“Growth is never by mere chance; it is the result of forces working together.” — James Cash Penney, adapted for the modern banking context.

In 2023, global banking assets surpassed $183 trillion, according to the Bank for International Settlements (BIS) — a figure that underscores the extraordinary scale and systemic importance of the financial sector in the world economy. Yet, scaling a bank sustainably is arguably one of the most complex strategic challenges in modern commerce. It demands the simultaneous mastery of regulatory compliance, risk architecture, digital transformation, talent management, and capital optimization — all while navigating an increasingly volatile geopolitical and macroeconomic environment.

Whether you are a C-suite executive at a Tier-1 institution, a strategy analyst at a regional bank, or a governance professional working within international finance frameworks, the question is the same: How do high-performing financial institutions grow — sustainably, responsibly, and at scale?

This post unpacks the core strategies, global case studies, and best practices that define excellence in bank growth today.

Table of Contents

- Defining the Foundation: Key Concepts in Bank Growth

- The Global Growth Imperative: Why Scale Matters Now

- Organic vs. Inorganic Growth: Choosing the Right Path

- Mergers, Acquisitions, and Cross-Border Consolidation

- Digital Transformation as a Growth Engine

- Regulatory Compliance and Governance Frameworks

- ESG Integration: Sustainability as a Strategic Advantage

- Lessons from Tier-1 Banks Across Regions

- Building Operational Excellence at Scale

- The Road Ahead: Emerging Trends Reshaping Bank Growth

- Conclusion and Actionable Insights

- FAQ

1. Defining the Foundation: Key Concepts in Bank Growth {#definitions}

Before examining strategies, it is essential to establish a shared vocabulary. The following terms form the conceptual scaffolding of sustainable bank growth:

Financial Intermediation

Financial intermediation refers to the process by which banks channel funds from savers (surplus units) to borrowers (deficit units). It is the fundamental economic role of banking — transforming idle capital into productive investment. At scale, the efficiency of this function is a core measure of institutional health, as measured by metrics such as the Net Interest Margin (NIM) and Return on Assets (ROA).

Maturity Transformation

Maturity transformation is the practice of borrowing short-term (e.g., customer deposits) and lending long-term (e.g., mortgages, infrastructure loans). It is inherently profitable — but also the primary source of liquidity risk in banking. The Basel Committee on Banking Supervision’s Liquidity Coverage Ratio (LCR) and Net Stable Funding Ratio (NSFR) exist precisely to manage this risk at a systemic level.

Fiduciary Responsibility

A fiduciary is an entity that acts in the best interest of another party. For banks — particularly those managing wealth, pension funds, or investment portfolios — fiduciary responsibility is both a legal obligation and a reputational cornerstone. Violations of fiduciary duty are among the most cited causes of regulatory sanctions globally.

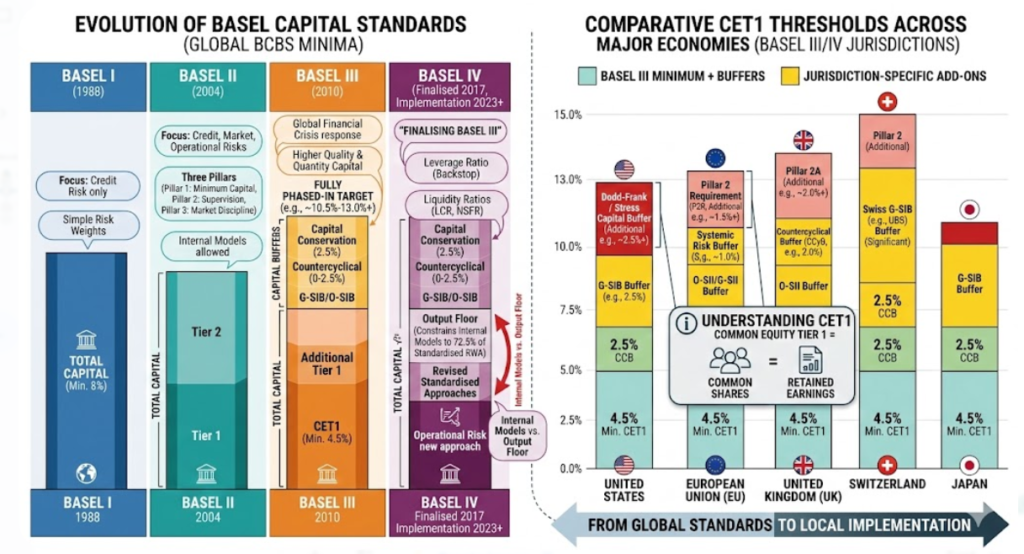

Capital Adequacy

Under Basel III and the forthcoming Basel IV (Basel III finalisation) reforms, banks are required to maintain minimum capital ratios — including the Common Equity Tier 1 (CET1) ratio — to absorb unexpected losses. Capital adequacy is the foundation of both growth and resilience. It is the mechanism by which banks demonstrate to regulators, investors, and markets that they can scale without becoming systemically fragile.

2. The Global Growth Imperative: Why Scale Matters Now {#global-context}

The post-pandemic global economy has reconfigured the competitive landscape of banking in profound ways. Several converging forces make the pursuit of scale not merely desirable but strategically necessary:

- Margin compression: Ultra-low interest rate environments — still unwinding in many markets — eroded traditional lending spreads, compelling banks to seek volume and diversification.

- Technology disruption: FinTech entrants and Big Tech platforms (operating under lighter regulatory regimes) have captured significant market share in payments, lending, and wealth management.

- Regulatory burden: Compliance costs have risen dramatically. According to a McKinsey Global Banking Report, regulatory compliance now accounts for 15–20% of total operating costs for large global banks — a burden that scales more favorably for larger institutions.

- Geopolitical fragmentation: From trade sanctions to currency volatility, global banks must build resilient, geographically diversified portfolios.

The IMF’s Global Financial Stability Report consistently highlights that banks with stronger capital buffers, diversified revenue streams, and advanced risk management frameworks demonstrate greater resilience during systemic shocks — and are better positioned to grow through disruption.

“The banks that emerged strongest from the 2008 financial crisis — and the COVID-19 shock of 2020 — were those with the deepest capital reserves and the most diversified business models.” — Adapted from IMF Global Financial Stability Report, 2023

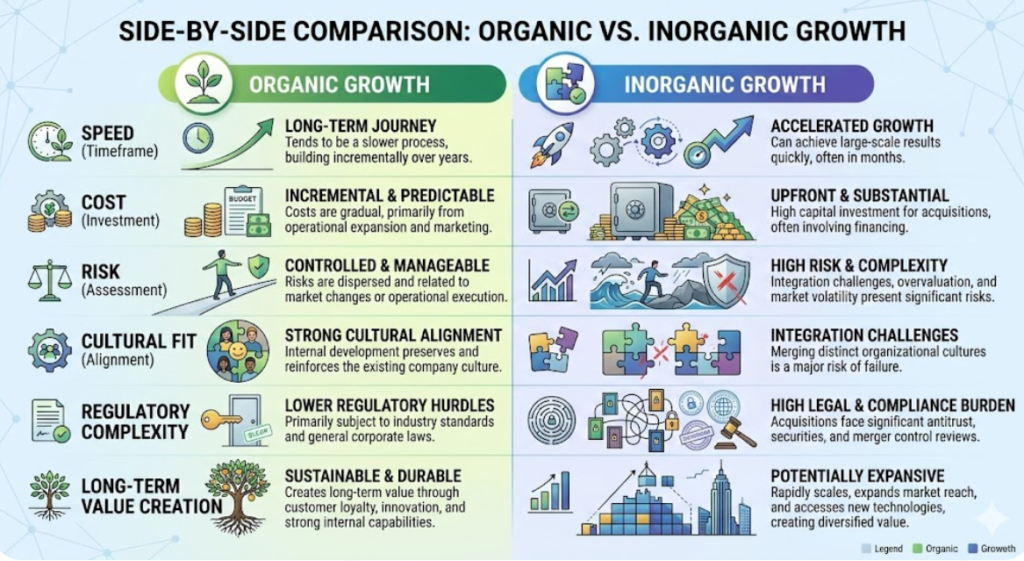

3. Organic vs. Inorganic Growth: Choosing the Right Path {#organic-vs-inorganic}

The strategic choice between organic and inorganic growth is not binary — it is a portfolio decision. Leading institutions typically pursue both simultaneously, calibrated to market conditions, capital availability, and competitive positioning.

Organic Growth Strategies

Organic growth refers to expanding a bank’s revenue base, customer portfolio, and market presence through internal capabilities — without acquisitions or mergers. Key levers include:

- Customer acquisition and retention: Deepening relationships through cross-selling, personalization, and superior digital experience.

- Geographic market entry: Opening new branches, representative offices, or digital-first operations in under-penetrated markets — particularly in Sub-Saharan Africa, Southeast Asia, and Latin America, where financial inclusion gaps remain significant.

- Product innovation: Launching new financial products — green bonds, embedded finance, Buy Now Pay Later (BNPL) platforms, or digital wallets — to capture new revenue streams.

- Talent and capability development: Building proprietary expertise in areas such as data analytics, cybersecurity, and ESG advisory.

Key Metrics for Organic Growth:

- Loan book growth rate

- Deposit market share gains

- Customer Lifetime Value (CLV)

- Cost-to-Income Ratio (CIR) improvement

Inorganic Growth Strategies

Inorganic growth — through mergers, acquisitions, strategic partnerships, or joint ventures — offers faster access to scale, talent, technology, and new markets. However, it carries execution risk and requires robust post-merger integration (PMI) capabilities.

4. Mergers, Acquisitions, and Cross-Border Consolidation {#mergers-acquisitions}

Global banking M&A has historically followed cyclical patterns — peaking during periods of regulatory liberalization or economic stress — but has taken on new dimensions in the current environment.

Strategic Rationale for Bank M&A

The primary motivations for consolidation in global banking include:

- Scale economies: Spreading fixed costs (technology platforms, compliance infrastructure, branch networks) across a larger asset base.

- Geographic diversification: Reducing concentration risk by entering new markets.

- Capability acquisition: Accessing FinTech capabilities, AI platforms, or specialized expertise that would take years to build organically.

- Market power: Gaining pricing power in concentrated lending or deposit markets.

Cross-Border M&A: Complexity and Opportunity

Cross-border acquisitions in banking are among the most complex corporate transactions globally. They require navigation of:

- Multi-jurisdictional regulatory approvals: From the European Central Bank (ECB) for eurozone banks, to the Federal Reserve and OCC in the United States, to the Monetary Authority of Singapore (MAS) in Asia.

- Currency and capital repatriation risks

- Cultural integration challenges, particularly in high-context banking cultures across Asia and the Middle East

- Data sovereignty and cross-border data transfer restrictions

The Financial Stability Board (FSB) and Basel Committee have issued guidance on the supervision of cross-border banking groups, emphasizing the need for home-host supervisor coordination and transparent Recovery and Resolution Plans (RRPs).

Case Study Framework: A Hypothetical Tier-1 Cross-Regional Merger

Consider a hypothetical European universal bank acquiring a Southeast Asian digital bank. The integration playbook would typically involve:

- Pre-deal due diligence: Regulatory capital assessment, asset quality review (AQR), technology architecture audit, and ESG risk screening.

- Regulatory engagement: Filing with all relevant supervisory authorities; submitting a Combined Group Recovery Plan.

- Integration Management Office (IMO): Establishing a dedicated governance body with representation from both entities.

- Technology integration: Rationalizing core banking platforms (often the most time-consuming element, typically 3–5 years).

- Culture and talent integration: Retention programs, unified leadership frameworks, and values alignment.

“The most common cause of M&A failure in banking is not financial miscalculation — it is cultural misalignment and underestimation of technology integration complexity.” — Global Banking M&A Outlook, Deloitte, 2023

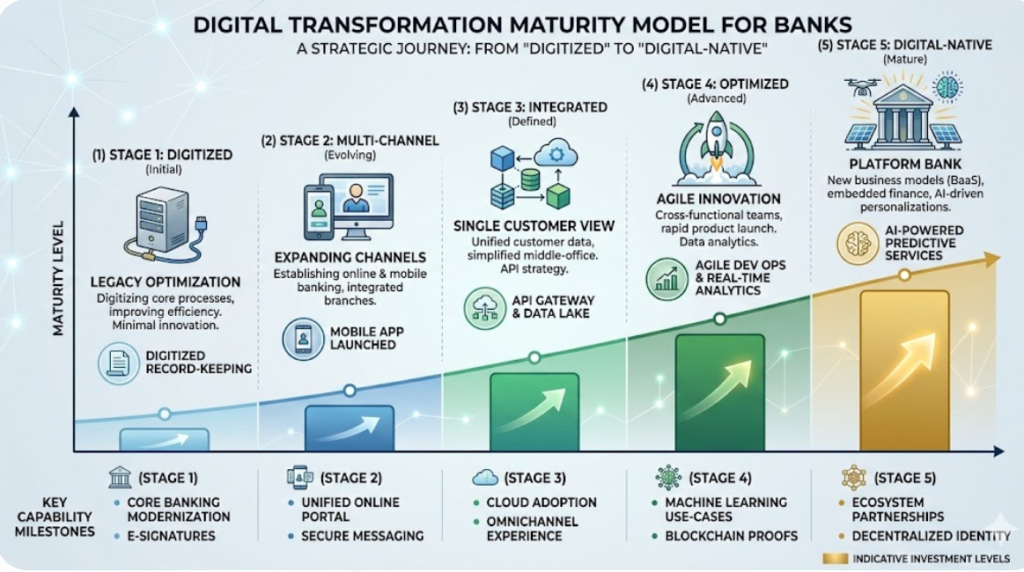

5. Digital Transformation as a Growth Engine {#digital-transformation}

Perhaps no single force is reshaping the trajectory of bank growth more profoundly than digital transformation. This encompasses not merely the digitization of existing processes but the fundamental reimagining of banking business models.

The Four Pillars of Digital Transformation in Banking

Pillar 1: Core Banking Modernization

Legacy core banking systems — some dating back 30–40 years — represent the single greatest constraint on digital agility for incumbent institutions. Migration to cloud-native, API-first core banking platforms (such as those offered by Temenos, Thought Machine, or Mambu) is now a strategic priority for growth-oriented banks globally.

Pillar 2: Data and Artificial Intelligence

The application of machine learning and AI across the banking value chain is generating measurable competitive advantage:

- Credit decisioning: AI-driven models assess creditworthiness using alternative data (transaction history, behavioral patterns), expanding financial inclusion to underserved populations.

- Fraud detection: Real-time anomaly detection reduces false positives while improving security.

- Personalization: Hyper-personalized financial advice and product recommendations at scale.

- Risk management: Predictive models for Expected Credit Loss (ECL) under IFRS 9 and stress testing under regulatory frameworks.

Pillar 3: Open Banking and Ecosystem Strategy

Regulatory mandates — including PSD2 in Europe and equivalent frameworks in the UK, Australia, and Singapore — have accelerated the shift toward open banking, where banks expose APIs to third-party providers. Forward-thinking institutions are leveraging this to:

- Build marketplace banking ecosystems

- Offer embedded finance services within non-financial platforms

- Generate new fee-based revenue streams beyond traditional intermediation

Pillar 4: FinTech Partnerships and Venture Investment

Rather than viewing FinTechs purely as disruptors, leading global banks are partnering with — and investing in — them strategically. M-Pesa, the mobile money platform pioneered in East Africa, is a landmark case study in how mobile-first financial infrastructure can achieve extraordinary penetration rates (reaching over 50 million active users across multiple markets) by meeting customers where they are — on their mobile phones, without requiring traditional banking infrastructure.

6. Regulatory Compliance and Governance Frameworks {#regulatory-compliance}

Sustainable growth is inseparable from regulatory integrity. The global regulatory architecture for banking is multi-layered, complex, and continuously evolving.

The Basel Framework: The Cornerstone of Global Banking Regulation

The Basel Committee on Banking Supervision (BCBS), housed at the BIS in Basel, Switzerland, develops global standards for the regulation, supervision, and risk management of banks. The key pillars of the current framework include:

- Pillar 1 – Minimum Capital Requirements: Covering credit risk, market risk, and operational risk.

- Pillar 2 – Supervisory Review Process: Requiring banks to assess their own capital adequacy relative to their risk profile (ICAAP/ILAAP).

- Pillar 3 – Market Discipline: Mandating public disclosure to enable market participants to assess a bank’s risk profile.

[🔗 External Link Suggestion: Basel Committee Publications — https://www.bis.org/bcbs/publications.htm]

Anti-Money Laundering (AML) and Financial Crime Compliance

The Financial Action Task Force (FATF) sets global standards for AML and counter-terrorist financing (CTF). Compliance failures in this domain carry existential consequences — both reputational and financial. Global banks have invested billions in Know Your Customer (KYC) infrastructure, transaction monitoring systems, and Suspicious Activity Reporting (SAR) frameworks.

Corporate Governance Best Practices

The G20/OECD Principles of Corporate Governance provide a globally recognized framework for board composition, executive remuneration, shareholder rights, and stakeholder transparency. For banks specifically, the BIS Senior Supervisors Group has published guidance on the governance of systemically important financial institutions (SIFIs).

Key governance imperatives for scaling banks include:

- Board independence and diversity: Ensuring directors are free from conflicts of interest and bring diverse expertise.

- Risk appetite framework (RAF): Clearly articulating the types and quantum of risk the institution is willing to accept in pursuit of growth.

- Three-lines-of-defence model: Business functions (1st line), Risk and Compliance (2nd line), and Internal Audit (3rd line).

- Remuneration alignment: Structuring executive incentives to reward sustainable long-term value creation, not short-term risk-taking (per FSB Principles for Sound Compensation Practices).

7. ESG Integration: Sustainability as a Strategic Advantage {#esg-integration}

Environmental, Social, and Governance (ESG) considerations have moved from peripheral corporate social responsibility to core strategic imperatives for global financial institutions. This shift is driven by regulatory pressure, investor expectations, and the mounting evidence that ESG-aligned institutions outperform on risk-adjusted returns over the long term.

Environmental Dimension: Financing the Green Transition

- Banks are increasingly required to disclose climate-related financial risks under frameworks such as the Task Force on Climate-related Financial Disclosures (TCFD) — now being superseded by the IFRS S2 Climate-related Disclosures standard globally.

- Green bonds, sustainability-linked loans, and transition finance instruments are fast-growing product categories, supported by the International Capital Market Association (ICMA) Green Bond Principles.

- The Network for Greening the Financial System (NGFS), a coalition of over 130 central banks, is integrating climate risk into prudential supervision.

Social Dimension: Financial Inclusion and Community Impact

- The World Bank’s Universal Financial Access Initiative highlights that 1.4 billion adults globally remain unbanked. Banks that expand access — through digital channels, agent banking, or microfinance — are not merely fulfilling social obligations; they are opening vast new market opportunities.

- Diversity, Equity, and Inclusion (DEI) within the institution itself is increasingly measured and reported, with investor pressure growing through initiatives such as the 30% Club and the UN Principles for Responsible Investment (PRI).

Governance Dimension: Accountability and Transparency

- Robust ESG governance includes dedicated Board-level ESG committees, transparent sustainability reporting (aligned with GRI Standards, SASB, or CSRD in Europe), and third-party assurance of non-financial disclosures.

“ESG is no longer a CSR bolt-on — it is embedded in how we assess credit risk, structure capital allocation, and evaluate the sustainability of our own business model.” — Representative quote reflective of leading global bank ESG strategy frameworks

[🔗 External Link Suggestion: TCFD Recommendations — https://www.fsb-tcfd.org/publications/]

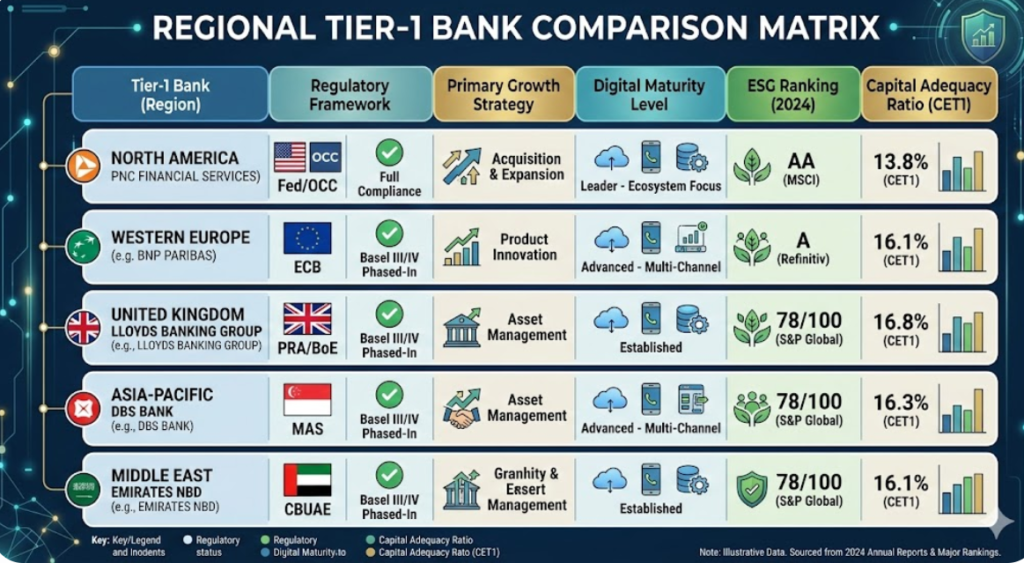

8. Lessons from Tier-1 Banks Across Regions {#tier1-lessons}

European Banks: Efficiency, Regulation, and the Digital Race

European Tier-1 institutions operate within the most stringent regulatory environment globally — governed by the ECB’s Single Supervisory Mechanism (SSM) and subject to SREP (Supervisory Review and Evaluation Process) assessments annually. The defining strategic challenge for European banks has been profitability restoration following years of near-zero interest rates. The strategic response has included:

- Aggressive cost transformation programs (workforce restructuring, branch rationalization, IT modernization)

- Pan-European consolidation to achieve scale

- Wealth management and fee income diversification

- Investment in digital-only subsidiary banks to compete with neobanks

Asian Banks: Growth Markets, Technology, and Financial Inclusion

Banks headquartered in markets such as Singapore, Hong Kong, and Japan operate as regional hubs for the dynamic Asia-Pacific growth corridor. Key distinguishing characteristics include:

- Deep integration with trade finance flows across the Belt and Road and ASEAN supply chains

- Leadership in digital banking licensing frameworks (Singapore’s MAS digital bank licenses being a globally cited model)

- Large-scale investment in AI-driven retail banking — with mobile banking penetration rates in some Asian markets exceeding 80%

Americas-Based Banks: Scale, Capital Markets, and Innovation

The largest banks in the Americas — operating under the oversight of the Federal Reserve, OCC, FDIC, and the SEC — are distinguished by:

- Unparalleled capital markets capabilities (investment banking, debt underwriting, derivatives)

- Global transaction banking dominance

- Massive investment in proprietary technology and data analytics

- Sophisticated stress testing regimes (e.g., the Federal Reserve’s DFAST and CCAR programs)

9. Building Operational Excellence at Scale {#operational-excellence}

Growth without operational excellence is a recipe for systemic fragility. The most admired global institutions combine aggressive growth ambitions with relentless attention to operational discipline.

Cost Efficiency: The Cost-to-Income Ratio Imperative

The Cost-to-Income Ratio (CIR) — operating costs as a percentage of operating income — is the primary measure of operational efficiency in banking. Best-in-class global banks maintain CIRs in the 40–50% range. Achieving this at scale requires:

- Process automation: Robotic Process Automation (RPA) and intelligent document processing for high-volume, low-complexity tasks (loan processing, KYC onboarding, reconciliation).

- Shared services and offshoring: Centralizing support functions across a global operational model.

- Zero-based budgeting (ZBB): Regularly challenging all cost lines from first principles, rather than incrementally adjusting prior-year budgets.

Resilience and Business Continuity

Operational resilience has become a regulatory priority globally, with the Bank of England’s Operational Resilience Policy and DORA (Digital Operational Resilience Act) in the EU setting new standards. Banks must now:

- Map important business services and their dependencies

- Set impact tolerances for disruption

- Test resilience through scenario analysis and stress simulation

- Ensure third-party and outsourcing risk is managed end-to-end

Talent Strategy: The Human Foundation of Scale

Growth strategies ultimately depend on people. Global banks compete intensely for talent in:

- Technology and engineering (cloud architects, AI/ML engineers, cybersecurity specialists)

- Risk and compliance (regulatory affairs, financial crime, model validation)

- ESG and sustainability advisory

- Data science and analytics

The most progressive institutions are building internal academies, partnering with universities, and deploying AI-powered talent matching to close skills gaps at pace.

10. The Road Ahead: Emerging Trends Reshaping Bank Growth {#emerging-trends}

The next decade of banking will be defined by several transformative forces. Institutions that anticipate and adapt to these trends will be the architects of the next era of banking excellence.

Artificial Intelligence and Generative AI

Generative AI is beginning to transform banking across functions: from automating regulatory reporting and drafting credit memos, to powering next-generation customer service interfaces. The BIS Innovation Hub is actively researching AI governance frameworks for financial institutions. The strategic imperative is not adoption per se, but responsible adoption — with robust model risk management, bias detection, and explainability frameworks.

Central Bank Digital Currencies (CBDCs)

Over 130 countries are exploring or piloting CBDCs, according to the Atlantic Council’s CBDC Tracker. From the Digital Euro project to the e-CNY in China and the Digital Rupee in India, CBDCs will fundamentally reshape payment infrastructures, monetary policy transmission, and potentially the deposit-taking model of commercial banks. Banks that proactively engage with CBDC design and interoperability will be better positioned to maintain their intermediation role.

[🔗 External Link Suggestion: IMF CBDC Virtual Handbook — https://www.imf.org/en/Topics/fintech/cbdc-virtual-handbook]

Embedded Finance and Banking-as-a-Service (BaaS)

The disintermediation of the customer relationship — as non-banks embed financial services within their own platforms — challenges banks to redefine their value proposition. The strategic response is Banking-as-a-Service (BaaS): offering licensed banking infrastructure (accounts, payments, credit) as an API-driven service to third-party platforms. This model allows banks to generate fee income at scale without the cost of direct customer acquisition.

Quantum Computing and Cybersecurity

Quantum computing poses both an opportunity (dramatically enhanced risk modelling, fraud detection) and an existential threat (breaking current cryptographic standards). The BIS and NIST are actively working on post-quantum cryptography standards. Forward-looking banks are beginning crypto-agility programs to ensure their security architectures can transition.

Sustainable Finance and Transition Finance

The global transition to a net-zero economy will require an estimated $4–5 trillion per year in green investment through 2030, according to the IEA. Banks with robust transition finance frameworks, credible net-zero commitments (aligned with the Science-Based Targets initiative for Financial Institutions — SBTi), and deep green product capabilities will capture a disproportionate share of this growth opportunity.

11. Conclusion and Actionable Insights {#conclusion}

Scaling excellence in banking is not a single strategy — it is the disciplined orchestration of multiple interdependent capabilities, executed consistently over time. The institutions that achieve sustainable growth are those that:

- Balance ambition with resilience: Growing the balance sheet while maintaining rigorous capital adequacy and liquidity standards.

- Lead with governance: Embedding robust risk management, ethical conduct, and regulatory compliance as foundations — not constraints — of growth.

- Invest in transformation: Committing to genuine digital and operational transformation, not cosmetic digitization.

- Embed sustainability: Treating ESG not as a reporting obligation but as a lens through which all strategic decisions are evaluated.

- Build adaptive capacity: Creating organizations capable of absorbing change — whether technological, regulatory, or macroeconomic — without losing strategic coherence.

Actionable Insights for Financial Professionals

- Audit your growth strategy against both organic and inorganic levers — are you systematically optimizing both?

- Assess your digital maturity honestly. Where are your core banking systems, data architecture, and AI capabilities relative to best-in-class peers?

- Engage proactively with regulators — particularly on emerging frameworks (CBDC, DORA, IFRS S2). Early engagement builds trust and competitive advantage.

- Embed ESG into capital allocation — not just reporting. How are climate risk and social impact factored into your credit and investment decisions?

- Invest in talent for the future: The capabilities you need most — AI/ML, cybersecurity, ESG advisory, digital product management — are in global shortage. Build pipelines now.

“The most dangerous moment for a bank is when it believes its past success is sufficient preparation for the future.” — Adapted from strategic leadership literature on institutional complacency

FAQ {#faq}

Q1: What is the most important regulatory framework for globally active banks?

The Basel III/IV framework developed by the Basel Committee on Banking Supervision is the most universally applicable regulatory standard for globally active banks, covering capital adequacy, liquidity management, and leverage. It is implemented through domestic law in over 100 jurisdictions and forms the foundation of prudential banking regulation worldwide. Complementary frameworks include FATF Standards for financial crime compliance and the FSB’s Key Attributes of Effective Resolution Regimes for systemically important institutions.

Q2: How should banks approach the organic vs. inorganic growth decision?

The optimal growth strategy depends on several factors: the bank’s capital position, its existing capabilities, the competitive intensity of its target markets, and its M&A integration track record. Organic growth offers greater cultural and operational control but is slower. Inorganic growth offers speed to scale but carries integration risk. Most Tier-1 banks employ a portfolio approach — using organic investment in core markets while pursuing selective acquisitions for geographic expansion or capability gaps. The IMF’s financial sector assessments (FSAPs) often provide useful benchmarks for evaluating whether a bank’s growth strategy is consistent with systemic stability objectives.

Q3: How is digital transformation changing the competitive dynamics of global banking?

Digital transformation is reshaping competitive dynamics in two fundamental ways. First, it is lowering barriers to entry: digital-native banks and FinTech platforms can now serve millions of customers with a fraction of the capital and infrastructure required by traditional incumbents. Second, it is raising the expectations bar: customers accustomed to seamless digital experiences in retail and entertainment now demand the same from their financial institutions. Banks that invest deeply in cloud infrastructure, AI, open APIs, and user experience design are widening the gap from those that do not. According to the World Economic Forum, digital leaders in banking achieve operating cost advantages of 30–40% over digital laggards, a gap that compounds over time.

Suggested External Links

- Basel Committee Publications

- IMF Global Financial Stability Report

- FSB Principles for Sound Compensation Practices

- TCFD Recommendations

- World Bank Financial Inclusion Data

- NGFS Climate Scenarios

This article is intended for informational and educational purposes. It reflects analysis based on publicly available global data, institutional publications, and recognized international standards as of 2024–2026. Readers should consult qualified professionals for specific regulatory, legal, or financial advice.