How the Federal Reserve, ECB, and Bank of England Navigate Inflation, Crises, and the Future of Finance

“Central banks are the guardians of monetary stability — but in an era of digital disruption, geopolitical shock, and climate risk, their toolkit must evolve faster than the crises they are designed to contain.” — Senior Economist, Bank for International Settlements (BIS), 2023

In 2022, global inflation surged to levels unseen in four decades, peaking at 9.1% in the United States and exceeding 10% across the Eurozone. Central banks worldwide were thrust into their most consequential battle in a generation — not just against rising prices, but against the erosion of institutional credibility built over decades. The response was swift, coordinated in spirit, yet divergent in execution: interest rate hikes of a scale and speed that rattled bond markets, mortgage holders, and finance ministers alike.

This is the world in which monetary authorities operate — one defined by volatility, interdependence, and the relentless pressure to maintain equilibrium in systems of extraordinary complexity. Understanding how central banks wield their toolkit — from lender of last resort functions to inflation targeting frameworks — is not merely an academic exercise. For financial professionals, institutional investors, policymakers, and informed citizens, it is essential intelligence.

This post provides a comprehensive, globally oriented analysis of the monetary authority’s core instruments, the institutions that deploy them, and the emerging challenges that will define central banking in the decade ahead.

Table of Contents

- What Is a Monetary Authority? Definitions and Scope

- The Core Toolkit: Instruments of Monetary Policy

- Lender of Last Resort: The Ultimate Safety Net

- Inflation Targeting: The Dominant Framework

- Interest Rate Cycles: Mechanics and Market Impact

- Case Study: The Federal Reserve — Power, Independence, and the Dual Mandate

- Case Study: The European Central Bank — Governing the Ungovernable

- Case Study: The Bank of England — Post-Crisis Resilience and the Gilt Shock

- Global Regulatory Standards: Basel III, IMF Oversight, and BIS Coordination

- Digital Transformation: CBDCs, FinTech, and the Future of Monetary Policy

- ESG, Climate Risk, and the Expanding Mandate

- Best Practices for Financial Institutions Navigating Monetary Cycles

- FAQ

- Conclusion: The Road Ahead

1. What Is a Monetary Authority? Definitions and Scope {#definitions}

A monetary authority is an institution — typically a central bank or equivalent regulatory body — empowered to manage a nation’s or economic zone’s money supply, credit conditions, and overall monetary stability. While the term “central bank” is most commonly used, not all monetary authorities take the same form. Currency boards, monetary unions, and multi-mandate financial stability committees all represent variants of this architecture.

Key Terms Defined

- Monetary Policy: The set of tools used by a monetary authority to influence the supply and cost of money in an economy, with the goal of achieving macroeconomic objectives such as price stability, full employment, and sustainable growth.

- Financial Intermediation: The process by which financial institutions (banks, credit unions, investment vehicles) channel funds from savers to borrowers, creating credit and liquidity in the economy. Central banks regulate the environment in which this occurs.

- Maturity Transformation: The practice by which banks borrow short-term (e.g., deposits) and lend long-term (e.g., mortgages). This inherent mismatch is central to banking’s systemic fragility and the rationale for central bank oversight.

- Fiduciary Responsibility: The legal and ethical obligation of financial institutions to act in the best interest of their clients, depositors, and the public — a duty that central banks help enforce through regulatory and supervisory mandates.

- Open Market Operations (OMO): Central bank purchases or sales of government securities in the open market, used to expand or contract the money supply.

- Reserve Requirements: Minimum amounts of liquid assets that commercial banks must hold, as set by the central bank, to ensure solvency and liquidity.

- Quantitative Easing (QE): A non-conventional monetary policy tool where a central bank purchases large-scale financial assets (bonds, mortgage-backed securities) to inject liquidity when interest rates approach zero.

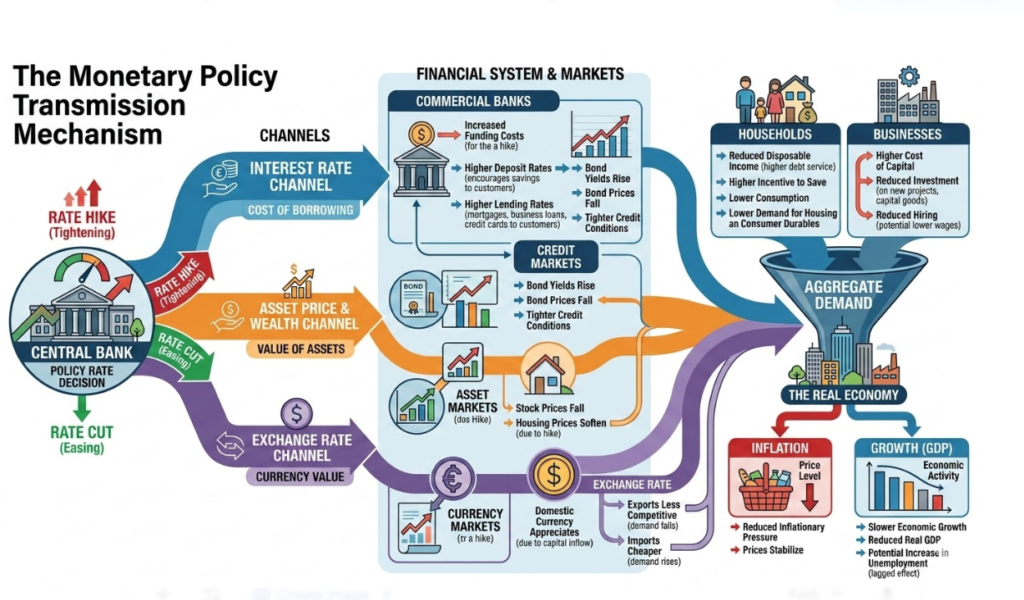

“The Monetary Policy Transmission Mechanism” — showing how central bank rate decisions flow through commercial banks, credit markets, consumer spending, and ultimately inflation and growth

2. The Core Toolkit: Instruments of Monetary Policy {#toolkit}

Central banks do not have a single lever — they have an orchestra of instruments, each suited to different economic conditions and objectives. Understanding this toolkit is fundamental to global finance literacy.

2.1 The Policy Interest Rate

The most powerful and visible tool in the central bank arsenal is the benchmark interest rate — variously known as the federal funds rate, the main refinancing rate, or the base rate depending on the institution. By raising or lowering this rate, a monetary authority effectively sets the “price” of money across the entire economy.

Transmission channels include:

- Bank lending rates: Commercial banks adjust loan and mortgage rates in response

- Exchange rates: Higher rates attract foreign capital, appreciating the currency

- Asset prices: Rate hikes typically depress equity and bond valuations

- Expectations: Forward guidance shapes anticipatory behavior in markets

2.2 Quantitative Easing and Tightening

When conventional interest rate tools are exhausted — particularly at the zero lower bound — central banks deploy Quantitative Easing (QE). Under QE, the central bank creates money electronically and uses it to purchase government bonds or other eligible securities, expanding the monetary base and suppressing long-term yields.

The reverse — Quantitative Tightening (QT) — involves allowing securities to mature without reinvestment or actively selling assets, withdrawing liquidity from the financial system.

| Policy Tool | Expansionary Use | Contractionary Use |

| Policy Rate | Rate Cuts | Rate Hikes |

| QE/QT | Asset Purchases | Asset Sales / Non-Reinvestment |

| Reserve Requirements | Lower Requirements | Raise Requirements |

| Forward Guidance | Dovish Signals | Hawkish Signals |

| Discount Window | Accessible Lending | Restrictive Terms |

2.3 Forward Guidance

Modern central banking recognizes that expectations are as powerful as actions. Forward guidance — public communication about the likely future path of monetary policy — allows authorities to influence financial conditions without necessarily changing rates immediately. The Federal Reserve’s practice of publishing quarterly “dot plots” (projections from individual FOMC members) has become a benchmark for transparency in global banking governance.

2.4 Macroprudential Tools

Beyond traditional monetary instruments, central banks increasingly employ macroprudential tools designed to manage systemic risk across the financial system as a whole:

- Countercyclical Capital Buffers (CCyB): Requiring banks to build capital reserves during booms, releasing them in downturns

- Loan-to-Value (LTV) Caps: Limiting mortgage borrowing relative to property values

- Sectoral Capital Requirements: Applying targeted requirements to overheating sectors (e.g., commercial real estate)

“Macroprudential policy has become the third pillar of the financial stability framework, alongside monetary policy and microprudential supervision.” — IMF Global Financial Stability Report, 2023

3. Lender of Last Resort: The Ultimate Safety Net {#lolr}

Few concepts in global banking are as consequential — or as misunderstood — as the lender of last resort (LOLR) function. First articulated by British economist Walter Bagehot in his 1873 work Lombard Street, the doctrine holds that in times of financial panic, a central bank should lend freely to solvent institutions at a penalty rate against good collateral, thereby halting bank runs and system-wide contagion.

The Bagehot Principle in Practice

The original doctrine contains three components:

- Lend freely — provide unlimited liquidity to prevent panic-driven collapse

- At a penalty rate — deter frivolous use and moral hazard

- Against good collateral — protect the central bank’s balance sheet and taxpayer

In practice, modern LOLR operations have expanded well beyond this classical framework.

Crisis Evolution: From 2008 to 2023

The 2008 Global Financial Crisis redefined the LOLR function. The collapse of Lehman Brothers triggered cascading failures that forced central banks to:

- Establish emergency lending facilities (e.g., the Federal Reserve’s Term Asset-Backed Securities Loan Facility)

- Extend LOLR support to non-bank financial institutions — a major departure from tradition

- Coordinate swap lines between central banks globally, providing dollar liquidity to foreign institutions

The 2023 Banking Turbulence — involving the rapid collapse of Silicon Valley Bank and the emergency absorption of Credit Suisse by UBS — revealed new vulnerabilities: social-media-accelerated bank runs, concentrated depositor bases, and unrealized losses from rapid rate hikes. Authorities responded with expanded deposit guarantees and emergency liquidity facilities that again tested the Bagehot boundaries.

“

Moral Hazard: The Persistent Tension

The LOLR function creates an inherent tension: institutions that expect rescue have reduced incentives to manage risk prudently. This is the classic moral hazard problem in banking. Regulatory responses — including higher capital requirements under Basel III, mandatory stress testing, and living will requirements — are designed to mitigate this dynamic.

4. Inflation Targeting: The Dominant Framework {#inflation-targeting}

Since New Zealand pioneered it in 1990, inflation targeting has become the dominant monetary policy framework adopted by over 40 central banks globally, including the world’s most systemically important institutions.

How Inflation Targeting Works

Under an inflation targeting regime, the central bank:

- Announces a specific inflation target (typically 2% for advanced economies)

- Uses policy interest rates as the primary instrument to achieve it

- Publishes regular forecasts and accountability reports

- Accepts democratic scrutiny for deviations from target

This framework delivers three core benefits: credibility, transparency, and accountability — all of which anchor inflation expectations, which are themselves a powerful determinant of actual inflation outcomes.

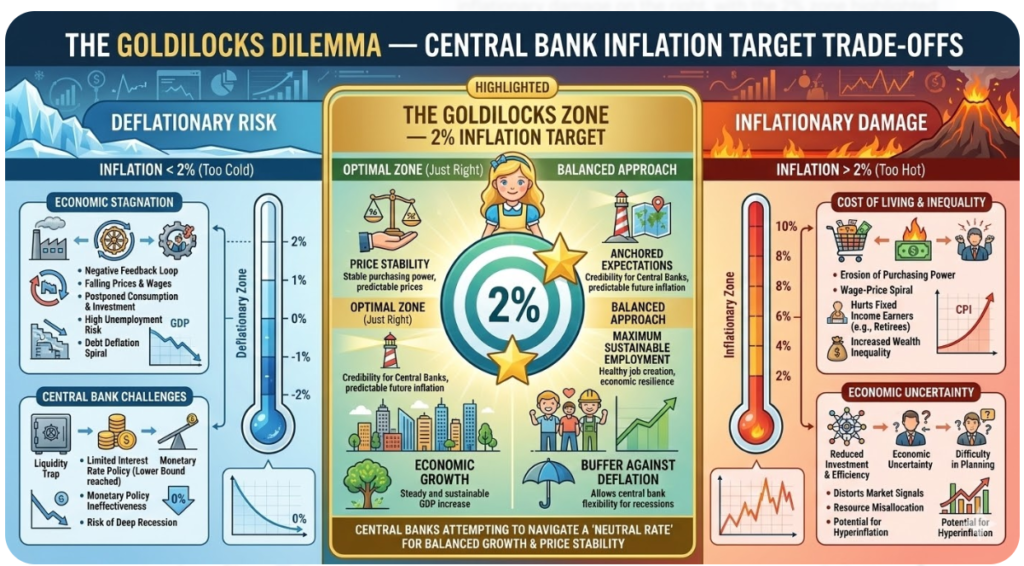

The 2% Target: Why Not Higher or Lower?

The 2% inflation target is not arbitrary. It reflects a careful balance:

- Too low (near zero): Increases the risk of deflation, which paralyzes spending and investment; reduces central bank room to cut rates in recessions

- Too high (5%+): Erodes purchasing power, distorts price signals, and requires more aggressive eventual tightening

- 2% sweet spot: Provides a buffer against deflation, accommodates relative price adjustments, and maintains the real value of money

“The Goldilocks Dilemma — Central Bank Inflation Target Trade-offs” — showing deflationary risk on the left, inflationary damage on the right, with the 2% zone highlighted

Flexible Average Inflation Targeting (FAIT)

In 2020, the Federal Reserve updated its framework to Flexible Average Inflation Targeting (FAIT), permitting inflation to run moderately above 2% for a period following below-target inflation. This represented a significant philosophical shift — acknowledging that symmetric risks (being too low for too long) were as dangerous as overshooting.

5. Interest Rate Cycles: Mechanics and Market Impact {#rate-cycles}

Interest rate cycles are among the most consequential recurring phenomena in global finance. Understanding their mechanics allows financial institutions, corporations, and investors to position themselves across the business cycle.

The Four Phases of an Interest Rate Cycle

Phase 1 — Tightening Cycle (Hiking) Central banks raise rates to cool overheating growth, suppress inflation, or reduce financial imbalances. Credit becomes more expensive; bond prices fall; yield curves typically flatten or invert.

Phase 2 — Restrictive Plateau Rates remain elevated as the monetary authority assesses whether inflation is durably returning to target. This phase can last quarters or years, generating prolonged pressure on leveraged sectors.

Phase 3 — Easing Cycle (Cutting) As inflation falls and growth weakens, central banks begin reducing rates. Bond markets rally; equities — particularly growth stocks — tend to outperform; credit spreads typically compress.

Phase 4 — Accommodative Plateau Rates stabilize at low levels to sustain recovery. This phase may include unconventional measures (QE, negative rates) if conventional cuts are insufficient.

The Yield Curve as a Diagnostic Tool

The yield curve — a graphical representation of interest rates across different maturities — is one of the most closely watched indicators in global finance:

- Normal (upward-sloping): Long-term rates > short-term rates; typical in healthy, growing economies

- Inverted (downward-sloping): Short-term rates > long-term rates; historically a reliable recession predictor

- Flat: Short and long-term rates converge; often signals a turning point in the cycle

The 2022–2023 U.S. yield curve inversion — with the 2-year Treasury briefly yielding over 100 basis points more than the 10-year — triggered widespread recession anticipation and impacted global banking strategies for asset-liability management.

Impact on Financial Institutions

| Rate Environment | Impact on Banks | Impact on Bond Markets | Impact on Equities |

| Rising Rates | NIM expansion short-term; credit risk rises | Bond prices fall; duration risk realized | Growth stocks de-rate; value outperforms |

| Falling Rates | NIM compression; refinancing boosts fee income | Bond prices rise | Growth stocks outperform; dividends valued |

| Inverted Curve | Funding costs exceed lending returns | Short-end elevated | Uncertainty; defensive sectors preferred |

6. Case Study: The Federal Reserve — Power, Independence, and the Dual Mandate {#fed}

The Federal Reserve System, established in 1913 following a series of banking panics, stands as the world’s most influential monetary authority and the de facto guardian of the global dollar-based financial system.

The Dual Mandate

Unlike most global central banks focused solely on price stability, the Federal Reserve operates under a dual mandate enshrined in the Federal Reserve Reform Act of 1977:

- Maximum employment — sustaining the highest level of employment consistent with price stability

- Stable prices — maintaining low and stable inflation over time

This dual mandate creates inherent tension. Achieving maximum employment often requires accommodative policy that risks stoking inflation; combating inflation may require tightening that raises unemployment. The Federal Open Market Committee (FOMC) must navigate this trade-off at every meeting.

The 2022–2023 Tightening Cycle

The Fed’s response to post-pandemic inflation represented the most aggressive tightening cycle in four decades:

- March 2022: First rate hike in three years — 25 basis points

- June 2022: 75 basis point hike — the largest since 1994

- July 2023: Rate peaked at 5.25–5.50% — the highest in 22 years

- September 2024: First cut, initiating an easing cycle

The speed and scale of this cycle had profound global implications — triggering dollar appreciation, capital outflows from emerging markets, debt servicing stress in dollarized economies, and the 2023 regional banking stress described earlier.

Fed Independence: Under Pressure

The Fed’s operational independence — the ability to make monetary decisions free from short-term political influence — is a cornerstone of its credibility. Research consistently shows that central bank independence is positively correlated with lower inflation and stronger macroeconomic outcomes (Cukierman, 1992; IMF Working Papers, 2018).

However, this independence is perennially contested. Political pressures to reduce rates ahead of elections, calls for the Fed to finance government deficits, and debates over its climate and supervisory mandates all represent ongoing challenges to institutional design.

“Central bank independence is not a gift from governments to technocrats — it is a commitment device that makes monetary policy more credible and ultimately more effective.” — Former BIS General Manager, Claudio Borio

7. Case Study: The European Central Bank — Governing the Ungovernable {#ecb}

The European Central Bank (ECB), established in 1998 and headquartered in Frankfurt, faces a challenge unique in the history of global banking governance: conducting a single monetary policy for 20 sovereign nations with vastly different economic structures, fiscal positions, and political traditions.

The Single Mandate and Its Implications

Unlike the Federal Reserve, the ECB operates under a single mandate: price stability, defined as inflation “below, but close to, 2%” over the medium term (updated to a symmetric 2% target in the 2021 strategy review).

This narrow focus was designed to insulate the ECB from political pressure to prioritize growth or employment — critical given the governance challenges of a multinational institution. In practice, however, the bank’s actions inevitably influence growth and employment across the Eurozone.

Fragmentation Risk: The Unique Eurozone Challenge

One challenge with no equivalent in other major central banks is fragmentation risk — the possibility that ECB rate decisions transmit unequally across member states, with peripheral economies (historically: Italy, Spain, Portugal, Greece) experiencing disproportionate stress when rates rise.

The ECB has developed specific instruments to address this:

- Transmission Protection Instrument (TPI): Launched in 2022 to allow targeted bond purchases in countries experiencing unwarranted spread widening

- Outright Monetary Transactions (OMT): The “whatever it takes” backstop announced by President Mario Draghi in 2012, widely credited with ending the sovereign debt crisis

- Targeted Longer-Term Refinancing Operations (TLTROs): Providing cheap, long-term funding to banks conditional on maintaining or expanding lending

“Whatever It Takes” — A Study in Central Bank Communication

When ECB President Mario Draghi stated in July 2012 that the ECB would do “whatever it takes” to preserve the euro, markets rallied dramatically — without a single euro being spent. This episode remains the most dramatic demonstration of the power of forward guidance in central bank history and is now taught globally as a masterclass in monetary communication.

8. Case Study: The Bank of England — Post-Crisis Resilience and the Gilt Shock {#boe}

The Bank of England (BOE), the world’s second-oldest central bank (established 1694), combines monetary policy responsibilities with the role of prudential regulator — a model increasingly examined by other central banks considering consolidation of financial oversight functions.

The Gilt Market Crisis of 2022

In September 2022, a fiscal event by the UK government — involving large unfunded tax cuts — triggered an extraordinary crisis in the UK government bond (gilt) market. Yields surged sharply, threatening the solvency of pension funds using liability-driven investment (LDI) strategies that were highly sensitive to rate movements.

The Bank of England responded with an emergency gilt purchase program, buying long-dated gilts to restore market functioning — even as it was simultaneously raising rates to fight inflation. This dual and apparently contradictory action — easing in one market while tightening in another — illustrated the complex, multi-dimensional challenges facing modern monetary authorities.

Key lessons from the Gilt Crisis:

- Systemic interconnections between pension funds, leverage, and rate markets are not always visible until stress

- Central banks must sometimes act against their primary policy direction to preserve financial stability

- Communication and sequencing matter as much as the action itself

The BOE’s Evolving Mandate

The BOE has progressively expanded its analytical and supervisory focus to include:

- Climate-related financial risk — pioneering supervisory stress tests for climate scenarios

- Operational resilience — requiring financial institutions to demonstrate ability to remain operational during disruptions

- Artificial intelligence governance — publishing guidance on the use of AI in financial services

9. Global Regulatory Standards: Basel III, IMF Oversight, and BIS Coordination {#standards}

No central bank operates in isolation. The global financial system is governed by a network of international standards, surveillance mechanisms, and coordination frameworks that shape how monetary authorities design and implement policy.

Basel III: The Capital and Liquidity Framework

Developed by the Basel Committee on Banking Supervision (BCBS) — hosted at the Bank for International Settlements (BIS) in Basel, Switzerland — Basel III is the cornerstone international standard for bank regulation, supervision, and risk management.

Core Basel III requirements include:

- Common Equity Tier 1 (CET1) ratio: Minimum 4.5% of risk-weighted assets (with buffers pushing effective requirements to 7%+)

- Leverage Ratio: Minimum 3%, limiting total exposure relative to capital irrespective of risk weights

- Liquidity Coverage Ratio (LCR): Banks must hold sufficient high-quality liquid assets to survive 30 days of stress

- Net Stable Funding Ratio (NSFR): Ensures stable funding over a one-year horizon

Basel III Endgame (Basel IV): The final tranche of Basel III reforms — informally called “Basel IV” — addresses the variability in risk-weighted assets calculated by banks’ internal models, imposing output floors and greater standardization. Implementation has been subject to significant debate in major jurisdictions.

🔗 External Link: Basel Committee on Banking Supervision Publications — access the full Basel III framework, monitoring reports, and consultation papers.

IMF Surveillance and the Financial Sector Assessment Program (FSAP)

The International Monetary Fund (IMF) plays a critical role in the global monetary governance architecture through:

- Article IV Consultations: Annual bilateral surveillance of member country economies and financial systems

- Financial Sector Assessment Program (FSAP): In-depth assessments of financial system stability, completed for all systemically important financial sectors

- Global Financial Stability Report (GFSR): Biannual assessment of global financial market conditions and systemic risks

- World Economic Outlook (WEO): Comprehensive global economic forecasting and policy analysis

🔗 External Link: IMF Global Financial Stability Reports — quarterly surveillance of global financial vulnerabilities.

BIS: The Central Bank of Central Banks

The Bank for International Settlements (BIS) serves as the primary forum for international central bank cooperation. Key functions include:

- Financial research and statistics — including the influential BIS Quarterly Review

- Standard-setting committees — hosting not only the BCBS but also the Committee on Payments and Market Infrastructures (CPMI) and the Financial Stability Board (FSB)

- Reserves management — managing foreign exchange reserves for member central banks

- Innovation Hub — coordinating cross-border CBDC experiments and digital finance research

10. Digital Transformation: CBDCs, FinTech, and the Future of Monetary Policy {#digital}

The intersection of banking innovation and monetary policy represents one of the most consequential developments in contemporary global finance. Central banks are no longer just observers of financial technology — they are increasingly its architects.

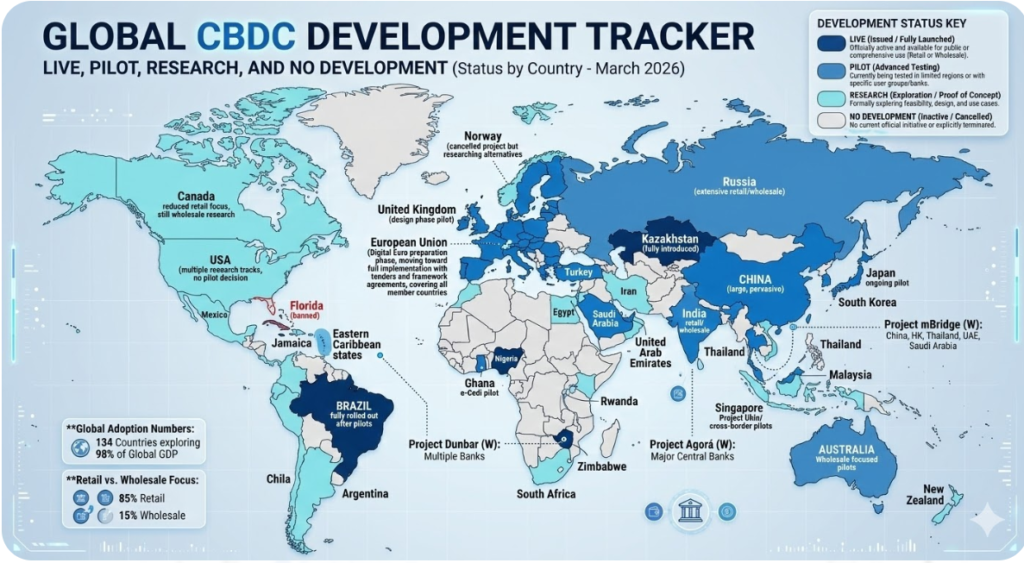

Central Bank Digital Currencies (CBDCs)

A Central Bank Digital Currency (CBDC) is a digital form of sovereign currency issued and backed directly by the central bank — distinct from commercial bank deposits and existing payment systems.

Current global landscape (as of mid-2025):

- Retail CBDCs live: The Bahamas (Sand Dollar), Nigeria (eNaira), Jamaica (JAM-DEX), Eastern Caribbean (DCash)

- Large economy pilots: Digital yuan (e-CNY) with hundreds of millions in transactions; digital euro in preparation phase; digital dollar under research

- Cross-border experiments: BIS Innovation Hub’s mBridge project — exploring multi-CBDC platforms for international settlements

Key policy questions raised by CBDCs:

- Disintermediation risk: If citizens hold CBDCs directly with the central bank, commercial bank deposits could shrink, reducing the banking sector’s credit creation capacity

- Privacy vs. control: CBDCs offer unprecedented transaction visibility — raising civil liberties concerns

- Financial inclusion: CBDCs could extend financial services to the unbanked — echoing M-Pesa’s transformational impact in East Africa, which demonstrated that mobile-based financial services can reach populations entirely bypassed by traditional banking infrastructure

- Monetary policy transmission: Direct CBDC channels could allow more precise policy transmission, including programmable features (e.g., time-limited stimulus payments)

“Global CBDC Development Tracker — Live, Pilot, Research, and No Development” — world map with color-coded status by country

FinTech and the Changing Monetary Transmission Landscape

The rise of FinTech — from peer-to-peer lending platforms to algorithmic trading systems — has altered the channels through which monetary policy transmits to the real economy:

- Non-bank credit intermediation: As FinTech platforms expand credit provision, rate hikes may have less immediate effect on aggregate credit conditions

- Stablecoins: Privately issued digital currencies pegged to fiat — if systemically adopted, could fragment monetary sovereignty

- Algorithmic market-making: High-frequency trading and algorithmic execution may amplify volatility during rate announcements

The Financial Stability Board (FSB) and the Bank for International Settlements have both published frameworks for the regulation of stablecoins and crypto-assets, emphasizing that “same activity, same risk, same regulation” should be the governing principle.

11. ESG, Climate Risk, and the Expanding Mandate {#esg}

Perhaps the most contested evolution in global banking governance is the incorporation of Environmental, Social, and Governance (ESG) considerations — particularly climate-related financial risk — into central bank mandates and supervisory frameworks.

Why Climate Risk Is a Financial Stability Issue

Central banks and supervisory authorities have increasingly concluded that climate change poses material financial risks through two primary channels:

- Physical risk: Direct damage to assets and economic activity from climate events (floods, wildfires, sea-level rise) — particularly relevant to insurance, real estate, and agricultural lending

- Transition risk: Financial losses arising from the repricing of carbon-intensive assets as economies decarbonize — potentially creating a “carbon bubble” in fossil fuel valuations

The Network for Greening the Financial System (NGFS) — a coalition of over 130 central banks and supervisors — has developed climate scenario frameworks now used by major institutions for stress testing and disclosure requirements.

Central Bank Actions on Climate

| Institution | Climate-Related Action |

| Bank of England | Mandatory climate stress tests for banks and insurers since 2021 |

| European Central Bank | Climate-related collateral haircuts; green corporate bond purchases |

| BIS | Published “The Green Swan” report on climate as systemic risk |

| Federal Reserve | Joined NGFS; conducting climate scenario analysis |

| IMF | Integrating climate risk into FSAPs and Article IV consultations |

The Mandate Debate

A significant debate exists about whether climate action falls within or beyond the legitimate mandate of monetary authorities:

The case for inclusion: Climate risk is a financial stability risk; central banks have a duty to identify and address systemic threats to the financial system regardless of their origin.

The case for caution: Central bank mandates are established by democratic processes; expanding them to encompass broad societal goals risks politicizing independent institutions and creating mission creep.

This debate is not merely academic — it will shape the institutional design and political legitimacy of central banks for decades.

12. Best Practices for Financial Institutions Navigating Monetary Cycles {#bestpractices}

For financial professionals and institutions, the central bank cycle creates both risks and opportunities. The following represent global best practices in risk management and strategic positioning:

Asset-Liability Management (ALM)

- Regularly stress-test interest rate risk across multiple scenarios, including non-linear shifts and curve inversions

- Align funding duration with asset duration to reduce NIM volatility during rate cycles

- Maintain adequate liquidity buffers above regulatory minimums (LCR, NSFR) to absorb stress

- Use derivatives (interest rate swaps, caps, floors) to hedge rate exposure where consistent with investment strategy

Credit Risk Management in Rising Rate Environments

- Monitor debt serviceability metrics (DSCR, ICR) across the loan book as higher rates compress borrower margins

- Identify concentration risks in rate-sensitive sectors (real estate, leveraged buyouts, long-duration assets)

- Apply early-warning indicators — rising non-performing loans in rate-sensitive sectors typically lag policy tightening by 6–12 months

Regulatory Capital Strategy

- Maintain capital ratios above minimum requirements and align with Pillar 2 guidance from supervisors

- Prepare for Basel III Endgame implementation, particularly output floor impacts on internal models

- Engage proactively with supervisory stress tests — use FSAP or national stress test scenarios internally for strategic planning

Communication and Stakeholder Management

- Monitor and interpret central bank communications — forward guidance, minutes, speeches, and press conferences are market-moving data points

- Develop internal “monetary policy watch” capabilities — interdisciplinary teams combining economists, strategists, and risk managers

- Communicate rate sensitivity clearly to investors, boards, and counterparties

ESG Integration

- Conduct TCFD-aligned climate risk disclosures — aligned with the Task Force on Climate-related Financial Disclosures

- Incorporate climate scenario analysis into credit risk frameworks, particularly for long-dated assets and real estate collateral

- Engage with NGFS scenarios for forward-looking portfolio stress testing

FAQ {#faq}

Q1: What is the difference between monetary policy and fiscal policy?

Monetary policy is controlled by the central bank and involves managing the money supply and interest rates to achieve macroeconomic objectives. Fiscal policy is controlled by the government and involves decisions on public spending and taxation. Both influence aggregate demand, inflation, and employment, but through different channels and with different institutional actors. The interaction between these two policy domains — particularly the risk of fiscal dominance (where fiscal pressures compromise monetary policy independence) — is a central concern in global banking governance.

Q2: Why do central banks target 2% inflation rather than 0%?

A zero inflation target would leave no buffer against deflation — a condition where falling prices cause consumers and businesses to delay spending, creating a downward spiral that is extremely difficult to escape (as Japan’s “lost decades” illustrate). A 2% target provides this buffer, accommodates the natural process of relative price adjustment, allows real wages to rise with modest nominal wage growth, and gives central banks room to cut real rates below zero by setting nominal rates near zero. The specific 2% figure has become a global benchmark through convergence among major central banks, reinforcing its role as an anchor for inflation expectations.

Q3: How do central bank decisions in advanced economies affect emerging markets?

Central bank decisions — particularly those of the Federal Reserve — transmit globally through multiple channels: exchange rate effects (dollar appreciation on rate hikes tightens financial conditions in dollarized and dollar-indebted economies); capital flow volatility (rate hikes in advanced economies attract capital away from emerging markets, raising their borrowing costs); and commodity price effects (dollar strength typically pressures commodity prices, affecting commodity-dependent economies). The IMF documents these “spillover effects” extensively and has called for enhanced policy coordination and communication to mitigate their impact on financial inclusion and development goals.

13. Conclusion: The Road Ahead {#conclusion}

Central banks have navigated extraordinary terrain over the past two decades: a global financial crisis, zero interest rates, experimental quantitative easing, a pandemic-driven demand collapse, a once-in-a-generation inflationary surge, and the emergence of digital money. Through each episode, the toolkit has expanded, the mandates have evolved, and the expectations of what monetary authorities can and should achieve have grown.

Key Takeaways

- Monetary policy is both science and art — informed by models and data, but ultimately dependent on judgment, credibility, and communication

- The lender of last resort function is irreplaceable — but its expansion increases moral hazard and demands robust complementary regulation, including Basel III compliance

- Inflation targeting remains the dominant framework — but its application must be flexible enough to accommodate asymmetric risks and structural change

- Interest rate cycles have deep, prolonged consequences for financial institutions, markets, and the real economy — requiring sophisticated ALM and risk management capabilities

- Digital innovation is reshaping the monetary landscape — CBDCs, FinTech, and stablecoins require urgent regulatory clarity aligned with FSB and BIS standards

- Climate risk is financial stability risk — central banks and financial institutions that fail to integrate this reality into their frameworks will face growing supervisory and market pressure

The Emerging Agenda

Looking forward, several themes will define the evolution of global banking and monetary governance:

- Artificial Intelligence in Central Banking: From nowcasting models to natural language processing of financial communications, AI is transforming how monetary authorities gather, analyze, and act on information. The BIS Innovation Hub is actively researching AI applications in central banking.

- The Geopolitics of Reserve Currencies: The dollar’s dominance is being challenged by the internationalisation of the renminbi, the development of multi-CBDC platforms, and the search for alternatives to SWIFT. Central banks are diversifying reserve portfolios into gold, euros, and other currencies.

- Fiscal-Monetary Coordination: Elevated public debt levels in advanced economies raise the specter of fiscal dominance — where central banks face pressure to keep rates artificially low to reduce debt servicing costs, at the expense of price stability. Maintaining independence while acknowledging fiscal realities is a defining challenge.

- Sustainable Finance Mainstreaming: The integration of ESG principles into monetary policy frameworks, collateral frameworks, and supervisory requirements will accelerate, with NGFS scenarios becoming standard tools for systemic risk assessment.

- The Next Crisis: History teaches that each financial crisis arrives in a form partly shaped by the regulatory response to the last one. The next systemic shock — whether from commercial real estate, private credit markets, geopolitical disruption, or an unforeseen technology failure — will once again test the limits of the monetary authority’s toolkit.

For financial professionals navigating this landscape, the imperative is clear: understand the central bank, understand the cycle, and build institutions resilient enough to weather whatever the next volatile chapter brings.

🔗 Further Reading & External Resources:

- BIS Annual Economic Report — Comprehensive annual assessment of the global monetary landscape

- IMF World Economic Outlook — Biannual global economic analysis

- FSB Annual Report — Financial Stability Board’s global supervisory reform progress

- NGFS Climate Scenarios — Central bank climate risk frameworks

- Basel Committee Publications — Full Basel III/IV regulatory framework

This article reflects publicly available information and analysis as of mid-2025. It is intended for educational and informational purposes and does not constitute financial or investment advice.