From Brick-and-Mortar to Digital-First: How the Global Banking System Is Being Reinvented

Introduction: The $180 Trillion Question

The global banking system manages assets exceeding $180 trillion — a figure that dwarfs the GDP of any single nation. Yet the institutions managing that wealth are being fundamentally disrupted. According to the World Economic Forum, over 33% of traditional banking revenue is at risk of displacement by FinTech and digital-native competitors by 2030.

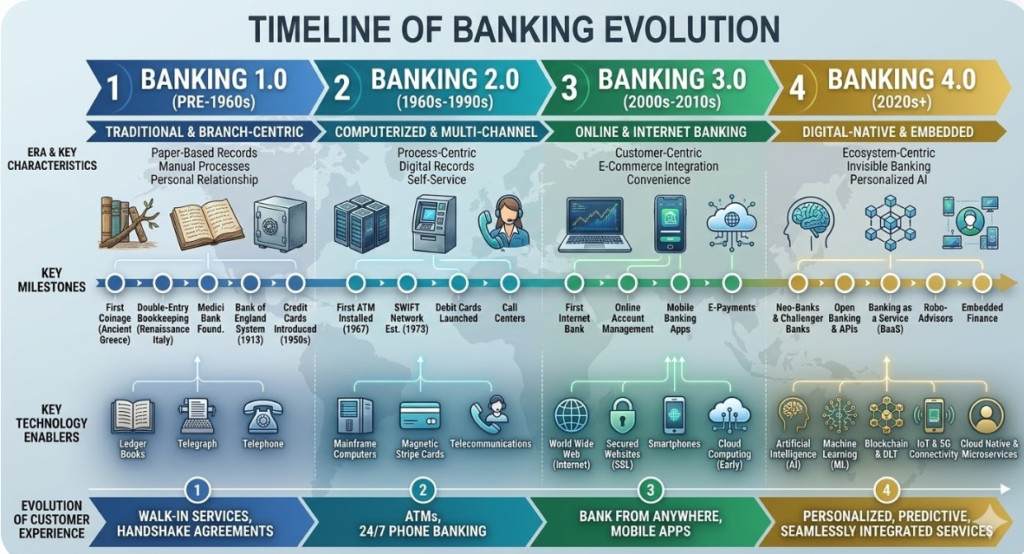

Welcome to Banking 4.0 — not just an upgrade, but a philosophical and structural reimagination of what a bank is, who it serves, and how it operates. Where Banking 1.0 was the ledger and vault, Banking 2.0 brought ATMs and online portals, and Banking 3.0 introduced mobile-first interfaces, Banking 4.0 dissolves the institution itself — embedding financial services invisibly into everyday life through APIs, AI, and platform ecosystems.

This post explores the transition from traditional brick-and-mortar models to Neo-banks, Banking-as-a-Service (BaaS), and digital-first institutions. Whether you are a finance professional, policy strategist, RegTech innovator, or institutional investor, understanding this transformation is no longer optional — it is imperative.

“The biggest change in banking is not technology. It’s the redefinition of what banking means in a connected, data-driven world.” — Global Financial Innovation Network (GFIN), 2023 Report

What Is Banking 4.0? Definitions and Core Concepts

Financial Intermediation in the Digital Age

Financial intermediation — the process by which banks collect deposits and channel them into productive loans and investments — remains the core function of global banking. What has changed is who performs this function and how.

In the Banking 4.0 paradigm, intermediation is increasingly performed by:

- Neo-banks (fully digital, branchless banks)

- Banking-as-a-Service (BaaS) providers (API-layer banks enabling third-party financial products)

- Platform-based lenders (embedded finance within e-commerce, SaaS, or super-apps)

- Decentralized Finance (DeFi) protocols (blockchain-based lending and borrowing without traditional intermediaries)

Key Terms Every Finance Professional Must Know

| Term | Definition |

| Maturity Transformation | The process of borrowing short-term funds (deposits) and lending them long-term (mortgages, corporate loans) — the classic banking risk |

| Fiduciary Responsibility | The legal and ethical obligation of financial institutions to act in the best interest of clients |

| Banking-as-a-Service (BaaS) | A model where licensed banks offer their infrastructure via APIs so non-bank companies can offer financial products |

| Open Banking | A regulatory and technical framework enabling third-party access to bank data with customer consent (enabled by standards like PSD2 in the EU) |

| Embedded Finance | The integration of financial services (payments, lending, insurance) into non-financial platforms and apps |

| RegTech | Technology applied to regulatory compliance processes — AI-driven KYC, AML monitoring, reporting automation |

| API Economy | An ecosystem where software systems share data and capabilities through Application Programming Interfaces |

Timeline of Banking Evolution — Banking 1.0 to 4.0, with key milestones and technology enablers

The Global Context — How Regions Are Navigating the Shift

The Basel Committee and International Regulatory Architecture

No discussion of global banking governance is complete without the Basel Committee on Banking Supervision (BCBS), which operates under the Bank for International Settlements (BIS). The Committee’s Basel III and emerging Basel IV frameworks establish minimum capital adequacy requirements, leverage ratios, and liquidity standards that every globally significant institution must observe.

Key Basel III pillars shaping Banking 4.0:

- Minimum Capital Requirements — Common Equity Tier 1 (CET1) ratio of at least 4.5% of risk-weighted assets

- Supervisory Review Process — Internal assessment of institution-specific risks beyond minimum thresholds

- Market Discipline — Mandatory disclosure standards to ensure transparency for investors and regulators

As Neo-banks and BaaS providers grow, the BCBS has signaled increasing scrutiny over non-bank financial intermediaries (NBFIs) — a category that now includes FinTechs, crypto platforms, and digital lenders. [→ External link suggestion: BIS/BCBS Publications at bis.org]

The IMF and World Bank — Financial Inclusion as a Global Imperative

The International Monetary Fund (IMF) and World Bank have placed financial inclusion at the heart of global development strategy. The World Bank’s Global Findex Database (2022) reports that 1.4 billion adults worldwide remain unbanked — yet 76% of them own a mobile phone. This data point is the defining opportunity for Banking 4.0.

The IMF’s Financial Sector Assessment Programs (FSAPs) evaluate member countries’ financial system stability, identifying gaps where digital banking models can serve underserved populations while maintaining macroprudential stability.

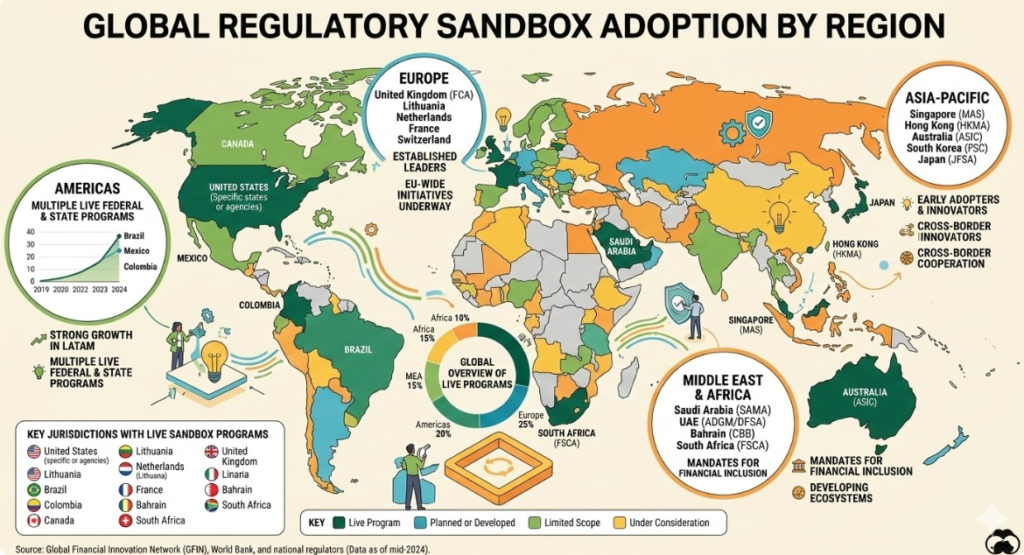

The FCA’s Sandbox Model — Regulatory Innovation at Scale

The UK’s Financial Conduct Authority (FCA) pioneered the concept of regulatory sandboxes — controlled environments where FinTech firms can test products with real customers under modified regulatory conditions. This model has since been replicated across:

- Singapore (Monetary Authority of Singapore — MAS)

- Australia (ASIC Innovation Hub)

- European Union (under the Digital Finance Strategy)

- United Arab Emirates (ADGM RegLab)

Sandboxes have become a cornerstone of Banking 4.0 governance, allowing innovation without systemic risk.

Global Regulatory Sandbox Adoption by Region — showing jurisdictions with live sandbox programs

From Traditional Banks to Neo-Banks — The Architecture of Change

The Traditional Bank Model — Strengths and Structural Inertia

For centuries, the brick-and-mortar banking model offered unmatched advantages: physical trust, branch networks, balance sheet depth, and regulatory permanence. Global institutions built on this model — names recognizable across the Rothschild banking dynasty’s 200+ year history to modern universal banks — accumulated vast client relationships and institutional knowledge.

However, this model carries significant structural costs:

- Cost-to-income ratios averaging 55–65% for traditional banks globally (McKinsey Global Banking Annual Review, 2023)

- Legacy IT infrastructure — many global banks run on COBOL-based core systems dating to the 1970s

- Regulatory compliance overhead — Basel III compliance alone costs large banks an estimated $50–100M annually

- Branch network expenses — physical infrastructure that digital-native competitors simply don’t carry

Neo-Banks — Digital-First, Customer-Obsessed

Neo-banks (also called challenger banks) are fully digital financial institutions operating without physical branches. They are characterized by:

- Mobile-first onboarding (account opening in under 5 minutes)

- Real-time notifications and spending analytics

- Transparent, low-fee structures often subsidized by interchange revenue

- API-driven architecture enabling rapid product iteration

- Customer experience scores consistently outperforming traditional peers

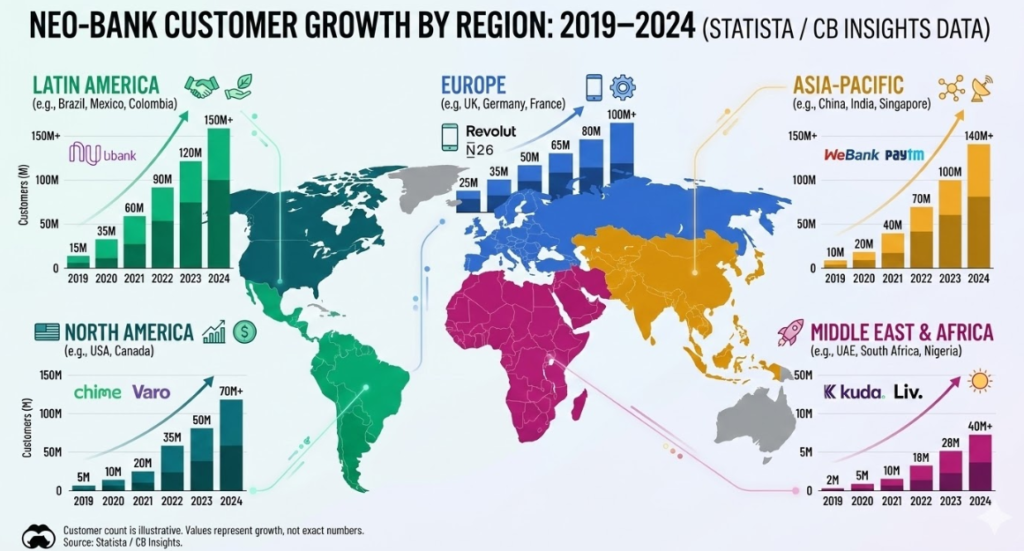

Neo-banks have captured over 300 million customers globally as of 2023 (Finder.com Global Neo-Bank Report). While profitability at scale remains a challenge for many, leaders in the sector have demonstrated viable unit economics through diversified revenue streams including premium subscriptions, B2B BaaS licensing, and lending products.

Global Neo-Bank Case Study Archetypes:

| Region | Model Type | Key Innovation |

| Europe | Regulatory-licensed digital bank | Multi-currency accounts, global money transfers |

| Africa | Mobile money-first (M-Pesa model) | Agent network + SIM-based banking |

| Asia-Pacific | Super-app embedded banking | Payments, investments, insurance in one platform |

| Latin America | Credit-led digital bank | Serving thin-file customers via alternative data |

| North America | Challenger bank | Fee-free checking, early paycheck access |

Neo-Bank Customer Growth by Region, 2019–2024, Source: Statista / CB Insights

The M-Pesa Blueprint — Financial Inclusion at Planetary Scale

Perhaps no Banking 4.0 case study is more studied than M-Pesa, the mobile money service launched in Kenya and now operating across multiple continents. What began as a simple SMS-based money transfer service has evolved into a full financial ecosystem — savings, credit, insurance, and merchant payments — all accessible via basic mobile phones.

M-Pesa’s success provides three foundational lessons for Banking 4.0 globally:

- Distribution before product — Agent networks create trust in low-connectivity regions before digital-only solutions are viable

- Interoperability is infrastructure — The value of a payment network scales with universal access (Metcalfe’s Law applied to finance)

- Regulatory partnership is non-negotiable — M-Pesa’s success was enabled by a forward-looking central bank willing to authorize a novel model

The IMF has cited M-Pesa as a model for regulatory-enabled financial innovation that reduced poverty and increased economic participation — a benchmark for the intersection of Banking 4.0 and sustainable development goals (SDGs).

Banking-as-a-Service (BaaS) — The Invisible Bank Revolution

How BaaS Works — A Technical Primer

Banking-as-a-Service is the model through which licensed banking institutions expose their core infrastructure — accounts, payments, lending, compliance — via APIs, allowing non-bank companies to build financial products without a banking license.

The BaaS stack operates in three layers:

Layer 1 — Regulated Bank (License Holder)

↓ Core banking infrastructure, balance sheet, regulatory compliance

Layer 2 — BaaS Platform (Middleware)

↓ API abstraction, developer tools, compliance orchestration

Layer 3 — Non-Bank Company (Product Builder)

↓ End-user product (e.g., a ride-hailing app offering driver payments)

This architecture is transforming industries far beyond finance. Airlines, retail chains, telecommunications companies, and SaaS platforms are embedding financial products — branded debit cards, earned wage access, invoice financing — into their core offerings, creating what analysts call “ambient banking” or the invisible bank.

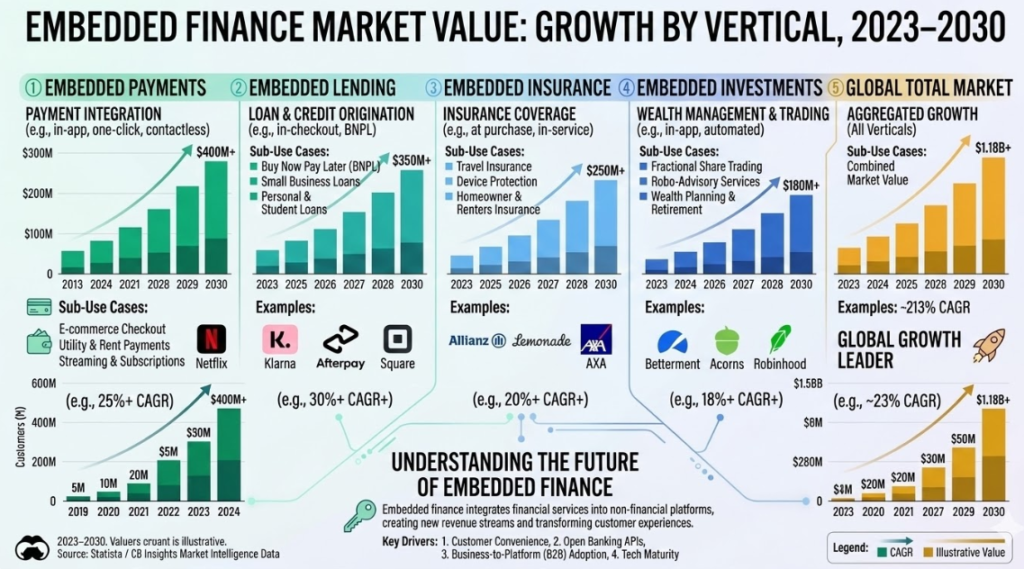

Embedded Finance — The $7 Trillion Opportunity

According to Accenture’s Embedded Finance: Who Will Lead the Next Payments Revolution? (2022), the total addressable market for embedded finance globally could exceed $7 trillion in transaction value by 2030.

Key drivers include:

- Super-app proliferation in Asia-Pacific (where single apps handle messaging, payments, shopping, and lending for hundreds of millions of users)

- Platform economy growth — gig economy platforms embedding earned wage access and micro-insurance

- SME financing gaps — e-commerce platforms offering working capital to sellers using transaction data as creditworthiness signals

- API standardization — Open Banking regulations (PSD2, CDR in Australia, FAPI standards globally) reducing integration friction

Embedded Finance Market Value by Vertical (Payments, Lending, Insurance, Investments) 2023–2030

Global Best Practices in Banking 4.0

Regulatory Compliance — Navigating a Multi-Jurisdictional World

For institutions operating globally, regulatory compliance in Banking 4.0 requires a layered, technology-enabled framework:

1. Know Your Customer (KYC) and Anti-Money Laundering (AML) The Financial Action Task Force (FATF) sets global AML/CFT (Counter Financing of Terrorism) standards adopted by 200+ jurisdictions. Digital banks must implement:

- Automated identity verification (biometric, document OCR)

- Perpetual KYC (continuous monitoring rather than periodic reviews)

- Transaction monitoring with AI-based anomaly detection

2. Data Privacy and Sovereignty

- GDPR (EU) — extraterritorial data protection obligations

- PDPA variants across Asia-Pacific

- Cross-border data transfer frameworks — essential for global BaaS models

3. Capital and Liquidity Requirements Even Neo-banks and BaaS providers must maintain adequate capital buffers. The Basel III Liquidity Coverage Ratio (LCR) and Net Stable Funding Ratio (NSFR) apply wherever a banking license is held.

4. Consumer Protection Standards The SEC (in securities contexts), FCA, and equivalent bodies globally mandate disclosure, fair treatment, and complaint handling obligations that apply equally to digital and traditional institutions.

Operational Excellence in Digital Banking

Best-in-class Banking 4.0 institutions share several operational hallmarks:

- Cloud-native core banking — Moving from monolithic legacy systems to cloud-based, modular architectures (microservices) enabling real-time processing and infinite scalability

- DevSecOps culture — Security integrated into software development pipelines from day one

- 99.99% uptime SLAs — Digital banks without branch fallbacks have zero tolerance for downtime

- Open API ecosystems — Proactive participation in open banking frameworks accelerates ecosystem value creation

- Data as a strategic asset — Customer transaction data, processed ethically and within privacy regulations, powers personalization, credit decisions, and fraud detection

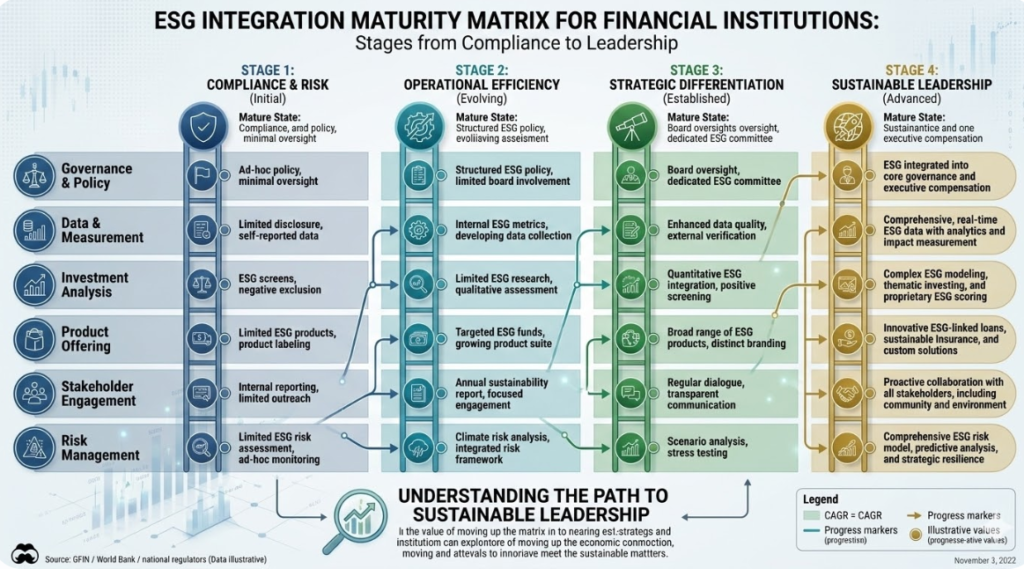

ESG Integration — Sustainable Finance Goes Mainstream

Environmental, Social, and Governance (ESG) principles are no longer peripheral to banking strategy — they are central to capital allocation, regulatory compliance, and institutional reputation.

Key ESG developments reshaping global banking:

Environmental:

- The Task Force on Climate-Related Financial Disclosures (TCFD) framework, now mandatory in the UK and referenced globally, requires banks to disclose climate-related risks in their portfolios

- Green bond issuance has surpassed $500 billion annually (Climate Bonds Initiative, 2023), with banks acting as both issuers and underwriters

- Sustainable lending — tiered pricing for ESG-compliant borrowers incentivizes corporate decarbonization

Social:

- Financial inclusion mandates — Regulators in the EU, India, and Kenya, among others, require institutions to demonstrate progress toward serving underbanked populations

- Fair lending frameworks — AI-driven credit decisions must be audited for discriminatory patterns (a growing area of scrutiny by the FCA, CFPB, and equivalent bodies)

Governance:

- Board-level ESG accountability — Major asset managers including BlackRock have embedded ESG governance expectations into their investment stewardship frameworks

- Executive remuneration linked to ESG KPIs — A growing standard among globally significant financial institutions

💬 Expert Perspective: “ESG is not a marketing checkbox. For financial institutions, it is a risk framework — physical climate risk, transition risk, and social risk are all balance sheet events.” — Consistent view expressed across NGFS (Network for Greening the Financial System) member central banks

ESG Integration Maturity Matrix for Financial Institutions — Stages from Compliance to Leadership

Technology as the Spine of Banking 4.0

Artificial Intelligence in Financial Services

AI is not a future ambition in Banking 4.0 — it is a present reality deployed across:

- Credit underwriting — Alternative data models (telco data, e-commerce behavior, psychometric scoring) extend credit to thin-file customers excluded by traditional bureaus

- Fraud detection — Real-time graph neural networks analyzing transaction networks catch fraud patterns invisible to rule-based systems

- Customer service — Large language model (LLM)-powered virtual assistants handling complex financial queries at scale

- Regulatory reporting — NLP-based tools automating the extraction of regulatory data from unstructured documents

- Portfolio management — BlackRock’s Aladdin platform, managing risk analytics for over $21 trillion in assets, is the defining example of AI-at-scale in institutional finance

Governance of AI in Banking: The Bank for International Settlements and the Financial Stability Board (FSB) have both issued guidance on AI governance in financial services, emphasizing:

- Explainability of AI decisions (particularly in credit)

- Human oversight in high-stakes decisions

- Bias auditing and fairness testing

- Model risk management frameworks

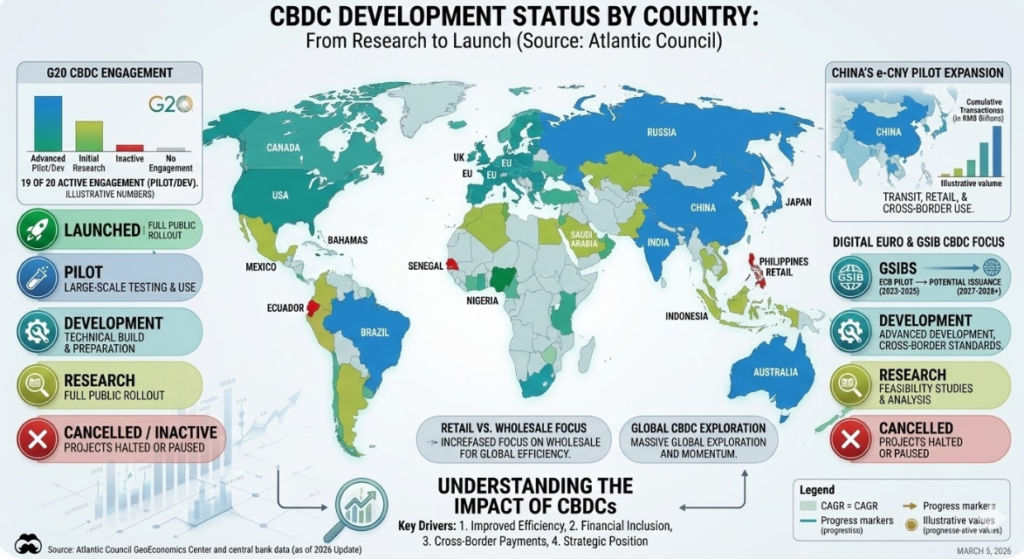

Central Bank Digital Currencies (CBDCs) — The Sovereign Digital Frontier

Over 130 countries representing 98% of global GDP are now exploring or piloting Central Bank Digital Currencies (CBDCs), according to the Atlantic Council CBDC Tracker (2024).

CBDCs represent the most significant restructuring of monetary infrastructure since the Bretton Woods agreement. Key global developments:

- The European Central Bank (ECB) is in the investigation phase of a Digital Euro, designed to complement cash rather than replace it

- The Bank for International Settlements (BIS) is facilitating cross-border CBDC experiments (mBridge, Project Dunbar) to test interoperable wholesale CBDC systems

- Retail CBDC pilots are live or completed in the Bahamas (Sand Dollar), Nigeria (eNaira), Jamaica (JAM-DEX), and several others

CBDCs have profound implications for commercial banking: if retail CBDCs enable direct citizen accounts at central banks, the deposit-gathering function of commercial banks could be materially disrupted — a dynamic regulators are actively managing through design choices like holding limits and non-interest bearing balances.

CBDC Development Status by Country — Research / Pilot / Launched / Cancelled, Source: Atlantic Council

Blockchain and Distributed Ledger Technology (DLT) in Institutional Finance

While retail crypto markets have attracted mainstream attention, the more transformative application of blockchain in Banking 4.0 is institutional DLT adoption:

- Settlement finality — The Depository Trust & Clearing Corporation (DTCC) and European equivalents are exploring DLT to compress securities settlement from T+2 to T+0

- Trade finance digitization — The ICC (International Chamber of Commerce) has championed DLT-based digital trade documents, reducing fraud and processing time in global supply chains

- Tokenization of real-world assets (RWAs) — BlackRock, Franklin Templeton, and other global asset managers have launched tokenized fund products on public blockchains, signaling institutional validation of the technology

Challenges and Risk Management in the Banking 4.0 Era

Cybersecurity — The Existential Risk

The digitization of banking creates an exponentially larger attack surface. The IMF’s 2024 Global Financial Stability Report devoted a full chapter to cyber risk, estimating that average annual financial sector cyber losses have more than doubled since 2017.

Best practice cybersecurity frameworks for Banking 4.0:

- NIST Cybersecurity Framework — globally adopted baseline for financial sector cyber risk management

- TIBER-EU (Threat Intelligence-Based Ethical Red Teaming) — the ECB’s framework for advanced penetration testing of financial institutions

- ISO/IEC 27001 — international standard for information security management systems

- Zero Trust Architecture — the principle of “never trust, always verify” replacing perimeter-based security models

Concentration Risk in Cloud and Third-Party Dependencies

Banking 4.0’s cloud-native infrastructure creates a new systemic risk: concentration in a small number of hyperscaler providers. The FSB’s 2023 Report on Financial Stability Implications of Cloud Outsourcing found that a critical outage at one of the top three cloud providers could simultaneously affect thousands of financial institutions globally.

Regulators are responding with:

- Operational Resilience frameworks (Bank of England, European Banking Authority)

- Digital Operational Resilience Act (DORA) in the EU — mandatory from January 2025

- Exit strategy requirements for cloud and third-party service agreements

Financial Crime in a Digital-First World

The speed advantage of Banking 4.0 is a double-edged sword. Real-time payments enable real-time fraud — particularly authorized push payment (APP) fraud, which has surged globally as faster payment infrastructure has expanded.

Best practice responses include:

- Confirmation of Payee (CoP) — identity verification before payment execution

- AI-driven transaction monitoring with behavioral biometrics

- Industry-wide fraud data sharing consortia (Cifas in the UK, equivalent bodies globally)

- Regulatory mandates for reimbursement of fraud victims (UK PSR 2024 regulations as a leading precedent)

Financial Inclusion — Banking 4.0’s Greatest Mandate

The most compelling argument for Banking 4.0 is its capacity to serve the 1.4 billion unbanked adults globally. Digital financial infrastructure makes the economics of serving low-income, remote, and informal economy customers viable for the first time.

Key enablers of digital financial inclusion:

- Mobile penetration — Ubiquitous smartphones provide the distribution channel

- Biometric identity — India’s Aadhaar system demonstrates how national digital identity infrastructure unlocks financial access for hundreds of millions

- Alternative credit scoring — Satellite data, mobile usage patterns, and psychometric testing enable credit decisions for customers with no formal credit history

- Agent banking networks — Human touchpoints in low-connectivity areas bridging digital and physical

- Simplified regulatory frameworks — Tiered KYC for low-value accounts reduces onboarding friction without increasing financial crime risk

The World Bank’s Universal Financial Access (UFA) 2020 goal, though not fully achieved, catalyzed $33 billion in commitments and significant regulatory reform globally. UFA 2030 targets continue this work, with digital rails at the center of the strategy.

💬 Expert Perspective: “Financial inclusion is not charity. It is the single largest untapped market in global banking — and Banking 4.0 has finally made the unit economics work.” — Consistent perspective across IFC (International Finance Corporation) FinTech investment reports

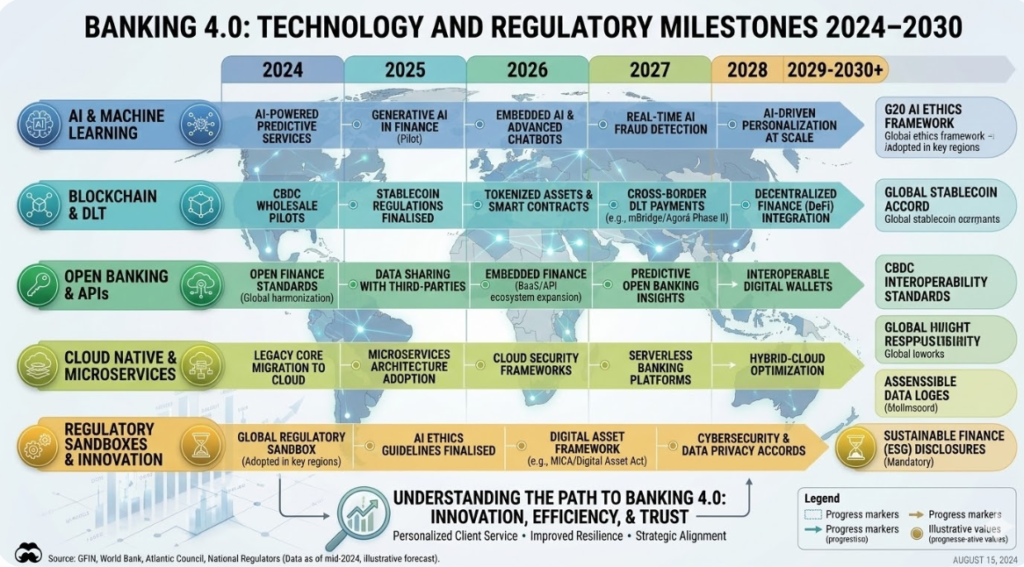

The Future of Banking 4.0 — Emerging Trends

The following trends will define the next decade of global financial evolution:

1. Generative AI and Hyper-Personalization

LLM-powered financial advisors will democratize wealth management advice currently accessible only to high-net-worth individuals. Regulatory frameworks for AI-generated financial advice are being developed across the EU, UK, and Singapore.

2. Open Finance and the Data Economy

Beyond Open Banking (payment accounts), Open Finance extends API-based data sharing to mortgages, pensions, insurance, and investments — creating truly comprehensive financial data portability. Brazil’s Open Finance implementation is the most comprehensive globally and serves as a model for other markets.

3. Quantum Computing and Cryptographic Risk

Quantum computing will eventually break current encryption standards protecting financial data. The National Institute of Standards and Technology (NIST) finalized its first post-quantum cryptographic standards in 2024 — financial institutions must begin migration planning now.

4. The Platformification of Banking

The long-term trajectory points to a small number of global financial platforms — potentially merging banking, investment, insurance, and commerce — serving billions of customers, much as social media platforms consolidated communication. Regulatory responses to prevent monopolistic concentration will be among the defining policy debates of the decade.

5. Sustainable Finance as Core Business

Net-zero commitments from major financial institutions, combined with mandatory climate risk disclosure (TCFD, ISSB standards), will make sustainable finance the default — not the exception — for capital allocation decisions by 2030.

Banking 4.0 Technology and Regulatory Milestones 2024–2030

Conclusion: Navigating the Banking 4.0 Imperative

Banking 4.0 is not a destination — it is a continuous transformation. The transition from brick-and-mortar to digital-first institutions, from proprietary products to BaaS ecosystems, and from transactional relationships to data-driven financial partnerships represents the most significant structural change in financial services since the invention of the joint-stock company.

Key takeaways for financial professionals and institutions:

- Embrace platform thinking — The future competitive advantage lies not in holding a banking license alone, but in orchestrating financial ecosystems

- Invest in regulatory intelligence — In a multi-jurisdictional world, regulatory navigation is a core competency, not a compliance afterthought

- Lead on ESG — Institutions that embed sustainability into their core strategy, not just their reporting, will outperform over the long term

- Prioritize cybersecurity and operational resilience — The reputational and regulatory cost of a major cyber incident in a digital-first institution is existential

- Champion financial inclusion — Both the moral and commercial case for serving the underbanked are stronger than ever; Banking 4.0 makes it possible

The institutions that will lead the next decade are those that understand technology not as a cost center or a disruption threat, but as the foundational infrastructure of a more inclusive, efficient, and resilient global financial system.

“The bank of the future may not look like a bank at all — but it will still need to earn trust, manage risk, and serve human needs. Those fundamentals are eternal.” — Synthesized from FSB, BIS, and IMF forward-looking financial stability assessments

Frequently Asked Questions (FAQ)

Q1: What is the difference between a Neo-bank and a traditional digital bank? A Neo-bank (or challenger bank) operates entirely without physical branches and is typically built on cloud-native, API-first architecture from inception. Traditional banks with digital channels have grafted digital interfaces onto legacy core banking systems — a fundamental architectural difference that affects speed of innovation, cost structure, and customer experience. Some Neo-banks hold their own banking licenses; others operate under BaaS arrangements with licensed partner banks.

Q2: How do Banking-as-a-Service (BaaS) models handle regulatory compliance? In a BaaS model, regulatory accountability is shared across the stack. The licensed bank (the regulated entity) retains ultimate responsibility for compliance with banking regulations, capital requirements, and AML/KYC obligations. BaaS platforms typically provide compliance infrastructure as part of their service. Non-bank companies building on BaaS must comply with applicable consumer protection, data privacy, and (where applicable) e-money regulations in each jurisdiction. Regulators globally are clarifying accountability frameworks — the FCA, ECB, and MAS have each issued guidance on responsibility allocation in BaaS arrangements.

Q3: What international standards should financial institutions prioritize for Banking 4.0 readiness? Key international standards and frameworks for Banking 4.0 readiness include:

- Basel III/IV — Capital adequacy and liquidity (BCBS)

- FATF Recommendations — AML/CFT compliance

- TCFD Framework — Climate risk disclosure

- ISO/IEC 27001 — Information security management

- NIST Cybersecurity Framework — Cyber risk management

- PCI DSS — Payment card data security

- GDPR / Privacy-by-Design principles — Data protection

- DORA (EU) — Digital operational resilience (from January 2025)

- NIST Post-Quantum Cryptography Standards — Future-proofing cryptographic infrastructure

Suggested External Resources and Links

- Basel Committee on Banking Supervision Publications — Capital standards, consultative papers

- IMF Financial Sector Assessment Program — Country-level financial stability analysis

- World Bank Global Findex Database — Financial inclusion data

- FSB Crypto-Asset and DeFi Reports — Regulatory frameworks for digital assets

- FATF Guidance on Virtual Assets — AML standards for digital finance

- BIS Innovation Hub — Central bank experimentation with technology

- TCFD Recommendations — Climate-related financial disclosure framework

- Atlantic Council CBDC Tracker — Global CBDC development monitor

This article reflects global banking and financial governance developments as of 2026. Financial regulations and market structures evolve rapidly — readers are encouraged to consult primary regulatory sources and qualified financial advisors for jurisdiction-specific guidance.