borrowers outside the public debt markets.

• Special Purpose Vehicles (SPVs) and Securitisation: Repackage pools of loans into structured securities (ABS, MBS, CDOs). Fundamental to mortgage finance and regulatory capital optimisation; but a key transmission mechanism in the 2008 crisis.

| CASE STUDY — BlackRock and the Rise of Institutional NBFI: With over $10 trillion in assets under management, BlackRock exemplifies the systemic significance of large asset managers. Its Aladdin risk management platform processes risk data for trillions in additional third-party assets, making it a critical piece of financial infrastructure. The FSB’s 2023 consultation on liquidity preparedness for margin and collateral calls reflects growing regulatory attention to asset manager systemic risk — an area previously associated exclusively with banks. |

2.4 Financial Technology (Fintech) — The Disruptive Fourth Pillar

Fintech is not merely a technology story — it is a structural reorganisation of financial intermediation. By disaggregating the traditional bank value chain into modular, API-accessible services, fintech has introduced new actors, new risks, and new possibilities for financial inclusion and operational efficiency.

| Fintech Segment | Description & Global Significance |

| Digital Payments & Mobile Money | M-Pesa (Kenya) demonstrated that mobile money could achieve 40%+ GDP transaction volumes in a low-income market, becoming the FSB’s reference case for financial inclusion fintech. Globally, real-time payment systems (FPS, UPI, PIX) are processing trillions in daily transactions. |

| Neobanks & Challenger Banks | Digital-first, app-native banks operating without branch networks. Regulated as full banks in most jurisdictions (EU Electronic Money Institution licence; FCA authorisation in the UK). Total global neobank customers exceeded 400 million by 2024. |

| Embedded Finance | The integration of financial services into non-financial platforms (e-commerce, ride-hailing, SaaS). Blurs the boundary between banks and technology companies; raises issues of data ownership and consumer protection. |

| RegTech & SupTech | Technology applied to regulatory compliance (RegTech) and supervisory processes (SupTech). Machine learning-based AML transaction monitoring; automated FRTB capital calculation; supervisory dashboards at the ECB and BIS. |

| Decentralised Finance (DeFi) | Blockchain-based financial protocols executing lending, trading, and settlement without intermediaries. The IMF’s 2023 Crypto Policy Note identified DeFi as requiring bespoke regulatory frameworks given its pseudonymous, cross-border, and algorithmically governed nature. |

| Central Bank Digital Currencies (CBDCs) | Digital forms of sovereign fiat currency. Over 130 central banks are in research or pilot phases (BIS CBDC Tracker, 2024). Atlantis, the BIS mCBDC Bridge (Project mBridge), links CBDC systems across jurisdictions for wholesale cross-border settlement. |

Table 2: Major Fintech Segments and Their Global Significance

Section 3: How the Pillars Interact — Mapping System Dynamics

The four pillars do not operate in isolation. Understanding a national financial system requires mapping the flows of funds, information, and risk between them. Three interaction mechanisms are especially critical to system stability.

3.1 The Credit Channel

Credit flows from commercial banks and NBFI entities into the real economy through the credit channel. Central banks influence this channel via policy rates (which set the floor for bank funding costs) and reserve requirements. When monetary policy tightens, bank lending standards rise, NBFI credit tightens, and the real economy contracts — a process the IMF terms financial conditions tightening.

The 2022–2024 global rate cycle demonstrated the asymmetric speed of this transmission: central bank rate hikes were transmitted rapidly to mortgage and corporate borrowing costs, while deposit rates lagged — generating significant interest margin benefits for banks but heightening pressure on leveraged borrowers and commercial real estate valuations globally.

3.2 The Interconnectedness Channel

Modern financial institutions are deeply interconnected through interbank lending markets, derivatives exposures, repo markets, and common asset holdings. This interconnectedness allows risk sharing but also creates contagion pathways. The BIS Global Systemic Risk Monitor and the IMF’s Financial Sector Assessment Programme (FSAP) use network analysis to map these exposures.

A practical illustration: in 2008, the failure of a US mortgage market — representing roughly 3% of global financial assets — triggered a systemic crisis because of the interconnections running through MBS securitisation, interbank funding, and derivatives counterparty risk. The post-crisis regulatory response — central clearing of standardised derivatives (EMIR, Dodd-Frank Title VII), mandatory bilateral margin requirements (BCBS-IOSCO Uncleared Margin Rules) — directly targeted these transmission channels.

3.3 The Confidence Channel

Financial systems are ultimately institutions of trust. Confidence — in the solvency of banks, the credibility of central banks, the enforceability of contracts — is not merely a soft complement to hard capital ratios; it is the system’s operating medium. When confidence falters, liquidity evaporates and solvency crises materialise.

This dynamic was observable in the March 2023 regional bank stress in the United States and the failure of Credit Suisse. In both cases, social media-accelerated deposit outflows demonstrated that the velocity of modern bank runs has outpaced historical supervisory response windows — a finding the Basel Committee has incorporated into its 2024 consultation on liquidity standards and the adequacy of the LCR framework.

“The speed at which depositor confidence can be lost in the digital age has rendered traditional run dynamics obsolete. Supervisors must adapt to instantaneous information environments.”

— BIS Working Paper No. 1140, 2023

Section 4: Global Regulatory Frameworks — Standards and Convergence

The global financial system operates across jurisdictions with varying legal traditions, institutional capacities, and political economies. International standard-setting bodies do not legislate directly — they publish principles, recommendations, and minimum standards that member jurisdictions implement domestically. Understanding the architecture of global financial regulation is essential for any institution operating across borders.

4.1 The Basel Framework — Capital and Liquidity Standards

The Basel Accords, developed by the Basel Committee on Banking Supervision (BCBS) and housed at the BIS, constitute the foundational international standard for bank capital adequacy. Their evolution reflects the successive crises and regulatory learning of four decades:

4. Basel I (1988): Introduced the 8% minimum Total Capital ratio against risk-weighted assets. Criticised for crude risk categories that incentivised regulatory arbitrage.

5. Basel II (2004): Introduced three pillars — minimum capital requirements, supervisory review, and market discipline. Permitted use of internal models (IRB approach), which contributed to underestimation of mortgage credit risk.

6. Basel III (2010–2019): Post-GFC response. Added CET1 minimum, Capital Conservation Buffer, Countercyclical Buffer, G-SIB surcharges, Leverage Ratio, LCR, and NSFR.

7. Basel IV / Basel III Final (2024–2028): Introduces output floors preventing internal models from generating RWA below 72.5% of the standardised approach. Reduces model variability and increases comparability of capital ratios globally.

| IMPLEMENTATION WATCH: As of 2025, the EU (CRR3/CRD6), UK (PRA CP16/22), US (NPR on Basel III Endgame), and other major jurisdictions are in various stages of transposing Basel IV. Divergences in implementation timelines and national discretions create competitive dynamics that the BCBS monitors through its Regulatory Consistency Assessment Programme (RCAP). |

4.2 The FSB and Systemic Risk Governance

The Financial Stability Board, established in 2009 by the G20, coordinates the work of national financial authorities and international standard-setting bodies. Its key workstreams include:

• G-SIB and G-SII Identification: Annual publication of Global Systemically Important Banks and Insurers, triggering enhanced supervision and capital/resolution requirements.

• NBFI Monitoring: Annual Global Monitoring Report on NBFI tracks the scale, risk profile, and regulatory coverage of non-bank credit intermediation across 29 jurisdictions representing 80%+ of global financial assets.

• Resolution Standards (TLAC): Total Loss-Absorbing Capacity requirements ensure G-SIBs maintain sufficient bail-inable liabilities to absorb losses in resolution without public funds — the single most important post-GFC structural reform for ending ‘too big to fail’.

• Climate Risk and Sustainable Finance: The FSB’s TCFD (Task Force on Climate-related Financial Disclosures) framework, now superseded by ISSB IFRS S2, has become the global standard for corporate and financial institution climate disclosure.

4.3 IMF Financial Surveillance — The FSAP Framework

The IMF’s Financial Sector Assessment Programme (FSAP) provides the most comprehensive diagnostic tool for national financial system vulnerabilities. Conducted periodically for all member countries (mandatory for G20 and other systemically significant jurisdictions), FSAPs assess:

• Bank solvency and liquidity under stress scenarios aligned with IMF macroeconomic baseline and adverse projections

• Regulatory compliance with Basel standards, IOSCO Principles, CPMI-IOSCO Principles for Financial Market Infrastructures

• Crisis management and resolution frameworks, including deposit insurance adequacy

• Macroprudential policy frameworks and their calibration to the financial cycle

• Financial inclusion, fintech regulation, and digital financial infrastructure readiness

The IMF’s Global Financial Stability Report (GFSR), published biannually, provides real-time analysis of global financial vulnerabilities — from leveraged loan market developments to crypto asset risks and sovereign debt sustainability. It is the single most widely cited reference for systemic risk assessment.

Section 5: Regional Perspectives — Global Approaches, Local Architectures

While international standards provide a common floor, financial systems reflect deep differences in history, political economy, and institutional capacity. The following comparative overview — illustrates the diversity of approaches to core system design questions.

| Dimension | Advanced Economy Model | Emerging / Developing Market Model |

| Banking Structure | Diversified: universal banks + specialised investment banks + neobanks. High intermediation depth (bank assets as % of GDP often >200%) | State-owned bank dominance in many markets; lower intermediation depth; rapid growth of mobile banking infrastructure |

| Capital Markets | Deep, liquid equity and bond markets; sophisticated derivatives infrastructure; significant NBFI sector | Shallower, less liquid; government bond markets often more developed than corporate debt; capital market development a policy priority (World Bank FCI) |

| Monetary Policy Framework | Inflation targeting or dual mandate (price + employment); sophisticated forward guidance; QE/QT toolbox | Often constrained by exchange rate considerations, dollarisation, or fiscal dominance; less policy independence |

| Regulatory Architecture | Independent central bank + separate prudential and conduct regulators (Twin Peaks or sector-based); high compliance intensity | Often integrated supervision in central bank; capacity constraints; IMF/FSB technical assistance programmes |

| Fintech Adoption | Regulatory sandbox regimes (FCA, MAS); open banking mandates (PSD2); CBDC pilots at advanced stage | Leapfrog adoption — mobile money before internet banking; fintech as primary tool for financial inclusion; lighter regulatory burden initially |

| ESG Integration | Mandatory climate disclosure (TCFD/ISSB); green taxonomy; sustainable finance roadmaps | Developing national green taxonomies; IFC/World Bank green bond facilitation; social bonds for inclusion |

Table 3: Comparative Financial System Architecture — Advanced vs. Emerging Markets

5.1 Case Study: The M-Pesa Model — Fintech-Led Financial Inclusion

No case study better illustrates the transformative potential of fintech for financial systems in emerging markets than the mobile money ecosystem pioneered in East Africa. At its peak, M-Pesa processed transactions equivalent to over 40% of Kenya’s GDP annually — through a network of mobile agents rather than bank branches.

The M-Pesa architecture achieved three things simultaneously: it bypassed the infrastructure gap of traditional banking; it created a documented transaction record enabling credit scoring for the previously unbanked; and it generated a float of customer deposits that, under Kenyan Central Bank regulation, is ring-fenced in prudentially regulated commercial bank trust accounts — protecting users while limiting systemic deposit substitution.

The BIS-CPMI has used this model to inform guidelines for e-money regulation globally, emphasising three design principles: fund safeguarding, interoperability, and consumer protection. The World Bank’s Financial Inclusion Action Plan reflects these same principles, targeting 1 billion additional people brought into formal financial systems by 2030.

Section 6: Risk Management — The System’s Immune System

Effective risk management at the institutional and systemic level is the mechanism by which financial systems absorb shocks without catastrophic failure. The post-GFC regulatory architecture has dramatically expanded the scope and sophistication of required risk management frameworks.

6.1 Institutional Risk Management Best Practices

For individual financial institutions, global best practice in risk management aligns with the Three Lines of Defence model endorsed by the Institute of Internal Auditors (IIA) and embedded in supervisory guidance from the ECB, Federal Reserve, and FCA:

8. First Line — Business Units: Own and manage risks within approved risk appetite frameworks. Responsible for day-to-day risk identification, assessment, and mitigation.

9. Second Line — Risk Management and Compliance: Provide oversight, policies, and independent challenge to business line risk decisions. Include the Chief Risk Officer function, Compliance, and Finance.

10. Third Line — Internal Audit: Provide independent assurance to the Board and senior management on the adequacy and effectiveness of governance, risk management, and internal controls.

Modern best practice extends this framework to encompass:

• Integrated Stress Testing: Bank-level stress testing aligned with supervisory scenarios (EBA EU-wide stress test; Federal Reserve DFAST/CCAR; PRA concurrent stress test). Results drive capital planning, dividend policy, and strategic decision-making.

• Climate and ESG Risk: Physical and transition risk integration into credit risk models, ICAAP, and ILAAP. Mandated by ECB supervisory expectations (November 2020 guide) and increasingly by supervisors in the NGFS network (Network for Greening the Financial System, 120+ member central banks).

• Operational Resilience: Post-COVID supervisory focus on technology resilience, third-party/outsourcing risk, and cyber security. The EU’s Digital Operational Resilience Act (DORA, effective January 2025) establishes the most comprehensive operational resilience framework globally.

• Recovery and Resolution Planning: G-SIBs and domestic SIBs are required to maintain credible recovery plans (triggers, options, playbooks) and resolution plans (living wills) demonstrating resolvability without public funds.

6.2 Macroprudential Risk Management

At the system level, macroprudential authorities employ a toolkit developed largely after 2008 to address the procyclicality of the financial system — its tendency to amplify rather than dampen economic cycles:

| Macroprudential Tool | Function & Application |

| Countercyclical Capital Buffer (CCyB) | Accumulates CET1 capital in periods of excessive credit growth; released in downturns to support lending. Used actively by the BIS and over 50 jurisdictions. |

| Systemic Risk Buffer (SyRB) | Addresses structural systemic risks specific to a financial sector (e.g., concentrated mortgage market). Jurisdiction-specific calibration. |

| Loan-to-Value (LTV) and Debt-to-Income (DTI) Limits | Borrower-based measures limiting mortgage or consumer credit relative to property value or income. Most effective tool for cooling overheated housing markets without raising policy rates. |

| Additional G-SIB / D-SIB Capital Surcharges | Institution-based measures requiring systemically important banks to hold additional capital commensurate with their systemic footprint. |

| Leverage Ratio | Simple non-risk-based backstop to risk-weighted capital requirements; limits total balance sheet leverage. Basel III minimum: 3% Tier 1 / Total Exposures. |

| NSFR / LCR | Liquidity tools requiring banks to maintain sufficient stable funding over 1 year (NSFR) and a buffer of High-Quality Liquid Assets against 30-day stressed outflows (LCR). |

Table 4: Global Macroprudential Toolkit — Instruments and Applications

Section 7: ESG Integration in Global Banking — From Commitment to Architecture

Sustainable finance has moved from a values statement to a structural feature of global financial governance. The integration of Environmental, Social, and Governance (ESG) factors into financial institutions’ strategies, risk management, capital allocation, and disclosure frameworks is now a regulatory expectation in the EU, UK, Singapore, Hong Kong, and progressively across all G20 jurisdictions.

7.1 The Regulatory Landscape for Sustainable Finance

• EU Sustainable Finance Disclosure Regulation (SFDR): Classifies investment products as Article 6 (no ESG integration), Article 8 (ESG promoted), or Article 9 (sustainable investment objective). Binding on all EU financial market participants.

• EU Taxonomy Regulation: Defines which economic activities qualify as environmentally sustainable, providing a science-based taxonomy for green investment. Aligned with the Paris Agreement 1.5°C pathway.

• ISSB IFRS S1 & S2: The International Sustainability Standards Board’s global baseline for sustainability-related financial disclosures. Adopted or incorporated into national regimes in over 20 jurisdictions. Supersedes the TCFD framework.

• NGFS Climate Scenarios: Used by over 120 central banks and supervisors for climate scenario analysis in FSAPs, stress tests, and supervisory expectations. Provides three transition pathway scenarios: Orderly, Disorderly, and Hot House World.

• Principles for Responsible Banking (PRB): UNEP FI framework adopted by over 300 banks globally, requiring alignment of business strategy with the SDGs and Paris Agreement through time-bound targets and independent assurance.

“Climate change is a source of financial risk — and it is our job to ensure the financial system is resilient to that risk. Green finance is not a niche; it is the future of finance.”

— Mark Carney, former Governor of the Bank of England and Bank of Canada, UN Special Envoy for Climate Action and Finance

7.2 ESG Risk in Practice — What Banks Must Do

Leading global financial institutions have operationalised ESG risk in the following ways:

• Credit Risk: Integration of physical climate risk (flood, heat, drought) and transition risk (carbon price, stranded assets) into probability of default (PD) and loss given default (LGD) models for corporate and real estate exposures.

• Portfolio Alignment: Science-Based Targets initiative (SBTi) for Financial Institutions requires banks to set portfolio-level decarbonisation targets covering financed emissions (Scope 3, Category 15). Measured using the PACTA or SBTi FI methodology.

• Green Bonds and Sustainable Lending: Issuance of Green, Social, and Sustainability (GSS) bonds aligned with ICMA Green Bond Principles. Sustainability-linked loans (SLLs) tie pricing to KPI performance, incentivising borrower transition.

• Governance: Board-level ESG committees; Chief Sustainability Officer roles; ESG-linked executive compensation. Increasingly required by the ECB, UK FRC, and SEC’s proposed climate disclosure rules.

Section 8: Digital Transformation — Rebuilding the System’s Infrastructure

The digital transformation of financial services is not merely an efficiency story — it is a fundamental re-engineering of financial infrastructure, with systemic implications that regulators, institutions, and policymakers are only beginning to fully map.

8.1 Core Banking Modernisation

The legacy technology infrastructure of large commercial banks — built on mainframe architectures dating to the 1970s and 1980s — represents a growing operational risk and strategic constraint. Core banking modernisation programmes, typically spanning 5–10 years and costing hundreds of millions of dollars, are underway at institutions globally.

The strategic imperative is clear: cloud-native, API-first, microservices-based core banking platforms enable real-time processing, data analytics, and the rapid deployment of new products. They are also prerequisites for open banking participation and embedded finance partnerships. The migration risk, however, is significant — the FSB and national supervisors have highlighted the concentration of cloud services among three hyperscale providers (AWS, Microsoft Azure, Google Cloud) as a structural operational risk requiring dedicated regulatory attention.

8.2 Artificial Intelligence in Financial Services

AI and machine learning are reshaping financial services across the value chain. Key applications with systemic implications include:

• AML/CFT and Financial Crime: AI-powered transaction monitoring has increased detection rates while reducing false positives by orders of magnitude relative to rules-based systems. The FATF’s 2023 Guidance on Digital Transformation endorses AI-based AML provided explainability and model governance requirements are met.

• Credit Underwriting: Alternative data (telco usage, e-commerce behaviour, social patterns) integrated into credit models is expanding access to credit for thin-file borrowers — addressing financial inclusion — but raises fair lending, data privacy (GDPR), and model risk concerns.

• Algorithmic Trading and Market Making: AI-driven market making has improved liquidity in many asset classes, but also contributed to flash crashes and correlated volatility events. The SEC, FCA, and ESMA have all issued guidance on algorithmic trading risk controls.

• Generative AI: Large Language Models (LLMs) are being applied to regulatory reporting, document analysis, customer service, and investment research. The BIS Innovation Hub is conducting research on systemic implications; IOSCO published its first AI in Capital Markets report in 2024.

| REGULATORY SPOTLIGHT: The EU AI Act (effective 2024–2026) classifies most credit scoring and AML applications as ‘high-risk’ AI systems, requiring conformity assessments, human oversight, transparency, and data governance standards. This creates compliance obligations for financial institutions using AI in consequential decisions — aligning with the BIS’s principles for effective AI governance in finance. |

8.3 Central Bank Digital Currencies (CBDCs) — The Next Infrastructure Layer

The potential introduction of retail and wholesale CBDCs represents the most significant redesign of monetary infrastructure in a generation. CBDCs could:

• Enable direct central bank-to-household transmission of monetary policy, potentially eliminating the ‘banks as intermediaries’ channel for some monetary operations

• Provide a risk-free digital settlement asset for wholesale transactions, reducing counterparty and settlement risk

• Enable programmable money — smart contract-based conditional payments that could revolutionise trade finance, public transfers, and automated compliance

• Pose disintermediation risk to commercial banks if retail adoption is high, as depositors shift funds from private bank deposits to sovereign digital currency

The BIS’s Project mBridge (with central banks from China, Hong Kong, Thailand, UAE, and Saudi Arabia) is the most advanced multi-jurisdiction wholesale CBDC infrastructure experiment. The IMF’s Digital Money Framework and the BIS Annual Economic Report 2023 both emphasise that CBDC design choices — account vs. token-based, retail vs. wholesale, interest-bearing vs. zero-interest, anonymous vs. identified — have profound implications for monetary sovereignty, financial stability, and privacy.

Section 9: Best Practices — Building a Resilient Financial Institution

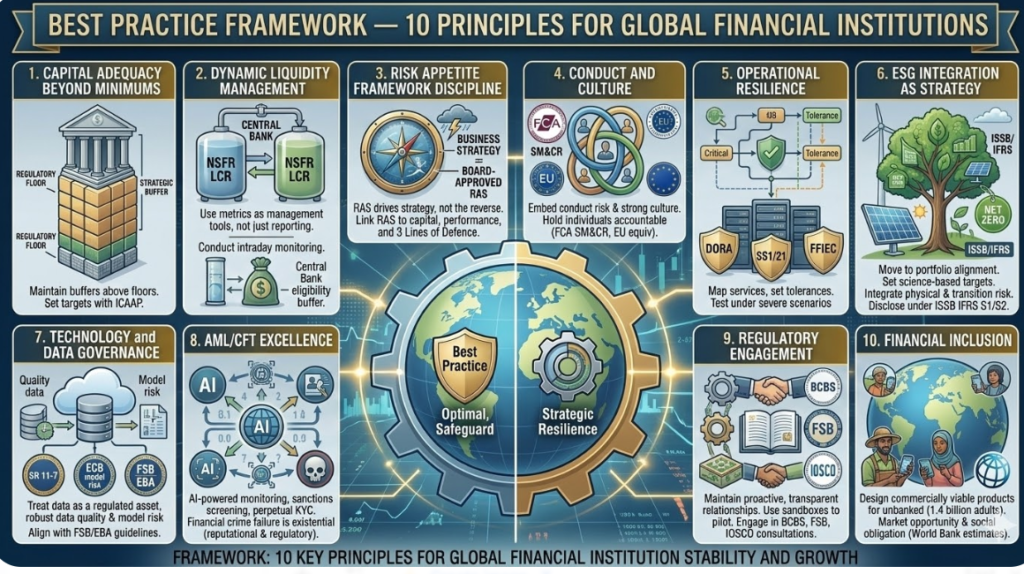

Drawing on the analytical framework above, we distil the following operational best practices for financial institutions seeking to build resilience, comply with global standards, and position for the system of tomorrow.

| BEST PRACTICE FRAMEWORK — 10 PRINCIPLES FOR GLOBAL FINANCIAL INSTITUTIONS |

| 1. Capital Adequacy Beyond Minimums: Maintain capital buffers materially above regulatory minimums to preserve strategic flexibility. Internal capital targets should be set using ICAAP outcomes, not regulatory floors. |

| 2. Dynamic Liquidity Management: Implement LCR and NSFR as management tools, not just reporting metrics. Conduct intraday liquidity monitoring and maintain a Central Bank eligibility buffer for stressed access. |

| 3. Risk Appetite Framework Discipline: Ensure the Board-approved Risk Appetite Statement (RAS) drives business strategy — not the reverse. Link RAS to capital planning, performance management, and the Three Lines of Defence. |

| 4. Conduct and Culture: Embed conduct risk management and a strong risk culture throughout the organisation. The FCA’s Senior Managers and Certification Regime (SM&CR) and the equivalent EU frameworks hold individuals accountable for conduct failures. |

| 5. Operational Resilience: Map critical business services, set impact tolerances, and test resilience under severe but plausible disruption scenarios. Comply with DORA (EU), SS1/21 (UK PRA), and FFIEC guidance (US) on operational resilience. |

| 6. ESG Integration as Strategy: Move beyond disclosure compliance to genuine portfolio alignment. Set science-based targets, integrate physical and transition climate risk into all material credit and investment decisions, and disclose under ISSB IFRS S1/S2. |

| 7. Technology and Data Governance: Treat data as a regulated asset. Implement robust data quality frameworks, model risk management policies (SR 11-7 / ECB model risk guidance), and cloud risk management aligned with FSB/EBA outsourcing guidelines. |

| 8. AML/CFT Excellence: Invest in AI-powered transaction monitoring, sanctions screening, and perpetual KYC processes. Failure in financial crime compliance carries existential reputational and regulatory consequences, as demonstrated by multiple global enforcement actions. |

| 9. Regulatory Engagement: Maintain proactive, transparent relationships with supervisors. Use regulatory sandbox opportunities to pilot innovations. Engage in BCBS, FSB, and IOSCO consultation processes to shape the standards that will govern the industry. |

| 10. Financial Inclusion: Where commercially viable, design products and distribution models that extend financial access. The World Bank estimates that 1.4 billion adults remain unbanked globally — a market opportunity as much as a social obligation. |

Section 10: Visual Data

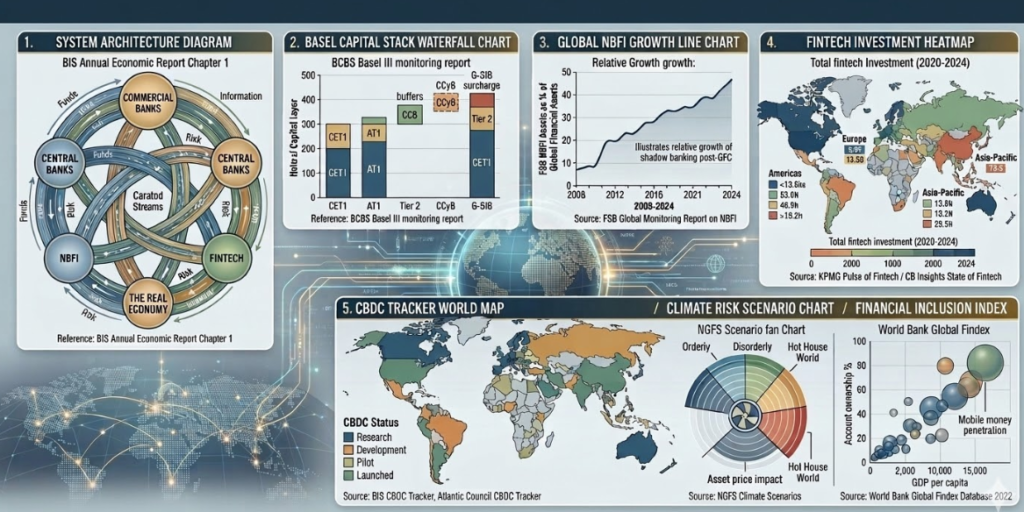

| System Architecture Diagram | Circular flow diagram showing funds, risk, and information flows between commercial banks, central banks, NBFI, fintech, and the real economy. Reference: BIS Annual Economic Report Chapter 1. |

| Basel Capital Stack Waterfall Chart | Stacked bar chart showing CET1, AT1, Tier 2, and buffers (CCB, CCyB, G-SIB surcharge) for a hypothetical G-SIB. Reference: BCBS Basel III monitoring report. |

| Global NBFI Growth Line Chart | FSB NBFI assets as % of global financial assets, 2008–2024. Illustrates relative growth of shadow banking post-GFC. Source: FSB Global Monitoring Report on NBFI. |

| Fintech Investment Heatmap | Geographic heat map of global fintech investment by region (2020–2024). Source: KPMG Pulse of Fintech / CB Insights State of Fintech. |

| CBDC Tracker World Map | Choropleth map showing CBDC status by country (research / development / pilot / launched). Source: BIS CBDC Tracker, Atlantic Council CBDC Tracker. |

| Climate Risk Scenario Chart | NGFS scenario fan chart showing asset price impact under Orderly, Disorderly, and Hot House World scenarios. Source: NGFS Climate Scenarios for Central Banks and Supervisors. |

| Financial Inclusion Index | World Bank Global Findex bubble chart: account ownership % vs. GDP per capita with mobile money penetration as bubble size. Source: World Bank Global Findex Database 2022. |

Conclusion: Building the Resilient Financial System of the Future

The anatomy of a financial system is not static. It is a living, evolving architecture shaped by technological disruption, regulatory adaptation, macroeconomic cycles, and the shifting demands of society. The commercial banks, shadow banking entities, fintech innovators, and regulatory institutions that together constitute this architecture are in a period of profound transformation — arguably the most significant since the post-Bretton Woods financial liberalisation of the 1970s and 1980s.

Five structural shifts are reshaping the system in real time:

• Digital infrastructure replacement: Core banking modernisation, real-time payment networks, and CBDCs are rebuilding the plumbing of financial intermediation.

• AI-driven operations: Machine learning is permeating risk management, compliance, product design, and customer service — creating new efficiencies and new model risk.

• Regulatory densification: Basel IV, DORA, SFDR, the EU AI Act, and ISSB IFRS S1/S2 collectively represent the most demanding compliance environment in financial history.

• Climate and nature risk mainstreaming: ESG is transitioning from voluntary reporting to mandatory risk management and capital allocation constraint.

• Fintech-banking convergence: The boundary between regulated banks and technology platforms is dissolving — raising questions about regulatory perimeter adequacy and competitive fairness.

For financial professionals, the strategic imperative is clear: build institutions that are simultaneously capital-strong, operationally resilient, technologically sophisticated, and socially responsible. These are not trade-offs — they are the integrated attributes of the durable financial institution.

For policymakers, the challenge is to maintain the internationally coordinated regulatory architecture that prevents race-to-the-bottom dynamics, while providing sufficient flexibility for innovation and national context. The BIS, IMF, and FSB provide the multilateral scaffolding — but national implementation determines outcomes.

The financial system’s ultimate function is simple: to allocate capital productively and inclusively, to price and distribute risk efficiently, and to provide the payment infrastructure on which modern economies depend. The anatomy described in this article is the means to that end. Understanding it is the foundation of effective participation in the global financial economy.

Expert Perspectives

“The lesson of the Global Financial Crisis is not that banks are inherently fragile — it is that fragility is a function of design. Capital, liquidity, and governance matter. The Basel framework exists to make fragility a choice, not a destiny.”

— Generalised from Basel Committee on Banking Supervision, Annual Report 2023

“Financial inclusion and financial stability are not competing objectives. A financial system that excludes half its potential participants is not merely unjust — it is inefficient and more vulnerable to systemic shock.”

— Composite perspective, IMF Financial Inclusion Strategy & World Bank FCI Group

“The central bank of the future will be a data institution as much as a monetary institution. Real-time payments data, CBDC transaction flows, and AI-driven surveillance tools will transform macroprudential policymaking.”

— BIS Innovation Hub Strategic Report 2023–2025

Frequently Asked Questions (FAQ)

Q: What is the difference between shadow banking and traditional banking, and why does it matter for financial stability?

A: Shadow banking — or Non-Bank Financial Intermediation (NBFI) in FSB terminology — refers to credit intermediation conducted outside the regulatory perimeter of conventional banking supervision. This includes money market funds, hedge funds, private credit funds, and securitisation vehicles. These entities perform similar economic functions to banks (maturity transformation, credit creation, leverage) but without equivalent capital requirements, deposit insurance, or lender of last resort access. Their systemic significance lies in their interconnection with traditional banks and their role in amplifying credit cycles. The FSB’s annual NBFI Monitoring Report — covering $218 trillion in global NBFI assets (2023) — is the essential reference for tracking this sector’s evolution and risk profile.

Q: How is Basel IV different from Basel III, and what should banks be doing to prepare?

A: Basel IV — formally the finalisation of Basel III reforms published by the BCBS in December 2017 — introduces output floors preventing banks from using internal models to produce RWA below 72.5% of the Standardised Approach calculation. This significantly increases RWA for banks that previously relied on internal models to minimise capital requirements, particularly in mortgage, low-default corporate, and trading book portfolios. Banks preparing for Basel IV (effective from 2025 in the EU/UK, with transition to 2028–2030) should: conduct parallel run RWA calculations under both current and Basel IV frameworks; stress-test capital ratios under the output floor; review business line profitability and pricing models; and engage with national supervisor implementation timelines and discretions. The BCBS’s Regulatory Consistency Assessment Programme (RCAP) monitors cross-jurisdictional consistency of implementation.

Q: What are the most important emerging trends in global financial regulation for the next five years?

A: Five trends will dominate the global financial regulatory agenda to 2030: (1) Basel IV full implementation and supervisory convergence across G20 jurisdictions; (2) Climate and sustainability risk integration — mandatory under NGFS frameworks and increasingly hard-wired into Pillar 2 ICAAP/ILAAP expectations; (3) Digital operational resilience — DORA implementation in the EU and equivalent regimes globally; (4) AI governance — IOSCO and BCBS work on AI risk management, model risk, and systemic implications of correlated AI decision-making; (5) CBDC deployment and its implications for monetary policy transmission, banking disintermediation, and cross-border payment architecture. Financial institutions that anticipate and invest in capabilities for all five dimensions will be best positioned for the regulatory environment of 2030.

Key References and Further Reading

All references below link to primary source documents available in the public domain:

• Basel Committee on Banking Supervision — Basel III: A global regulatory framework for more resilient banks and banking systems (BIS.org/bcbs)

• Financial Stability Board — Global Monitoring Report on Non-Bank Financial Intermediation 2023 (FSB.org)

• International Monetary Fund — Global Financial Stability Report (October 2024) (IMF.org/GFSR)

• Bank for International Settlements — Annual Economic Report 2024 (BIS.org/AER)

• World Bank — Global Findex Database 2022: The State of Financial Inclusion (WorldBank.org/Findex)

• Network for Greening the Financial System — NGFS Climate Scenarios for Central Banks and Supervisors (NGFS.net)

• ISSB — IFRS S1 General Requirements and IFRS S2 Climate-related Disclosures (IFRS.org/ISSB)

• BIS Innovation Hub — Work Programme and CBDC Research (BIS.org/Innovation)

• FATF — Guidance on Digital Transformation and AML/CFT (FATF-GAFO.org)

• European Banking Authority — Basel IV / CRR3 Implementation Resources (EBA.europa.eu)

Global Banking & Financial Governance Series | Aligned with BIS, IMF & Basel IV Standards